Next Week's Risk Dashboard

- Central bank divergence will be on full display

- RBA under hike pressure

- BoE to hold, inform path forward

- Banxico likely to pause ahead of election

- Peru’s central bank expected to cut

- Will Brazil’s central bank downshift the pace of easing?

- Sweden’s Riksbank could cut

- Bank Negara to hold

- France kicks off the ECB’s wage watch ahead of the June meeting

- Canadian jobs rebound?

- Canada’s job market is rebalancing…

- …but that doesn’t mean wage pressures will go away

- Are US lending conditions still tightening?

- UK GDP expected to accelerate

- CPI: Chile, Colombia, Mexico, Brazil, Norway, Philippines, China, Taiwan, Thailand

- US macro risk goes quiet

Chart of the Week

This will be a fascinating week during which to monitor the risk of policy divergence across a significant array of global central banks not named the Fed, ECB or BoJ. Some could cut, some could hold and sound patient, some could hold and guide cuts, and one is faced with markets thinking it could resume hikes. A Fed-obsessed world has lost sight of the scope of greater relative central bank divergence. There is a gambling analogy here as central banks continue to deal with high uncertainties; like the song goes, knowing when to hold ‘em, fold ‘em, walk away or run will separate the central banks that choose the right path from the ones that mess up.

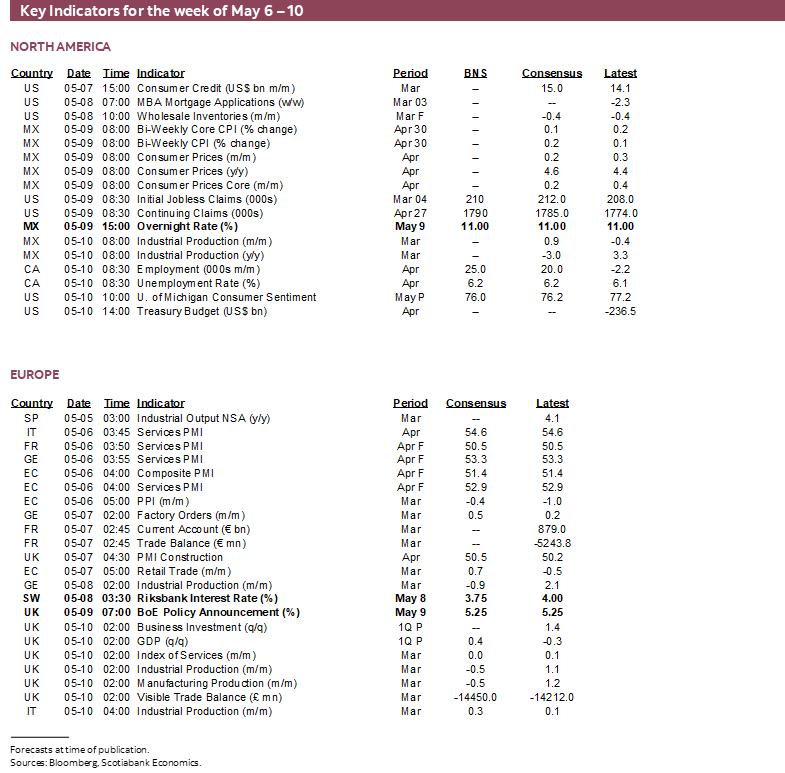

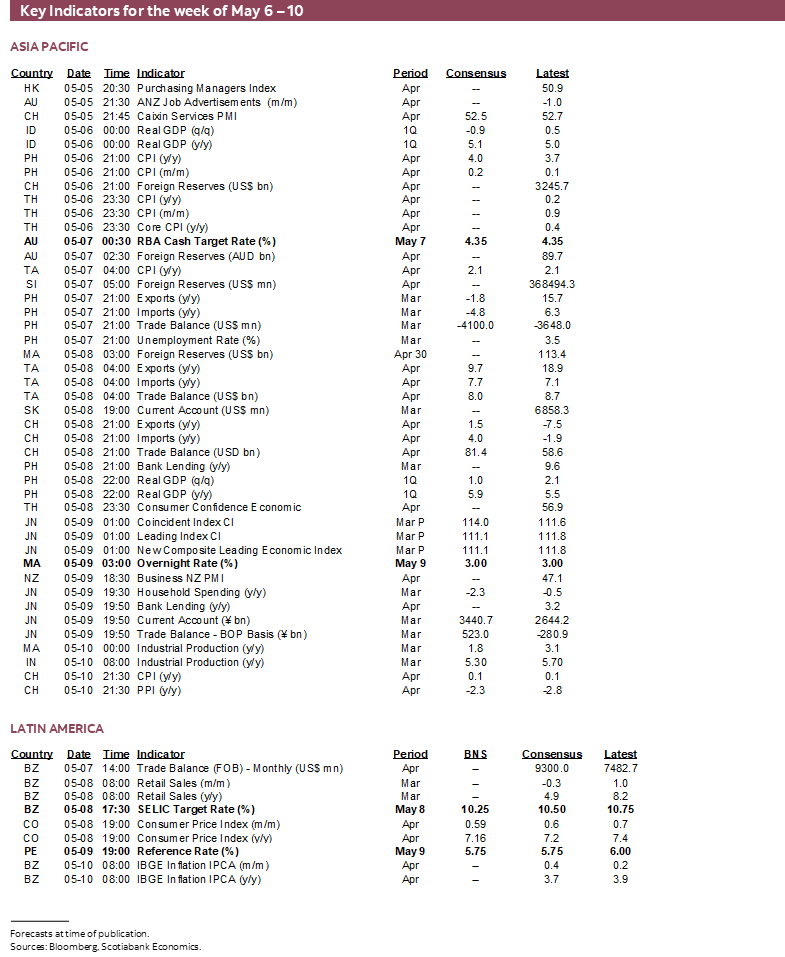

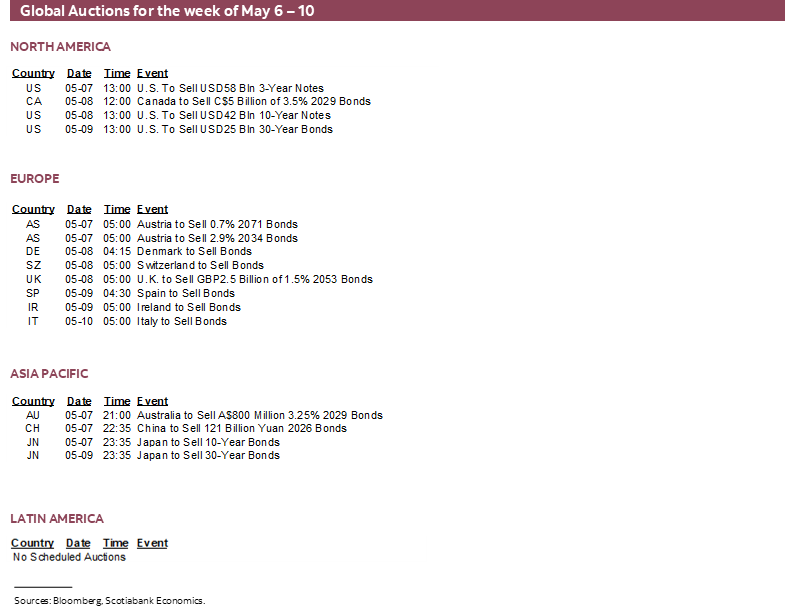

The global macro calendar will be lighter than it has been of late, but still populated by some key gauges. Canadian jobs and wages for one. The start of tracking Eurozone wages ahead of the June ECB decision for another. Are US credit conditions still tightening and adding to downside risk to growth? We’ll find out at the start of the week. Canada may take further steps around implementing the Federal Budget as tensions with India flare. US-centric macro risk should be very low this week amid light calendar-based developments. The health of the UK economy will be a focal point at the end of the week. A round of global inflation reports is also due out with implications for regional markets.

CENTRAL BANKS—CUTS, HOLDS, KEY GUIDANCE AND…A HIKE??

