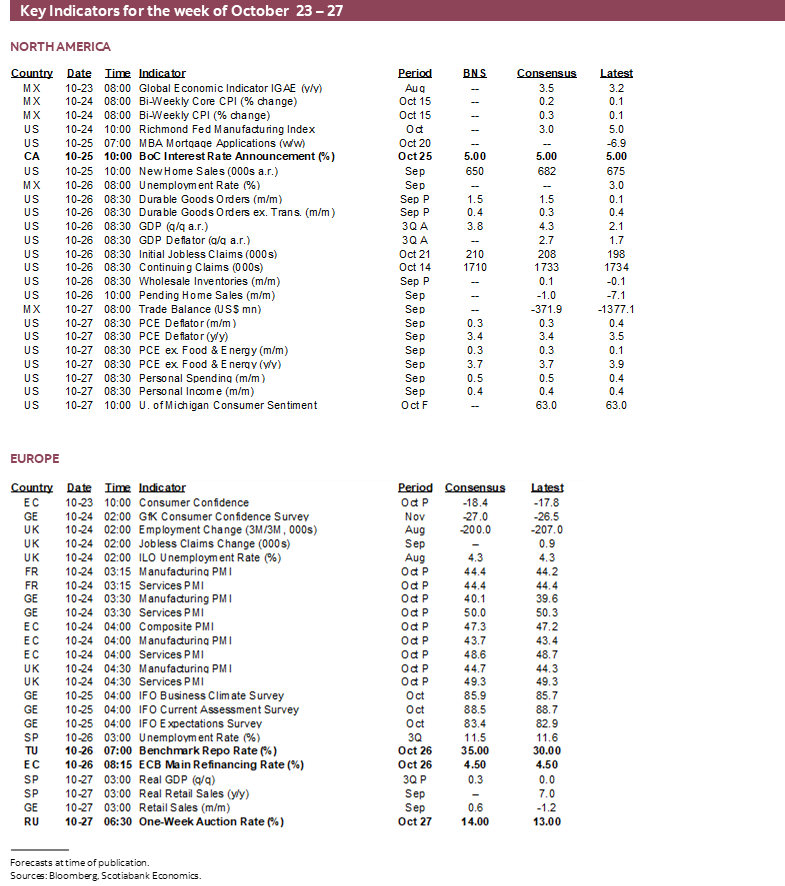

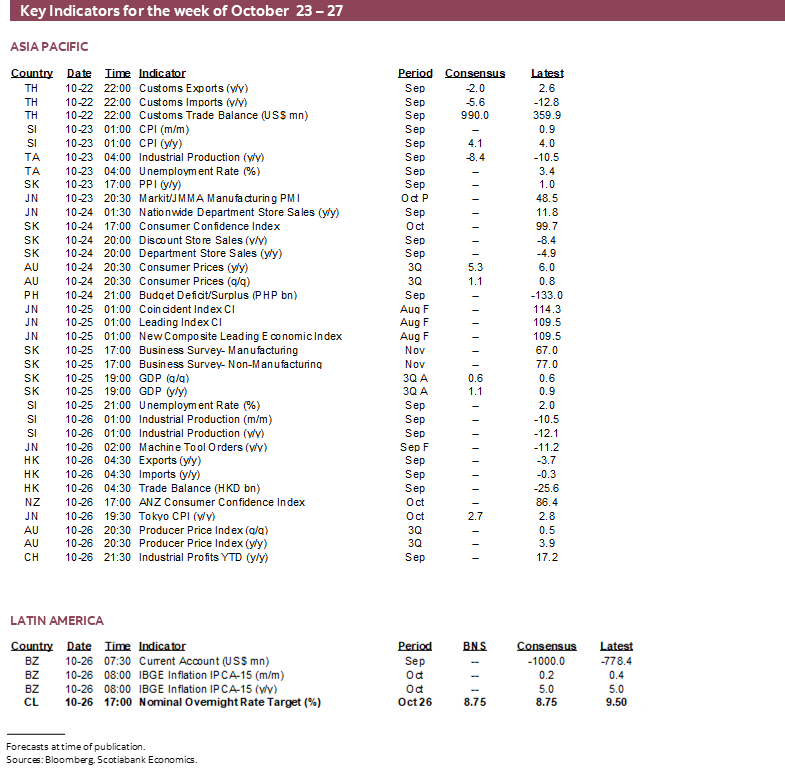

Next Week's Risk Dashboard

- Financial markets are functioning well through the risks

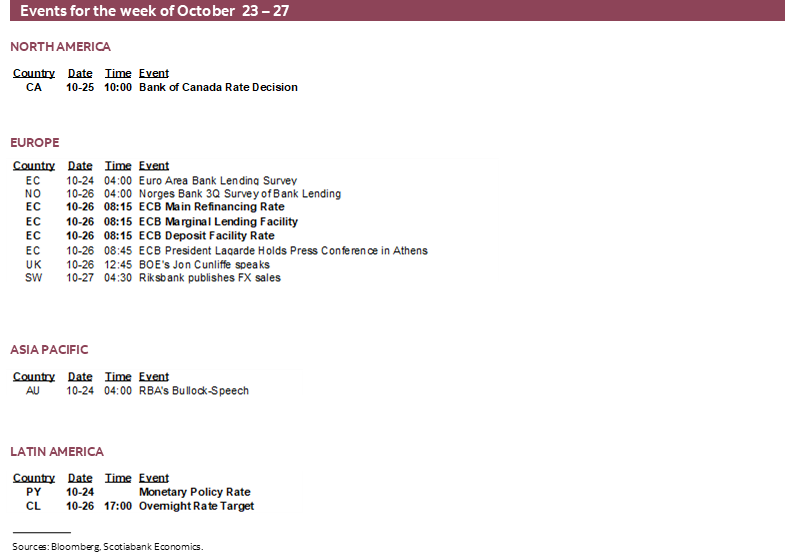

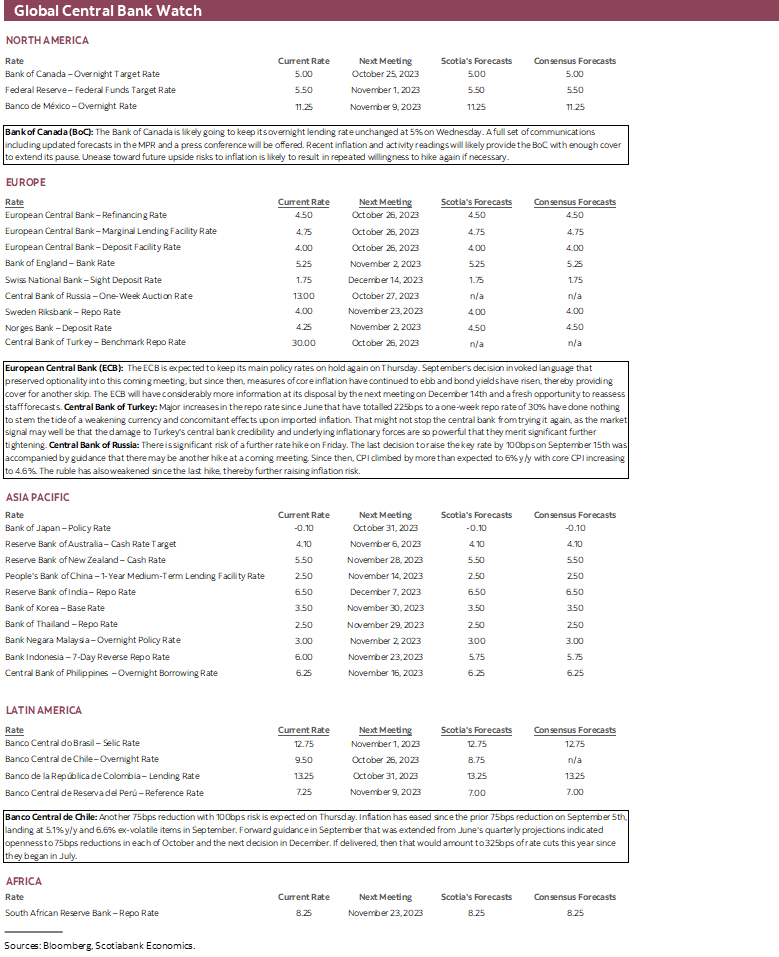

- ECB expected to pause, but will it preserve optionality?

- BoC still faces upside risks to inflation

- US Q3 GDP to showcase a strong economy

- US PCE, Tokyo, Aussie inflation updates

- Chile’s central bank to cut again, peso a concern

- Tumbling shekel limits Bank of Israel’s options

- Turkey’s central bank still struggles with the lira

- Russian central bank to hike as inflation reaccelerates

- PMIs to inform Q4 global growth momentum

