- The Bank of England lifted its policy rate by 50bps today in line with consensus forecasts, but disappointed markets that saw around a two-thirds chance of a 75bps hike.

- We think the government’s Growth Plan should have motivated pre-emptive action from the BoE today with a 75bps rate increase.

- Despite the BoE missing our expectation for this meeting, we see upside risks to our latest official BoE forecast.

The Bank of England lifted its policy rate by 50bps today in line with consensus forecasts, but disappointed markets that saw around a two-thirds chance of a 75bps hike to 2.50% (which was also our forecast).

We think the impact of the government’s Growth Plan, with details due tomorrow, will lead to a period of higher core inflation (than previously thought) that should have motivated pre-emptive action from the BoE today with a 75bps hike.

The lower-than-expected hike should have depressed UK yields, but the Bank’s announcement that it will begin active gilt sales in early-October as planned (at a pace of £40bn/year) sent the yield on 10-yr bonds higher by up to 13bps versus pre-decision after some speculation had built that the BoE’s plans would change due to higher HMT issuance related to Truss’s plans.

On the other hand, the disappointingly sized hike nullified the positive impact of higher long-term yields on the GBP, translating into a net roughly unchanged GBP against the EUR and the USD. Sterling gains for the day by and large reflected the broad move against the USD with Japan’s MoF intervention in FX markets. The QT impact is also reflected in a more modest increase in 2-yr yields, relative to 10-yr yields, of only ~2–3bps at writing compared to pre-statement levels.

The split vote saw five members (including Gov Bailey and Chief Econ Pill) vote for a 50bps hike against three hawks in favour of a 75bps increase and a surprising 25bps vote from Dhingra at her first MPC appearance (out-doving Tenreyro who voted for 50bps).

The minutes of the meeting accompanying the statement imply that some MPC members preferred to wait for the full details of the Truss/Kwarteng plan before opting for a 75bps increase. This suggests a 75bps hike remains on the table for the November decision where the Committee will “make a full assessment” and incorporate the government’s announcements in its updated MPR projections.

Despite the BoE missing our expectation for a 75bps hike, we see upside risks to our latest official BoE forecast. Our September update projects that the BoE will continue its hiking cycle with an additional 100bps in tightening by year-end, taking the bank rate to 3.25% and holding there until late-2023, at least.

The tone of today’s minutes, teeming with references to inflationary pressures and upside risks (now also from the demand side), highlights that the bank is more concerned about entrenched inflation than previously thought and they’re ready to impact demand more harshly to prevent runaway inflation.

The surprising resilience of UK labour markets and robust wages growth as well as fiscal support against the cost-of-living crisis—that should translate into relatively higher and longer-lasting core inflation—opens the door to at least 50bps more in tightening than we have penciled in. On top of a 50 or 75bps move in November and a half-point increase in December, the Bank looks positioned to roll out at least two additional rate increases next year, perhaps taking its policy rate past 4%.

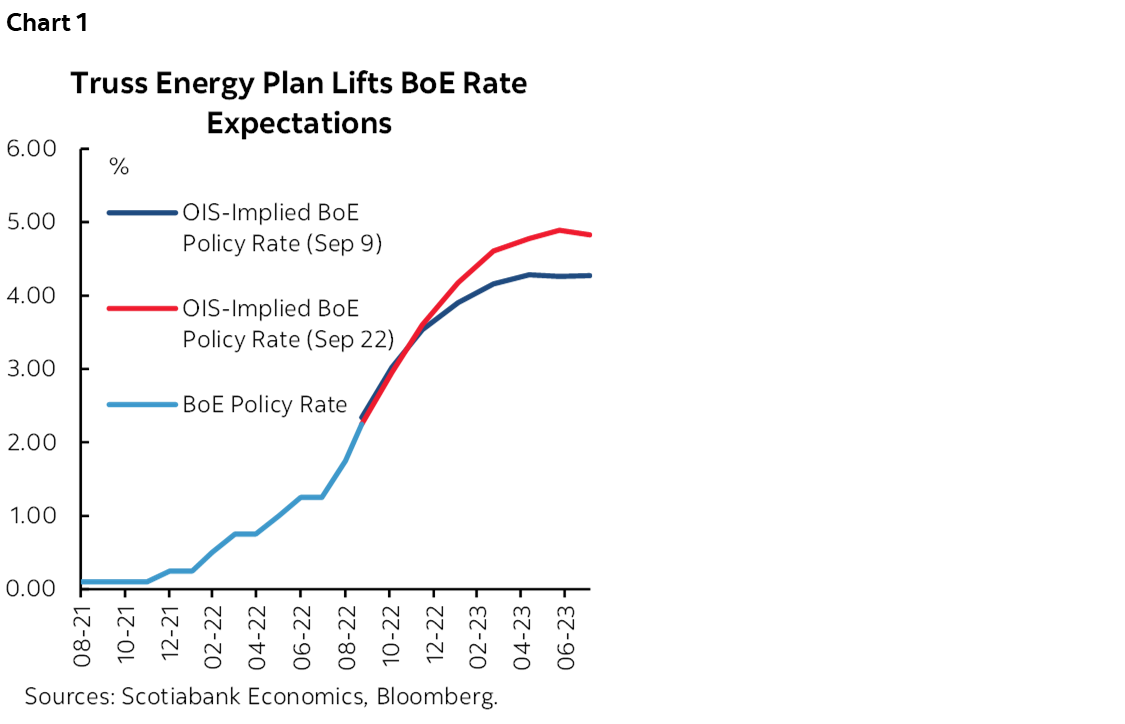

Whether this is enough to prevent continued currency weakness remains to be seen. The bar for a strong GBP is high given that markets are already expecting the BoE to lift its policy rate to close to 5% by H2-2023 (chart 1), which seems excessive in our opinion. Moreover, there are a multitude of factors conspiring against the GBP aside from a hawkish Fed and an ECB that is catching up: an economic contraction, energy supply risks, increased public spending without fiscal offsets, poor productivity/investment, and the effects of Brexit.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.