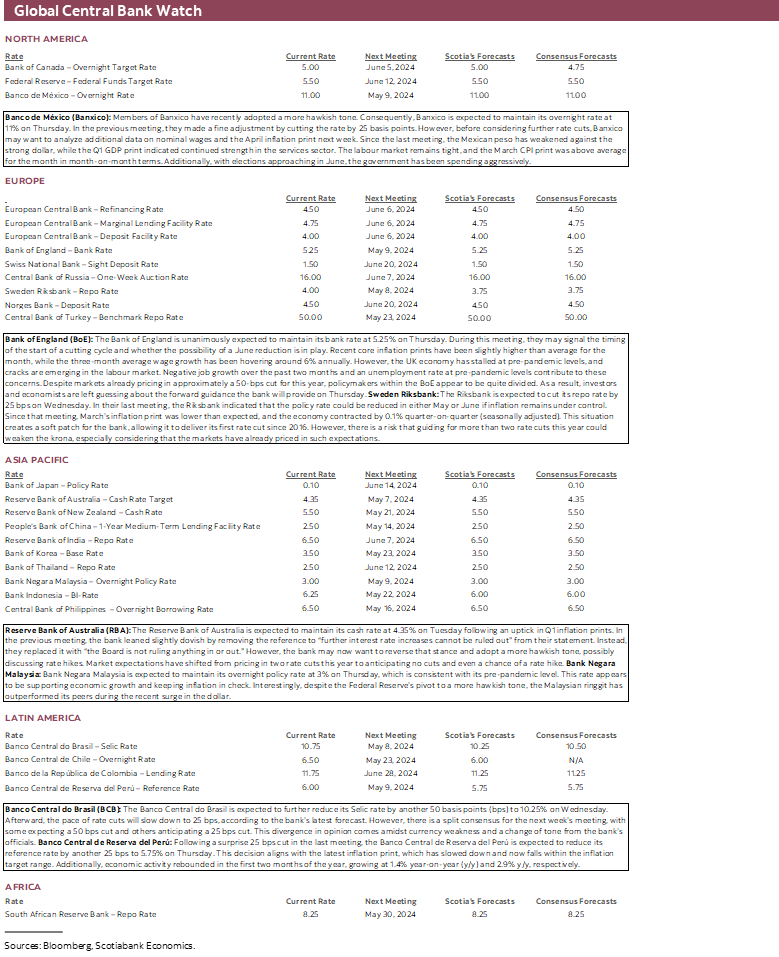

This will be a big week for central banks not named the Fed, ECB or Bank of Japan. Seven banks will weigh in with policy decisions. Three might cut, two are expected to hold but might guide future cuts, one will hold outright and one is dealing with market sentiment that thinks the next move is more likely to be a hike.

Brief expectations are outlined in chronological order:

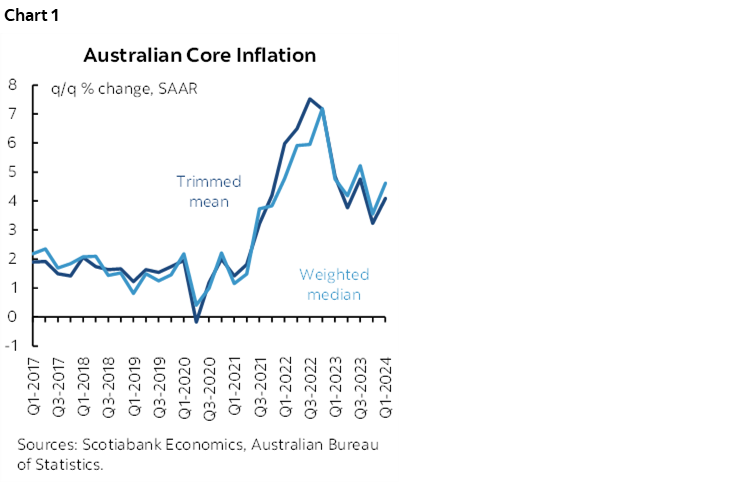

- RBA (Monday): No one seriously expects a policy rate change at this meeting. One person out of 24 thinks they’ll hike. Markets have nothing priced, so it would be a total surprise in an environment in which surprises are probably unwise. Markets are pricing most of a 25bps rate hike by the September meeting. The motivating consideration for additional tightening is persistent inflation after Q1 core measures surprised higher than expected (chart 1). Trimmed mean CPI increased by almost 4% q/q SAAR with weighted median CPI up by 4.6% q/q SAAR. Such a pace of underlying inflationary pressure is incompatible with achieving the RBA’s 2–3% headline CPI target range. This will be the first meeting in reaction to the inflation readings.