- The UK’s weakening job market

- earnings roll on

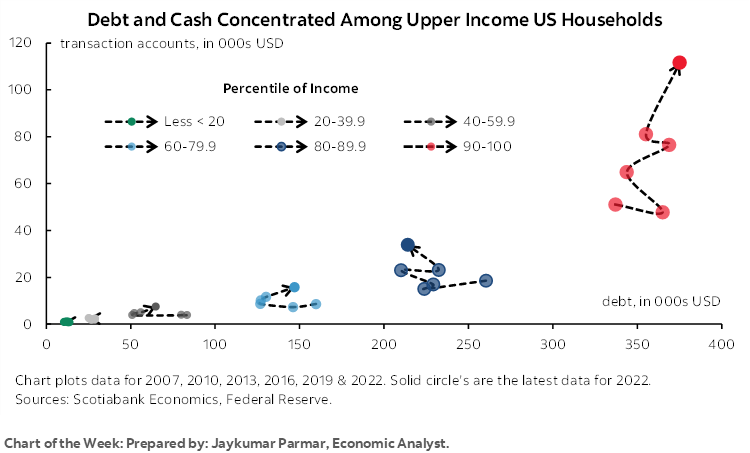

Chart of the Week

The coming week will offer a mixture of optimism and concern toward the global economy and geopolitical developments.

A week of extremes could well include intensification of the war in Israel with the risk of spillover effects. The US House of Representatives remains in limbo, unable to advance a Speaker, and hence unable to process required bills not least of which ones to fund war efforts and avert a government shutdown by mid-November. Maybe a cathartic process is underway as one by one the leftovers from the prior regime face their days of reckoning.

