- The Canadian labour markets have displayed strong momentum as the central bank walks the inflation-recession tightrope. The robust labour market performance since early 2021 is not a myth—this note delves into the impact of surging labour demand on wages and production costs, assessing how these factors could influence inflation going forward.

- In 2021, the strong rebound in consumer demand following the pandemic-induced downturn led to a significant ramp-up in production to meet demand, with firms recruiting more inputs to increase supply, including labour.

- Wage growth rose well above its trend pace with rapidly increasing labour demand. However, labour costs declined in real terms for the majority of the period since early 2021 given the faster increase in product prices compared to nominal wages, spurring labour demand.

- Labour costs have had a limited impact on propelling price inflation, but remains an important driver for the trajectories ahead of inflation, monetary policy and growth. Real business-sector unit labour costs (ULC) began putting pressure on inflation in late 2022 as labour’s value added started lagging wage growth, increasing production costs for Canadian businesses.

- Our baseline forecast for the Canadian economy expects it to return to excess supply by the last quarter of 2023. As firms adjust to higher labour costs in an environment of weakening consumer demand, wage growth should slow down as labour market tightness dissipates, which should help drive inflation down over the 2023–2024 period.

- However, if wage growth does not slow down and continues at its current speed, it could add additional pressure on inflation through higher production costs, forcing the hand of the central bank. Although the wage-price spiral has not yet materialized as a threat to inflation, it is crucial for wage growth to materially decelerate from its current 5% range and/or productivity to improve to bring inflation down to its target range.

- Our model shows that more persistent wage pressure combined with reduced central bank credibility could lead to a larger decline in real growth for the central bank to bring inflation back to its target, reducing the possibility of a soft landing. Without a loss in credibility, strong wage growth only has limited impact on inflation—this highlights the need for central banks to show material progress in achieving price stability.

LABOUR MARKETS SHRUG OFF RATE HIKES AND KEEP ROCKING ON

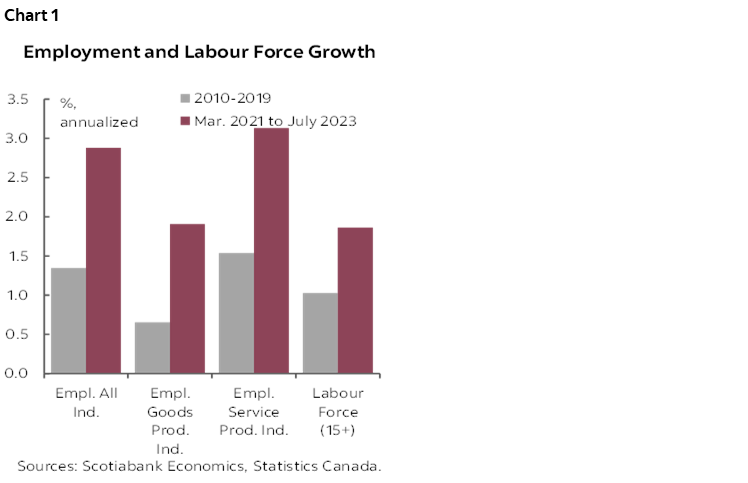

The Canadian economy has been experiencing a prolonged period of labour crunch with the pace of employment growth significantly outstripping labour supply. The impressive 2.9% annual growth in LFS (Labour Force Survey) employment since March 2021 is well exceeding its pre–pandemic decade trend growth rate of 1.3%, with hiring growth exceeding historical averages in both goods and services sectors (chart 1). Strong employment performance during this period is accompanied by elevated job vacancy rates, and a historically low unemployment rate, highlighting the extreme tightness in the job market.