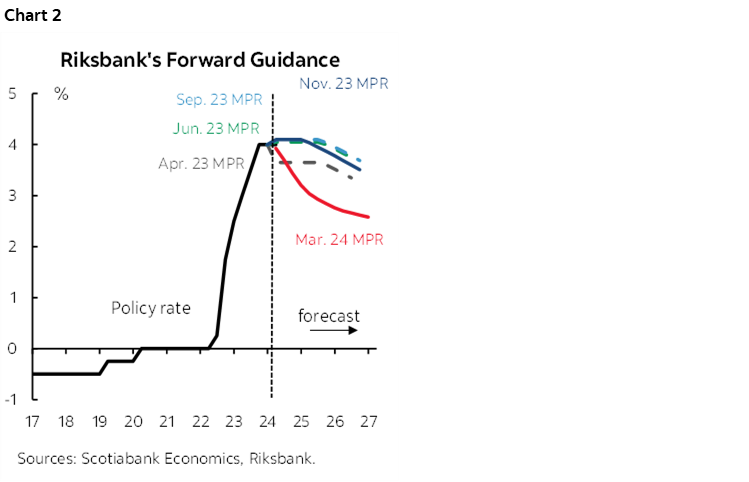

- Riksbank (Wednesday): Consensus is divided over whether Sweden’s central bank may begin an easing cycle this week. A little over half of forecasters in a modest sample of 13 expect a 25bps cut. Six are not convinced. The uncertainty mostly rests upon whether they would cut at this meeting or the next one in June after the central bank said in its March statement that “If the inflation prospects remain favourable, the policy rate may well be cut in May or June” and the published forward rate path showed an expedited pace of easing (chart 2). Since then, underlying inflation came in materially weaker than expected for March at 0% m/m ex-energy (0.3% consensus) and the year-over-year rate fell beneath 3% at 2.9% for the first time since early 2022 while remaining on a steep downward descent.

- Banco Central do Brasil (Wednesday): Brazil’s central bank has been on auto pilot to date. 50 has been their favourite number as they have cut by this magnitude six consecutive times in lowering the Selic rate from 12.75% over a year ago to 10.75% now. This time, however, more forecasters expect a 25bps downshift in the pace of easing than another 50bps cut. Currency volatility is one consideration as the real fell sharply earlier in April but has since regained its footing.

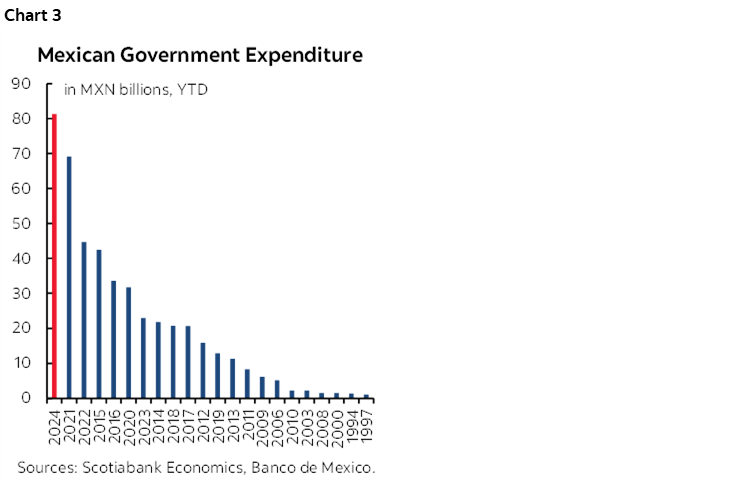

- Banxico (Thursday): All but one out of 16 forecasters expect Mexico’s central bank to hold its overnight rate unchanged at 11% on Thursday. This follows the 25bps cut on March 21st that was strongly telegraphed in advance. The peso has depreciated by about 4% to the USD since earlier in April as expectations for rate cuts by the Federal Reserve were pushed out. This is likely to keep the Governing Board led by Governor Victoria Rodríguez Ceja sounding careful but with an ongoing forward easing bias conditional upon CPI that arrives on the morning of Banxico’s decision. Complicating matters is strong fiscal easing ahead of June elections (chart 3).