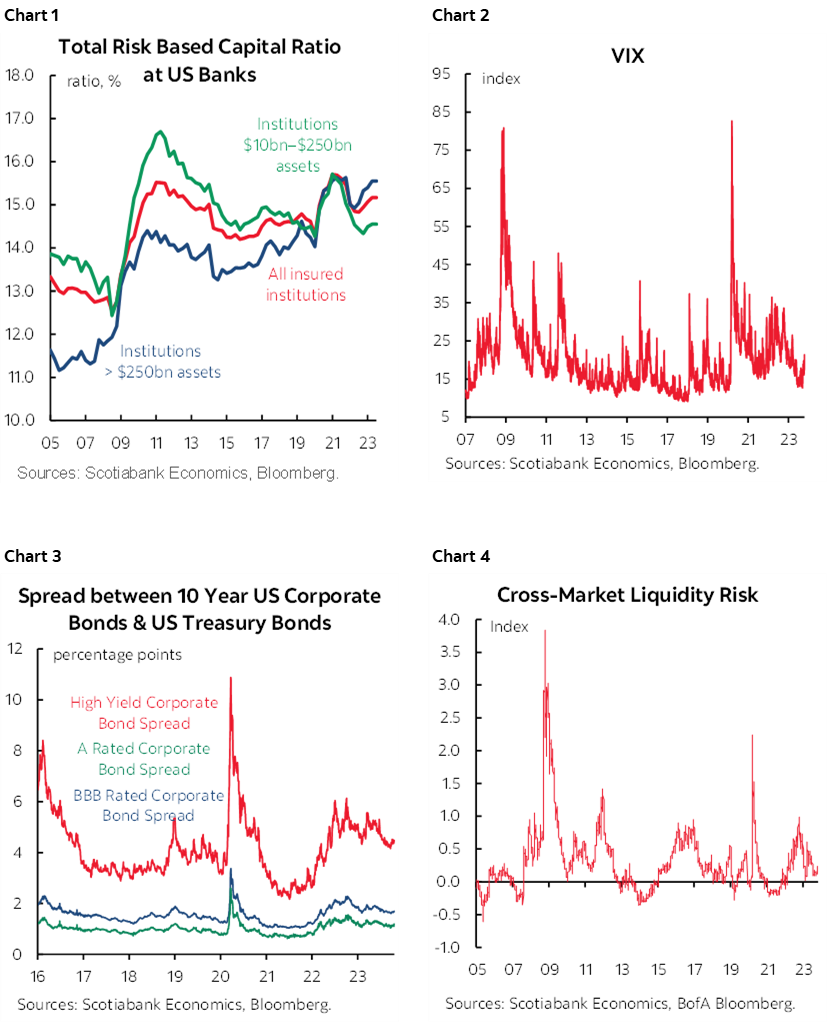

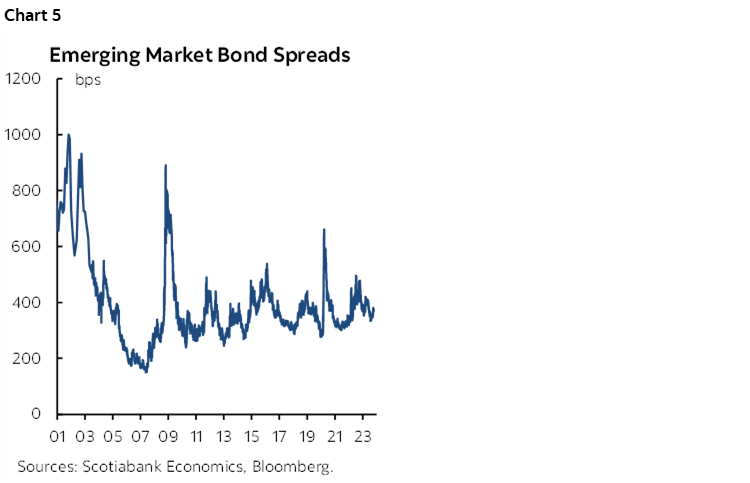

For the audience of a publication such as this one, it’s important to stress the supporting factors into such risks and uncertainties to help assuage some of the very legitimate concerns. For one thing, banks are well capitalized and hence well positioned to adapt with one example being the position of US banks in chart 1. You could add Canadian banks, among others. Financial markets continue to function very well as evidenced by measures of equity market volatility (chart 2), corporate bond spreads (chart 3), cross-market liquidity risk (chart 4) and emerging market debt spreads (chart 5). Even during the bond market sell off, markets have been functioning well while pursuing price discovery toward what should perhaps be new equilibrium resting points.

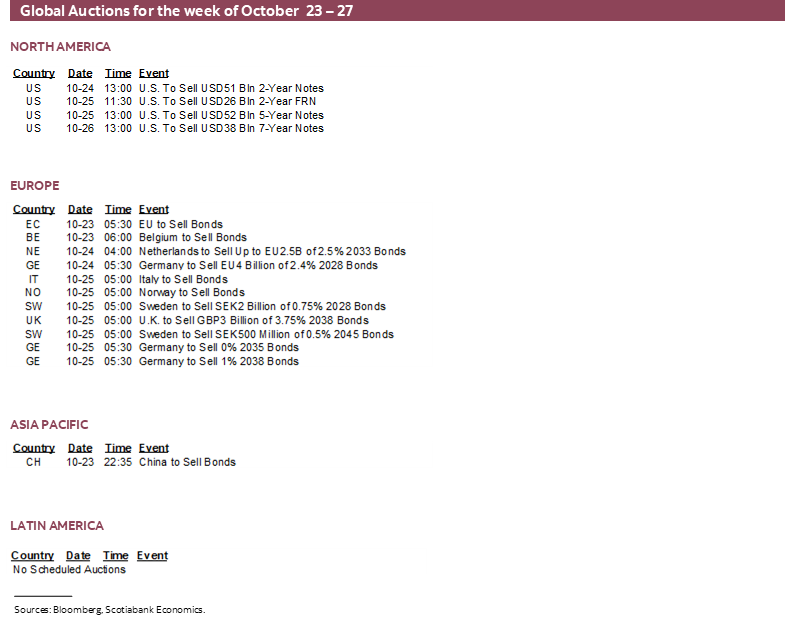

The week’s main developments other than potential geopolitical matters will focus upon the ECB’s narrative (Thursday) that may sound awfully like September’s sans forecasts this time. The Bank of Canada (Wednesday) is probably going to sound commitment phobic. Chile’s central bank is likely to continue easing with a nervous eye on the peso. Q4 GDP will showcase the US economy’s ability to mitigate some of the downside risks to the world economy while several other global indicators speak to tracking of current economic growth and inflation.

ECB—IT’S A LESS BEAUTIFUL PLAY NOW

The European Central Bank is widely expected to keep its main policy rates on hold again on Thursday. Markets are pricing no chance of a move and the consensus of forecasters is in broad agreement. No changes are expected to balance sheet plans either. After issuing fresh forecasts at the September meeting, the next update will come with the December 14th communications.

