- Our forecast assumes a gradual decline in inflation that results principally from a fast improvement of the domestic and global supply constraints and bottlenecks, the recent fall of the price of oil and the expected slowdown of the US and Canadian economy. The pace at which inflation falls is limited by a forecast of solid wage growth in 2023, leading us to forecast inflation of around 4% this year, with a return to the 2% target in 2024.

- There is considerable uncertainty around this outlook. We investigate the effect of four alternative scenarios to give a sense of the risks around our view. Two are on the upside (more current excess demand and a deterioration of the supply constraints and bottleneck over the next 2 years) and two are to the downside (a faster effect on inflation of the recent important improvement in supply constraints and a 90/91 type recession).

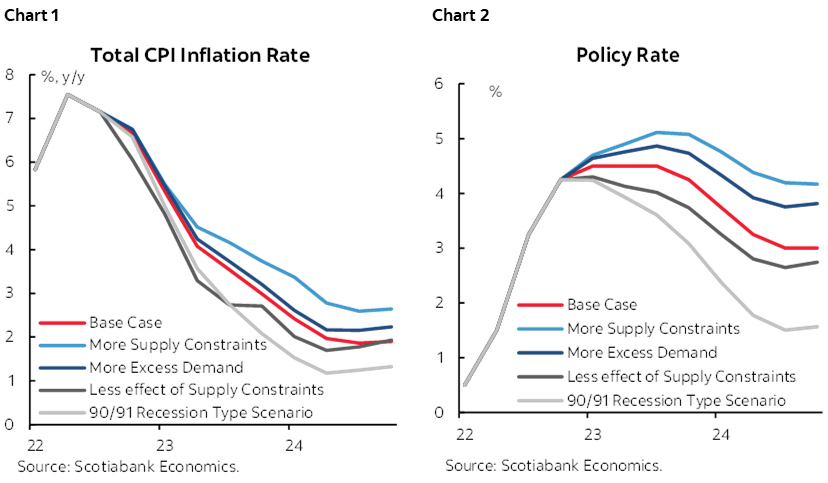

- Though some scenarios are admittedly dramatic, they imply an upper and lower band for average inflation in 2023 of 3.3% to 4.5% (chart 1). Likewise, a 1990/91 recession could lead to a cut in the policy rate to 3.0% by the end of this year, while an important resurgence of supply constraints could see the policy rate rise further to 5.0% (chart 2).

Recent developments in Canadian inflation suggest that it is firmly on a downward path. This is of course much welcome following the post-pandemic experience with inflation. This experience has shaken our understanding of inflation dynamics and there is an ongoing debate about its drivers and, as a result, the appropriate policy response to it.

Our view is that most of the inflation we have experienced in Canada results from factors that, to date, have largely been beyond the control of the Bank of Canada. Global supply issues, high (though now lower) commodity prices, transportation bottlenecks and shipping delays, and of course low inventories. While these factors have the semblance of being supply issues, we take the perspective that the inflation challenge has its roots in the rapid acceleration of global demand resulting from the massive monetary and fiscal stimulus laid out during the early days of the pandemic in 2020. This created a wedge between global demand and supply that was exacerbated by COVID-19 supply challenges. There was always going to be a temporary dimension to the inflation shock—as supply rose to meet demand, and demand normalized as life returned to normal and central banks began to withdraw some stimulus. It was clear however, that the inflation shock was far more persistent than expected and that had a large impact on expectations, and of course eventually on wages. The deviation of inflation from targets and overheating in major economies necessitated a pronounced monetary tightening, as is now clear in actions take to date.

Our forecast assumes a gradual decline in inflation that results principally the already observed decline in input prices. The pace at which inflation falls is limited by a forecast of solid wage growth in 2023, leading us to forecast inflation of around 4% this year, with a return to the 2% target in 2024. Monetary policy will have a limited impact on much of the decline in inflation that is expected as it essentially reflects global developments. That being said, a normalization of international factors will not be sufficient to return inflation to 2% hence the need for policy actions taken to date. In our current forecast, the Bank of Canada’s policy peaks at its current level and is cut once near end-2023.

There is no question that our faith in our collective ability to forecast inflation has been shaken over the last couple of years. While Canadian inflation is evolving largely in line with models and forecasts now (our inflation forecast for 2023 has been reasonably stable since September), there is no question that forecasters and policymakers must be humble when forecasting inflation. A few months of data that align with general expectations do not make up for several quarters of serious underestimation. It is with this perspective in mind that we consider a few scenarios around our baseline view of inflation. We estimate two plausible scenarios which could result in higher inflation and two scenarios in which inflation might come down more rapidly than expected. In both cases we lay out implications for monetary policy and the outlook. The aim is simply to shed some light on alternative inflation paths in light of the inflation forecasting errors of the last two years.

We first consider two scenarios that could lead to higher inflation. The first assumes that excess demand is twice what we currently assume. The recent performance of the Canadian economy and labour market suggest that this assumption might be more realistic than would have been the case a month ago. This leads to inflation rising by about one third of a percentage point relative to our current forecast (2023: 4.2% vs 4.0% and 2024: 2.3% vs 2.0%) and, by the end of 2024, a gradual additional 75 basis points of tightening in Canada relative to the base case. In this scenario the peak response of the Canadian policy rate is 4.75% instead of 4.5% in the base case. The second assumes a further rise in input costs associated with additional disruptions in supply chains and higher oil prices, such as what might occur if the war in Ukraine deteriorated. In this scenario, inflation gradually rises by more than half a percentage point above our current forecast (2023: 4.5% vs 4.0% and 2024: 2.8% vs 2.0%), leading to a persistent peak policy rate of 5.00%. The policy rate is still at 4.25% at the end of 2024 compared to 3.0% in our base case.

On the downside, we consider a scenario where the economy is confronted by a 1990/91 type recession. This quadruples the amount of excess supply expected at end-2024 and leads to a roughly 1% decline in inflation relative to our current view. The fall in inflation and economic activity would force the Bank of Canada to cut rates immediately and rapidly, with the policy rate falling to 3% by the end of this year and 1.5% at the end of 2024. This is clearly a dramatic scenario, which is clearly at odds with the upward revisions to the outlook in recent weeks. A more realistic scenario is built around a faster passthrough of supply chain improvements to inflation as our inflation model incorporates an estimated relation between supply delivery indices and inflation. An acceleration of this channel would shave about one third of a percentage point from inflation by the end of this year. This would force the Bank of Canada to lower rates 50 bps below the base case at the end of 2023.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.