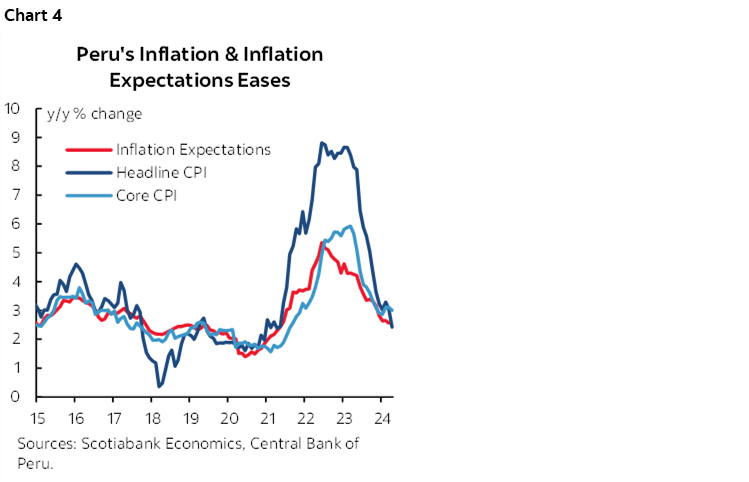

- BCRP (Thursday): Most forecasters expect another 25bps cut by Banco Central de Reserva del Peru on Thursday. That would extend the easing path that started in September at a -25bps pace from 7.75% to a policy reference rate of 6% now. Inflation recently surprised lower in April with the Lima CPI reading falling to 2.4% y/y (3.1% prior, 2.7% consensus) to the lowest reading since about mid-2021 before a big surge of inflationary pressure began to unfold (chart 4).

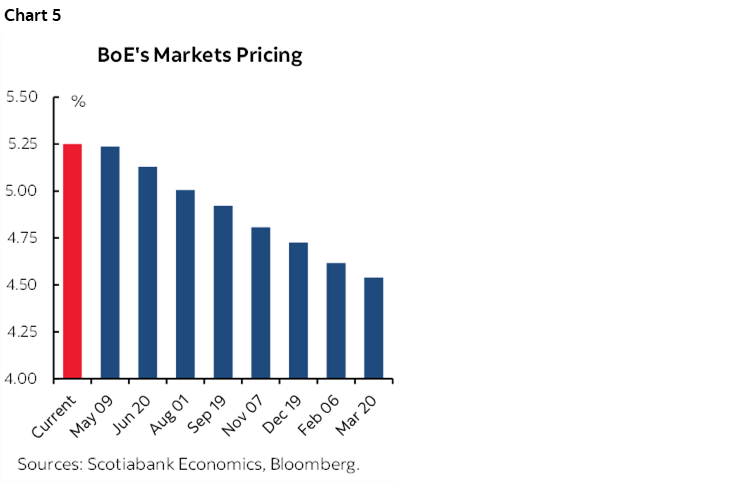

- Bank of England (Thursday): Consensus and markets unanimously expect Bank Rate to be held at 5.25% on Thursday. Key will be forward guidance as markets are pricing a 50–50 chance at a 25bps cut at the next decision on June 20th and a full 25bps reduction by the next meeting on August 1st followed by a path of gradual easing (chart 5).

- Bank Negara Malaysia (Thursday): Malaysia’s central bank is widely expected to continue holding its overnight policy rate at 3% on Thursday. Watch forward guidance, however, as inflation at 1.8% y/y is low and the ringgit has been relatively stable.