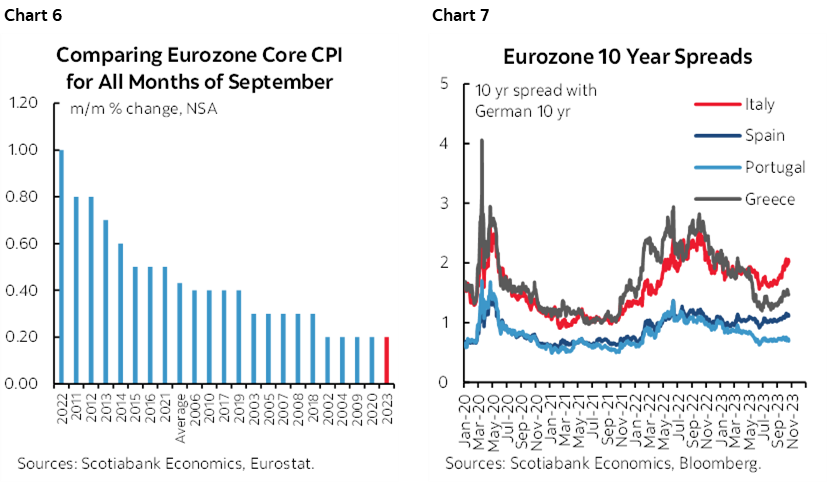

This one may be an open and shut case, especially because core CPI was quite soft since the last decision. Furthermore, bond yields have risen quite sharply, Italian and peripheral spreads have widened over bunds, and Europe’s close proximity to two wars in Ukraine and Israel plus the surrounding region amplify geopolitical risks and spillover effects (charts 6, 7).

Lagarde may sound like Fed Chair Powell and other central bankers who require evidence of persistence before becoming more concerned about bond market developments. Nevertheless, bond market developments make it very unlikely that she will broach the topic of ending reinvestments within the Pandemic Emergency Purchase Programme. The PEPP is treated as the first line of defence against spread widening across EGBs. Prior to the bond sell off, there had been rising speculation that the ECB might bring forward a previously planned end to reinvesting the PEPP’s maturing proceeds from the end of 2024. That seems rather unlikely at this point.

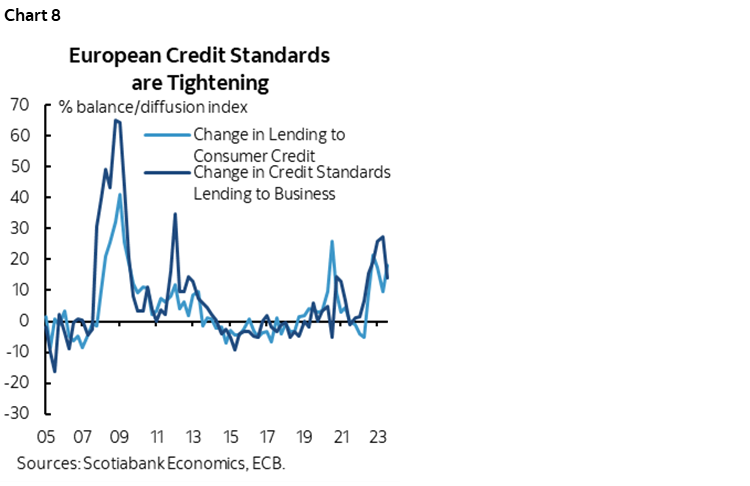

It's also worth noting that bond markets matter relatively less to European credit conditions than bank lending conditions compared to the US and Canada. Lagarde cannot, however, go too far with that argument since bank lending terms to households and businesses are also tightening (chart 8).

Key, however, is whether Lagarde preserves optionality toward possible future moves on the policy rate, or perhaps sounds more definitive by guiding a more prolonged holding period that somewhat more significantly fends off the hawks.

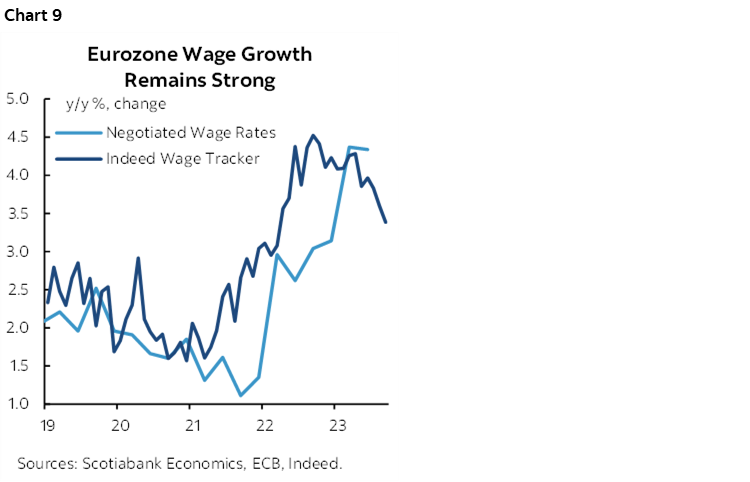

Alternatively, she may retain flexibility because the ECB will have considerably more information at its disposal by the next meeting on December 14th and a fresh opportunity to reassess staff forecasts at that time. Oil has been on the rise. And wage pressures continue to threaten (chart 9). Both of these developments suggest that inflation risk has not gone away and the ECB’s prime mandate is price stability.

For further context, it may be worth a recap of the communications that were delivered at the time of the last decision on September 14th when they hiked by another 25bps and delivered noncommittal forward guidance. The statement preserved optionality around future decisions in what read very much like a committee-written statement that tried to please everyone, hawks and doves alike. President Lagarde emphasized the precise wording of the statement and appeared to call attention to “substantial” (instead of, say, complete) and “will be set” (instead of, saying they already are) in the following sentences:

"Based on its current assessment, the Governing Council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target."

And

"The Governing Council’s future decisions will ensure that the key ECB interest rates will be set at sufficiently restrictive levels for as long as necessary."

When further pressed to opine on the prospects of additional tightening in less ambiguous terms, Lagarde shot back with a reference to a “beautiful” 1730 French play—Pierre Carlet de Chamblain de Marivaux’s “The Game of Love and Chance”—and said that saying the door must be either open or closed is theater, not central banking.

Furthermore, recall that the opening line to the statement started by emphasizing that inflation “is still expected to remain too high for too long.” The concluding paragraph emphasized that they “will continue to follow a data-dependent approach” to making decisions.