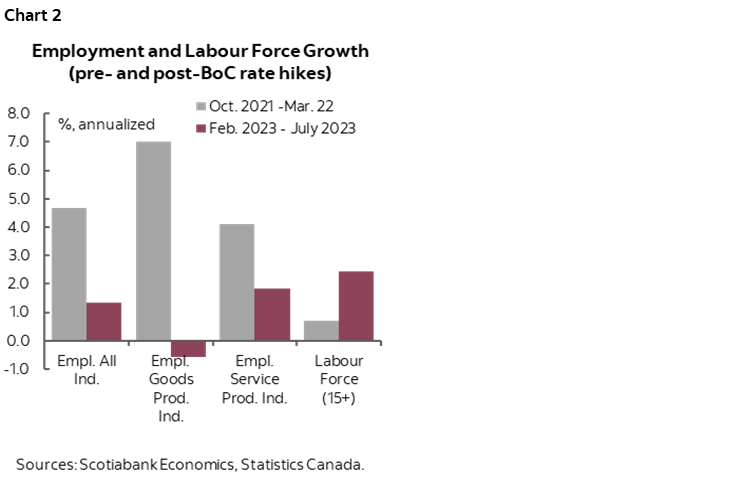

Despite the sharp hikes in the policy rate since March 2022 and the continued rise in real interest rates (as discussed in this note), the labour market has surprised on the upside with its resilience. Employment growth inevitably slowed—LFS employment grew by an annualized 1.3% in the last 6 months, down from 4.7% in the 6–month period to the Bank of Canada’s policy rate liftoff in March 2022 (chart 2). Employment growth in goods production plunged from the whopping 7% to a rate more consistent with its pre-pandemic average, before contracting sharply in July. Employment growth in the service sector also softened from over 4% before BoC’s liftoff to only slightly above its long-term average, despite of strong increases in the transport & warehousing industry likely boosted by healing supply chains. Labour supply improved notably thanks to booming immigration, providing some relief to the labour market tightness. However, it continues to remain constrained, as reflected by near historically low unemployment rate and the persistently elevated 4.3% job vacancy rate as of May 2023, well above the 2.8% average in the 5-year period preceding the pandemic (2015–2019). Demand for labour still exceeds supply.

The tightness in the Canadian labour market is a result of strong labour demand driven by increased production, affordable labour costs and strong domestic and global demand. Since 2021, the Canadian economy has been in a sharp recovery from the pandemic-induced downturn, which led to a significant ramp-up in production to meet demand. Slack in the economy was quickly reduced and the output gap closed at the end of 2021. Firms have accommodated the pent-up demand by enlisting more inputs to increase production, leading to a rise in labour demand. Furthermore, labour costs became relatively cheaper (explained below), which has made hiring more workers a profitable option for firms. As a result, the labour market has shown significant momentum, marked by strong job gains, historically low unemployment rate, and high vacancies.