There were dissenting views at the meeting, as indicated by Lagarde’s remark that “Some members did not draw the same conclusion. Some would have preferred to pause and reserve future decisions. But I can tell you that there was a solid majority that agreed" with what was done today. If there were members that advocated a pause instead of hiking at the last meeting, then their number probably grew since then given CPI and bond market developments.

That the ECB is not discussing balance sheet adjustments was clear when Lagarde said in her September press conference that they have not discussed the Asset Purchase Programme and outright sales while the Pandemic Emergency Purchase Programme is the first line of defence in terms of flexibility in any event.

On forward guidance should the terminal rate have been reached, Lagarde said they “did not discuss how long we would need to be sufficiently restrictive. We will need to be data dependent and test data against projections.” She went on to say, somewhat defensively, that “I am not changing anything I said at Sintra” in reference to the ECB’s annual Forum on Central Banking on June 26th, and “We are not saying we are now at peak. The focus is probably going to shift a bit more to the duration, but we cannot say that we are now at peak.”

BANK OF CANADA—A COMMITMENT PHOBIC PAUSE

The Bank of Canada is widely expected to hold its policy rate unchanged at 5% on Wednesday. It will deliver a statement and full forecast update in the Monetary Policy Report at 10amET. Governor Macklem and Senior Deputy Governor Rogers will host a press conference about one hour later.

I also expect the statement to retain reference to how “Governing Council remains concerned about the persistence of underlying inflationary pressures, and is prepared to increase the policy interest rate further if needed.” Such guidance is likely to remain highly data dependent.

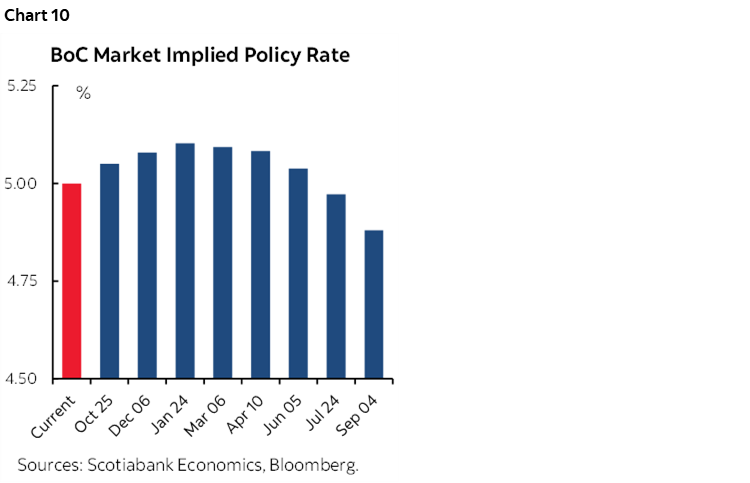

One reason for this bias continues to be market management. Markets being markets would pounce upon a clearer signal that the central bank thinks it is done and could move more aggressively toward pricing rate cuts. It’s too soon for the Governing Council to be open to such a discussion. At present, volatile markets are pricing modest risk of a further rate hike, so to signal otherwise could ease financial conditions (chart 10).

But are financial conditions excessively tight when judged through the lens of Governing Council? Macklem’s recent remarks at IMF and World Bank meetings in Morocco indicated that he thinks higher bond yields reflect central bank guidance and hence they are not a substitute for tighter monetary policy rather than reflecting such expectations. That suggests he does not think bond market conditions have become excessively tight relative to their intentions. He did, however, also note that recent bond market developments could be taken into account during deliberations.

One reason Macklem can adopt this posture more so than, say, the Federal Reserve, is because of the shorter terms in Canadian mortgage markets. The BoC is less concerned about, say, the 10-year segment of the curve that drives pricing for US mortgages before tacking on spreads. The BoC’s policy rate influences are concentrated in shorter-term rates but can influence yields through the belly of the curve which is the sweet spot for fixed term mortgages in Canada.

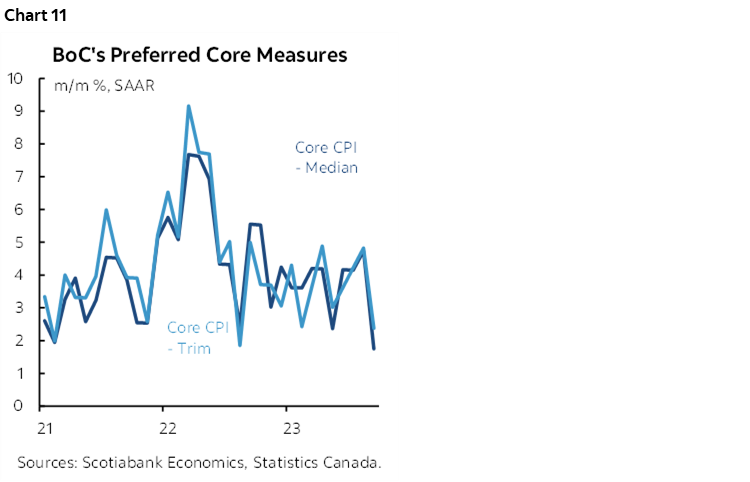

Another, more dominant rationale for a continued tightening bias is that inflation risk remains slanted higher notwithstanding the first indication that underlying inflation softened in September (chart 11). Those arguments have not gone away after a single, solitary CPI report that keeps a three month moving average still well above the BoC’s 2% headline CPI target over the medium-term. I don’t see any reason for Governor Macklem to drop his prior line about how the easy part of the disinflationary experience has been achieved and that the next phase is going to be more challenging. Some of the reasons are as follows.

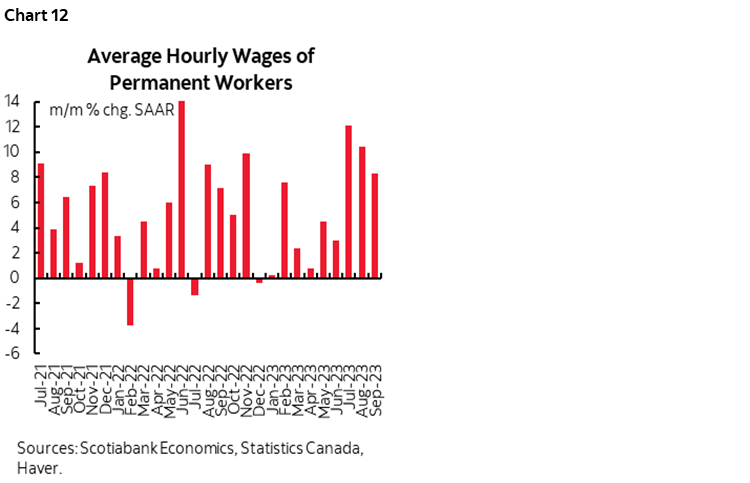

Wage growth is explosive (chart 12) and has been outpacing inflation for over a year now. Wage growth has also been vastly outpacing labour productivity that itself has been tumbling throughout the pandemic.

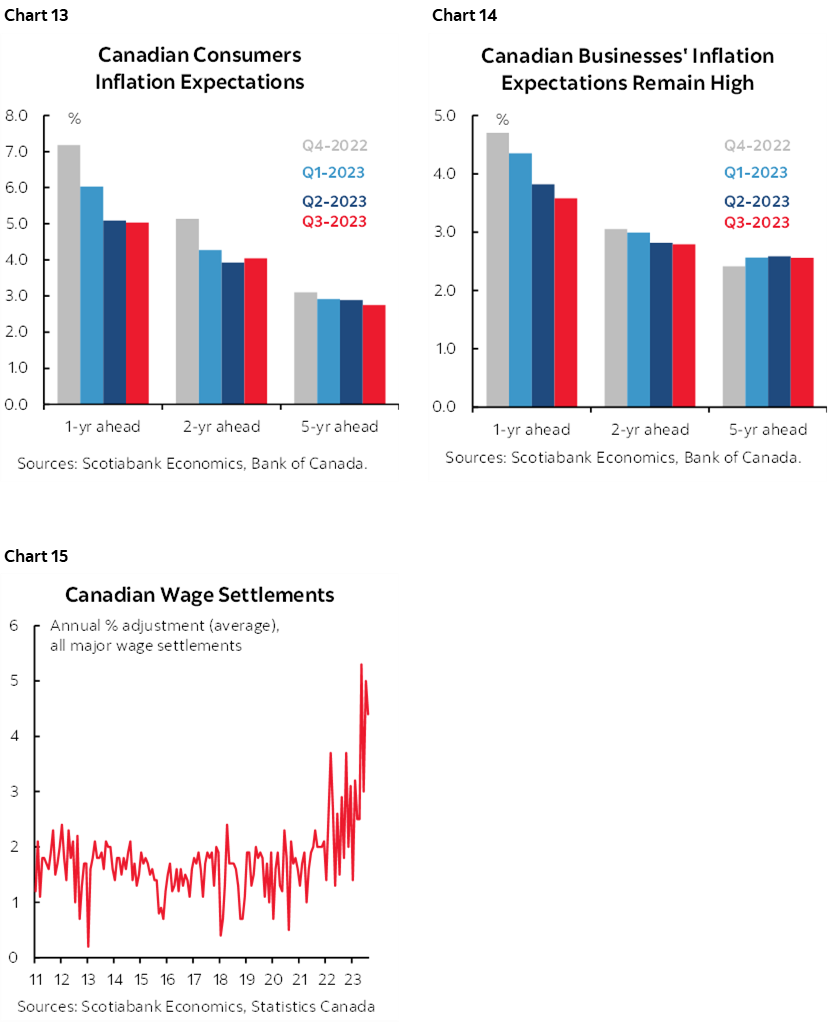

This past week’s updated surveys show that inflation expectations remain unmoored (charts 13, 14). Workers in a country where one-in-three are unionized and resetting wages higher through multi-year contracts are signalling changed behaviour because they don’t believe that the BoC will be able to durably achieve 2% inflation (chart 15).

The terms of trade remains supportive of the economy by presenting an imported positive income shock with trickle down benefits. High oil prices on Middle East tensions are supportive and important to an oil producing and exporting country like Canada.

We do not as yet know how supply chains may evolve in the face of geopolitical tensions across multiple theaters. We cannot rule out another round of disruptive effects to global production on top of the risk of a bigger oil price shock. Domestic supply chains remain constrained in key sectors like housing and autos that are experiencing tight inventories.

Fiscal policy remains excessively stimulative and with risk of becoming more so as previously announced spending plans continue to get rolled out, as new measures targeting housing are added, and should demands for added spending become further amplified, such as a highly contentious national pharmacare program.

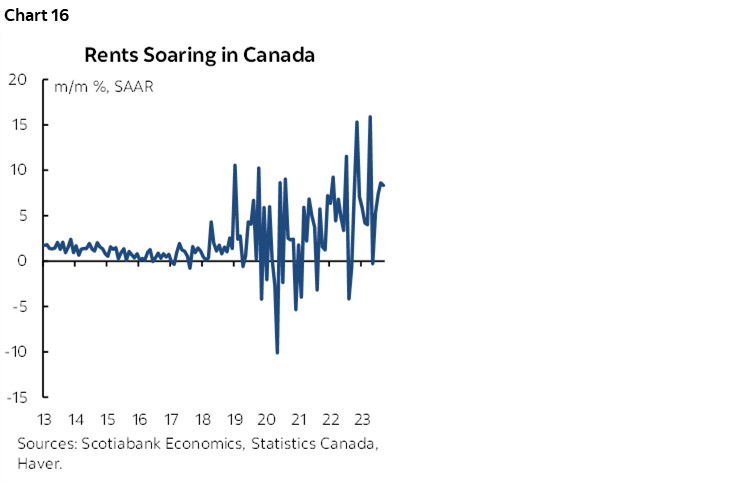

Immigration is well in excess of the country’s ability to absorb new arrivals relative to its ability to provide shelter and other necessities without stoking ongoing price pressures. Rent is one obvious example that is being driven higher by residents hesitant to enter owner occupied housing markets, plus new arrivals (chart 16).