LABOUR COSTS REMAIN AFFORDABLE DESPITE BURGEONING GROWTH IN NOMINAL WAGE

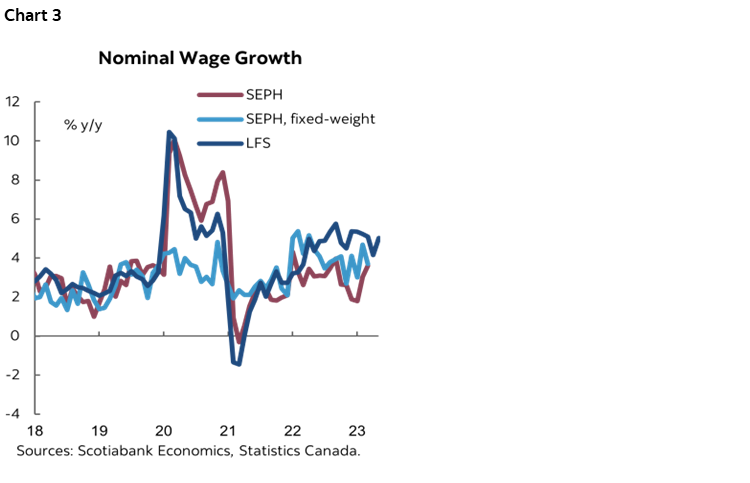

Tight labour market conditions beget robust nominal wage growth (chart 3). These conditions contributed to strengthen wage growth with firms bidding them up to attract and retain workers. They also provided workers with a strong bargaining position and the willingness to use it to recover their loss in purchasing power from the strong rise in consumer prices since March 2021. Nominal wage growth—as measured by both the average and median hourly wage rate from the Labour Force Survey (LFS)—grew at 2–3% y/y before the Bank of Canada’s policy rate liftoff in March 2022. Wage growth from both indicators trended up thereafter and peaked well above 5% in November 2022. It declined since but was still elevated in July, at 4% and 5% respectively for the median and average hourly wage. Annual wage inflation indicators tracked by the Survey of Employment, Payrolls and Hours (SEPH) have also strengthened during a similar period. They have generally been weaker than the LFS measures since July 2022—hovering within a 3% to 4% range.

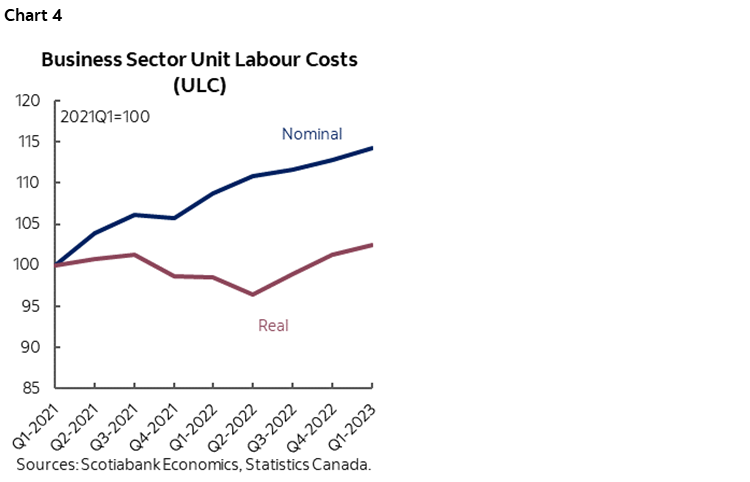

Despite rapid growth in nominal wage, labour costs became effectively cheaper in real terms for most of the period since early 2021, underpinning strong employment growth. In the context of employment decisions, when a firm decides to hire an additional worker, it assesses additional revenues this worker would generate, or its value added, weighed against their cost. This trade-off is captured by the real unit labour cost indicator, representing the real compensation of a worker per unit of output. This metric is directly linked to the value added from labour and consequently labour productivity. An increase in wages does not necessarily translate into heightened labour costs or increased production expenditures, as long as it corresponds to a commensurate rise in labour’s value added. Consequently, a decrease in real ULC indicates that labour is becoming more affordable relative to the value it contributes to a firm’s production, thereby fostering a subsequent upswing in labour demand. Real ULC1 have been on a downward trend from Q1 2021 to Q2 2022 (chart 4), suggesting that wages increased at a slower pace than labour’s value added over this period.

1 The real ULC figures are calculated by their nominal—or published (by Statistics Canada)—figures deflated by the implicit price index for the business sector, a proxy for businesses’ selling price.

Labour costs have not contributed materially to price inflation since 2021 but could become increasingly inflationary. Labour compensation accounts for a significant share of production costs (roughly 50% of GDP), and even higher in the service sectors. The economy wide ULC indicator is now almost at its early 2021 level in real terms, suggesting that the contribution of labour costs to elevated inflation since early 2021 has been neutral. In the case of the business sector, real labour costs started to contribute positively to this rise in inflation only in the last quarter of 2022. The recent pick-up in real ULC can be attributed to the slowdown in product price inflation since mid-2022 and the mediocre performance of labour productivity. These two factors have contributed to constraining the rise in labour’s value added below wage growth.

HIGHER LABOUR COSTS, DEPLETING PENT-UP DEMAND WILL DRIVE WAGE GROWTH DOWN

With expected headwinds on sales and revenues from the expected easing in economic conditions, businesses are expected to slow their demand for labour. Our most recent outlook expects Canada’s economic activity will slow markedly over the coming quarters and even post a mild decline in the first quarter of 2024 (-0.1% at annual rate). Growth resumes after but the expected slowing in economic activity will reduce annual average growth in real GDP from 3.4% in 2022 to 1.7% in 2023, and 0.9% in 2024. Businesses’ sales and revenues are also expected to slow along with economic activity which will slow their demand for labour and ease labour market conditions and wage growth. We expect wage to grow at a slower pace in the order of 4% over the remainder of the year before slowing to 3% by the end of 2024. Assuming labour productivity recovers at a pace consistent with its trend, real unit labour cost is expected to rise at an annualized pace of 0.7% over the same period. This pace is consistent with the expected decline in inflation in our baseline outlook from 3.5% in second quarter of 2023 to 2.1% in last quarter of 2024.

CONTINUED UPWARD PRESSURE ON WAGE GROWTH CAN INCREASINGLY BECOME A CONCERN FOR THE ECONOMY AND THE BoC…

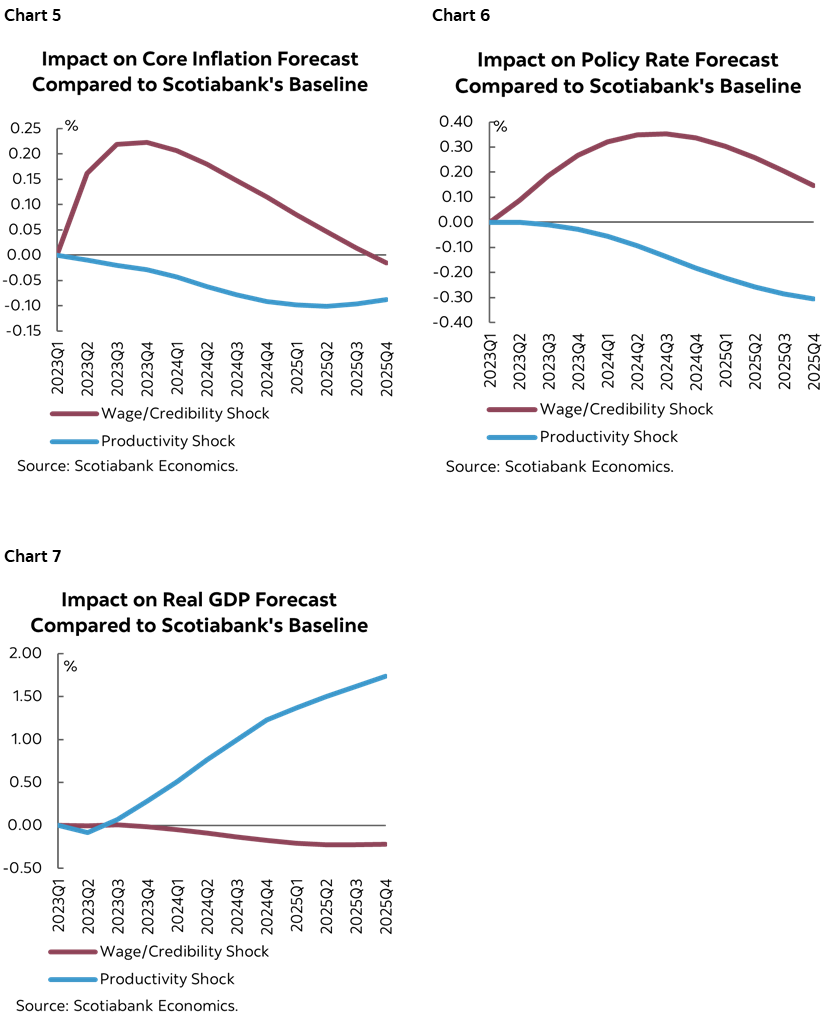

Wage growth needs to slow rapidly from current speed to bring down inflation. To illustrate the importance of slower wage growth for inflation, interest rates and economic outlook, we use our macroeconomic model to generate an alternative scenario in which workers have: 1) reduced confidence that the central bank will achieve a meaningful reduction in inflation by the end of 2024, and 2) a stronger desire to recover the loss in their purchasing power. In this scenario, the weight allocated to the inflation target by workers when forming their wage demand is reduced at the expense of a stronger weight on past—and more elevated—inflation figures, and their wage demand stays near recently observed annual pace of 5% in the next 12 months, rather than declining with the expected labour market cooling as in our baseline scenario. This scenario essentially assumes that the pick-up (to 4.1%) in the average annual percent wage adjustment for 2023Q2 wage settlements—from an about 2.5% average in second half of 2022—will continue over our forecast horizon.

In this alternative scenario where wage growth remains in the 5% range, the rate of decline in consumer price inflation is much slower than in our baseline outlook (chart 5). Given stronger inflation pressures, the path of policy rate is also higher than in our baseline outlook (chart 6) —by 30 bps on average over 2023–2024—and economic activity weaker (chart 7). To summarize, more persistent wage pressure and reduced central bank credibility are leading to a larger decline—or sacrifice— in GDP for the central bank to achieve its inflation objective. This highlights the need for central banks to show progress in achieving their stated inflation objective.