The US economy continues to vastly outpace forecasts for a fifth consecutive quarter. There remain solid arguments in favour of further resilience.

The Canadian dollar is significantly undervalued.

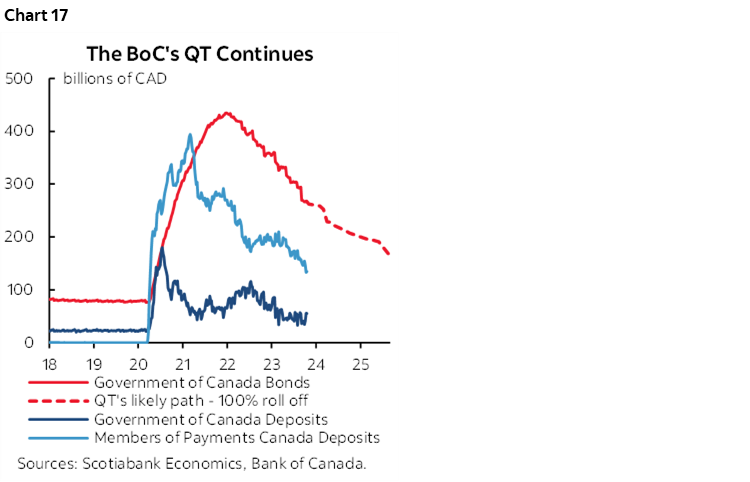

The BoC will also continue along with its quantitative tightening program that entails allowing full roll-off of maturing Government of Canada bonds that dominate its balance sheet. Chart 17 depicts the projected trajectory of its holdings should the BoC continue to allow 0% reinvestment of maturing holdings. An objective of QT plans is to tighten funding conditions for banks and with that deposits of Members of Payments Canada, also shown on the chart. Expect Macklem to be asked whether the prospect of surging debt issuance as deficits deteriorate complicates aggressive withdrawal from the bond market by the BoC. I would expect him to stand by QT plans and remind us that balance sheet tweaks are not supposed to be about accommodating debt issuance in well functioning markets. Balance sheet tools like bond buying are supposed to be confined to moments when markets are dysfunctional and especially when the policy rate is constrained by a lower bound that is probably positive in Canada’s financial system.

As for forecasts, the MPR may downgrade growth projections relative to the projections that were offered in July. It’s very unlikely that we’ll hear the ‘R’ word from them. Their 1.8% Q4/Q4 2023 real GDP forecast is somewhat above what is more likely to come in at around 1% by our estimates. By contrast, however, they may need to revise up their 2.9% Q4/Q4 CPI projection for this year toward being materially above 3%.

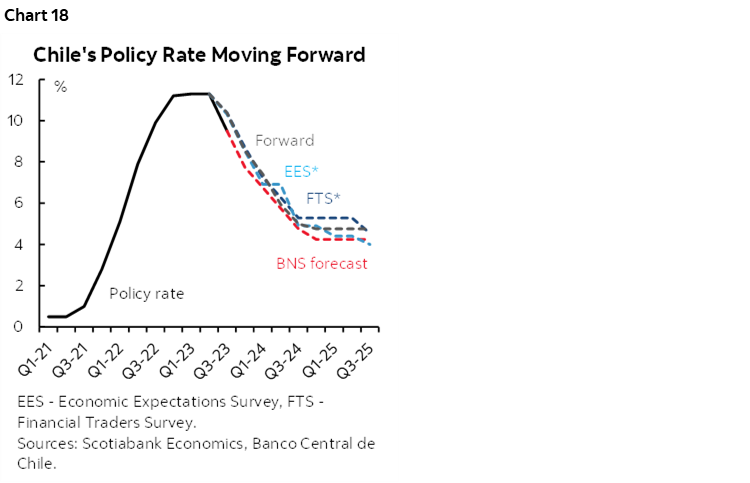

BANCO CENTRAL DE CHILE—FRESH WRINKLES TO THE PLAN?

Another 75bps reduction with 100bps risk is expected on Thursday. That would take the overnight rate down to 8.75% for a cumulative 250bps of easing since it began in July. Fresh forecasts were delivered in September with the next batch due in December.

Inflation has continued to ease since the prior 75bps reduction on September 5th, landing at 5.1% y/y and 6.6% ex-volatile items in September. The central bank has said it expects inflation to converge upon the 3% target by 2024H2. Policy easing today is viewed as necessary to land upon the target instead of undershooting it by that time, assuming they or anyone else can forecast inflation that far out which I’ll return to in a moment.

Forward guidance in September, that was extended from June's quarterly projections and July’s meeting, indicated openness to at least 75bp reductions in each of the decisions in October and December. The September MPR stated that if developments unfold as expected, then the BCCh will reduce the policy rate to between 7.75% and 8% from 9.5% at present. This implies risk of one of those moves being another -100bps reduction like the one that began easing in July. Chart 18 shows the longer run expected path.

To upsize once again at these meetings—or perhaps even to deliver back-to-back 75bps moves—would have to be driven by conviction that inflation is tumbling at least as quickly if not faster than anticipated. That could be viewed with fresh skepticism. For one thing, volatile commodity, and especially oil prices, add uncertainty, although copper prices have been softening. For another, the Chilean peso has depreciated by another roughly 7% to the USD since the last cut and is the worst performer among major LatAm crosses. The peso has depreciated by about 15% since last June, second only to the Argentine peso among the worst LatAm performers. Such performance raises risks to imported inflation.