… UNLESS PRODUCTIVITY IMPROVES, WHICH DAMPENS INFLATION AND ALLOWS WAGE TO GROW FASTER

While wage growth is increasingly a concern, the likelihood of lower productivity growth could be a greater threat to economic growth and inflation. Labour productivity is a critical factor in determining labour demand, as it measures the value added from an additional hour of work to a business’ profitability. As labour productivity rises, firms become more willing to use labour to extract efficiency gains and potential additional profits, which in turn increases labour demand. This leads to higher wages as firms are willing to attract additional workers or encourage current workers to work additional hours to benefit from this productivity gain. The additional wage gains can be justified by increased output per hour worked, and therefore put downward pressure on price inflation. In other words, the economy can sustain higher wage growth if productivity growth picks up.

Simulation results from our macro model prove that not only does higher productivity benefits workers by raising trend wage growth, it also has the effect of reining in inflation and boosting economic and income growth. In this simulation, the productivity profile is raised to generate the same wage profile as in the previous illustrative scenario. In this higher productivity scenario, wage growth improves for reasons explained in the previous paragraph, and this now comes from a series of productivity boosts throughout 2023–24 instead of a wage-price spiral. The results show a slightly lower trajectory for core inflation by an average of 5 bps, and consequently faster pace of rate cuts by the Bank of Canada—approximately one rate cut more than our baseline forecast by the end of 2024. But the key point is the higher level of economic activity compared to the baseline and the previous alternative scenario (chart 7). Higher productivity growth raises the speed at which the economy can grow without generating additional pressure on inflation.

Against the backdrop of low/negative productivity growth, wage growth needs to slow from current speed. If wage growth remains at current speed, labour productivity will need to grow at above 2% y/y to offset the effect of strong wage growth on labour costs and therefore on inflation—a very fast pace when compared to its historical performance. Productivity growth is currently in line with the pre-pandemic trend, but the recent movements in total hours worked and output growth suggest productivity could decline further in the near term, raising production costs for firms. If wage growth persistently exceeds productivity growth, firms face higher labour costs per unit produced and may raise prices to preserve profitability, potentially reinforcing inflationary pressures especially in labour-intensive sectors. (See this note for Scotiabank Economics’ theoretical framework to study wage growth, inflation and productivity.)

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.