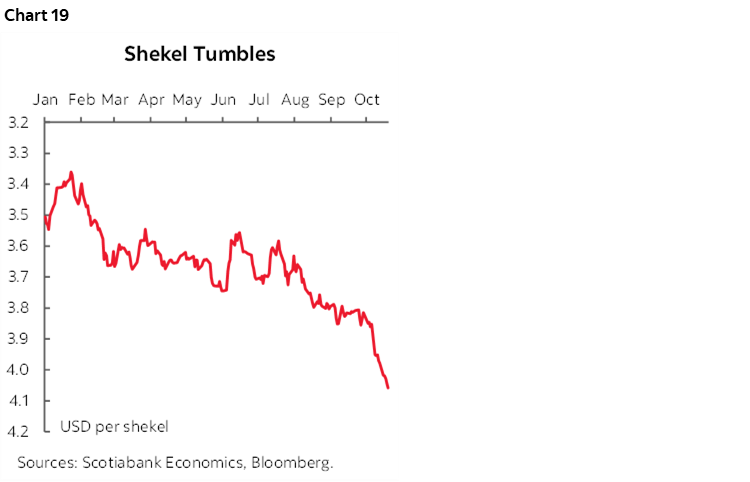

BANK OF ISRAEL—TUMBLING SHEKEL LIMITS OPTIONS

Israel’s central bank will deliver a previously scheduled policy decision on Monday. A hold is widely expected.

Intuitively, perhaps one might think that a war is a prime opportunity to ease monetary policy. That logic had been prompting a minority of forecasters to anticipate easing, although they have since revised this view. The offset is that it’s also typically a reason to sell the currency. The shekel has been tumbling (chart 19). This has prompted Deputy Governor Andrew Abir to guide that the central bank wishes to avoid anything that would further destabilize the currency as it continues to intervene in open markets.

CENTRAL BANK OF THE REPUBLIC OF TURKEY

Major increases in the repo rate since June that have totalled 225bps to a one-week repo rate of 30% have done nothing to stem the tide of a weakening currency and concomitant effects upon imported inflation. That might not stop the central bank from trying it again on Thursday, as the market signal may well be that the damage to Turkey's central bank credibility and underlying inflationary forces are so powerful that they merit significant further tightening.

CENTRAL BANK OF THE RUSSIAN FEDERATION

There is significant risk of a further rate hike on Friday. The last decision to raise the key rate by 100bps on September 15th was accompanied by guidance that there may be another hike at a coming meeting. Since then, CPI climbed by more than expected to 6% y/y with core CPI increasing to 4.6%. The ruble has also weakened since the last hike, thereby further raising inflation risk.

GLOBAL MACRO—IN A CLASS BY ITSELF

The strength of the US economy, an updated batch of global purchasing managers indices and several inflation reports will dominate the fundamentals calendar over the coming week. Earnings season will remain a heavy focus.

The week kicks off with multiple countries releasing purchasing managers’ indices. Australia and Japan typically kick it off each month and will release on Monday evening eastern time. Each of the Eurozone, UK and US will update their own readings the next day. The readings are correlated with in-quarter GDP growth and therefore fresh, provide soft data evidence on economic momentum. Details also inform supply chain developments.

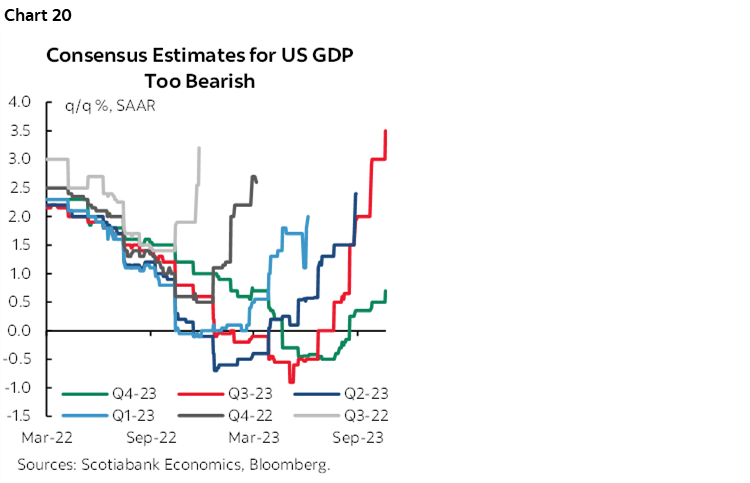

US Q3 GDP arrives Thursday. Scotiabank Economics figures that the economy grew by around 4% q/q at a seasonally adjusted and annualized pace. That would make for the fifth consecutive quarter in which consensus has had to sharply revise estimates higher (chart 20). The US economy continues to grow much faster than the noninflationary speed limit, or potential GDP growth. It’s also outpacing many other major industrialized economies. Consumer spending is expected to figure prominently as a key driver of such strength ahead of the key holiday shopping season.

A batch of key global inflation readings will consist of the following:

- US core PCE: Friday’s update for September is likely to closely follow the already known up-tick in core CPI to 0.3% m/m SA.

- Tokyo CPI: Watch this gauge on Thursday evening eastern time. The Bank of Japan delivers a policy decision on Halloween amid speculation that it might abandon negative rates by raising its -0.1% policy balance rate. Tokyo CPI is fresher than national CPI but highly correlated. Any surprise up-tick could further inform such policy expectations.

- Australian CPI: The Q3 print arrives on Tuesday evening (ET). A seasonally unadjusted rise of 1.1% q/q nonannualized is expected. Similar gains are expected for weighted median and trimmed mean CPI that weed out the more volatile and often commodity-derived components. The RBA delivers another policy decision on November 6th. At present, markets are pricing around a one-in-four chance of a rate hike, particularly in the wake of new Governor Bullock’s recent remarks. Bullock recently remarked that “it’s going to be difficult to get inflation down.” Any upside surprise in underlying inflation would only add to such difficulties and perhaps her stance.

The UK is updating its labour market readings in two waves this time. It already released payrolls for September and wages for August, both of which slipped. Next up is the total employment report for August that factors in a more complete accounting of small business employment conditions. Overall employment has been mildly slipping of late.

Other US macro readings will include durable goods orders that will probably soar on nondefence airplane orders given the surge on Boeing’s order book (Thursday). New home sales (Wednesday) have been more resilient than resales, partly because people don’t want to move and give up their juicy mortgage rates and so the housing stock is expanding.

Other key readings will include South Korean Q3 GDP (Wednesday). Spanish Q3 GDP (Friday) leads off the path to the next Eurozone GDP report with other countries releasing the following week. China reports monthly industrial profits for September (Thursday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.