WAGE WATCH AT THE ECB

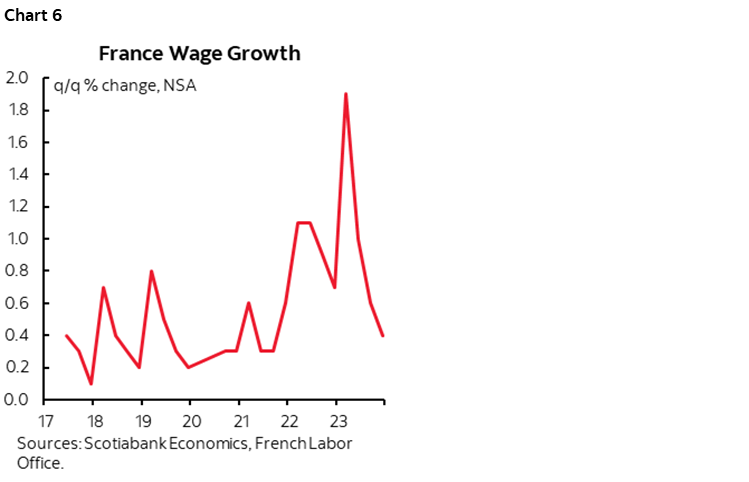

A key consideration for the ECB as it considers whether to ease at the June meeting is wage growth. The figures are not seasonally adjusted and that matters because collective bargaining has its biggest effects during Q1. We see that in the French figures that post clear seasonality with the biggest gains in Q1 each year (chart 6). A key sensitivity for the ECB is whether this year will repeat or come close to the magnitude of the gains witnessed over the past couple of years.

The ECB’s concern is that if negotiated wage rates continue their steep ascent (chart 7) then it could be more difficult to get inflation risk under control. Given high proportions of Euro area countries subject to collective bargaining exercises (chart 8), the wage resets in these agreements could be more powerful influences than indicates that wage growth for new job postings has been ebbing (chart 9).

CANADA’S JOB MARKET—A FIRST STEP TO THE JUNE BOC MEETING

Canada updates jobs, wages and other labour market readings within the household survey for April on Friday. It will be the only calendar-based form of macro risk to the Canadian market this week.

I went with a gain of 25k in April and a slight up-tick in the unemployment rate to 6.2% on the view that continued rapid population growth will drive greater growth in the labour force than employment. For instance, the labour force grew by 58k in March and 76k the month before that and has averaged 37k new entrants in search of work per month since the start of 2022 when the immigration surge began.

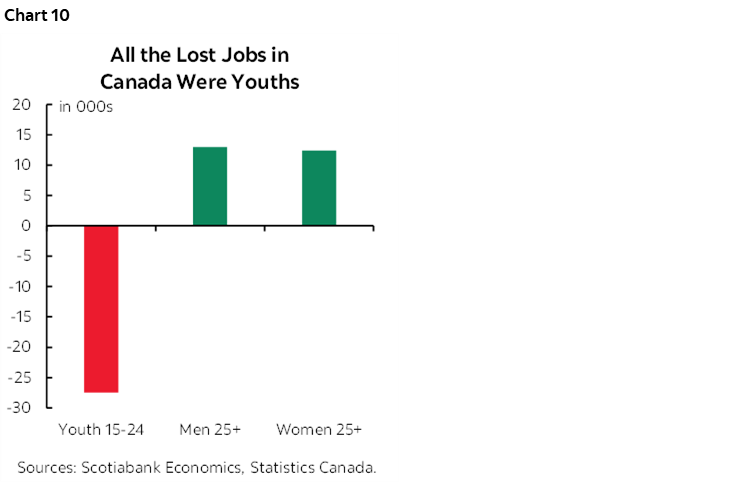

Why a rebound in job growth? I’m loosely going with a narrative that says the prior month’s distorted softness should stabilize or reverse and feed the condition for a rebound in April. A key driver of weakness in March was the youth category. Those aged 15–24 lost 28k jobs that month while men and women aged 25+ both saw significant gains (chart 10). That could have been a March break timing issue relative to the reference week for the LFS survey which was the week of March 10th to the 16th. Spring break occurred in Quebec and New Brunswick before that week, while it was later than that week in BC, Alberta, Saskatchewan, Manitoba, Newfoundland and Labrador and PEI. Provinces with Spring breaks outside of the LFS reference week accounted for about 80% of the ‘lost’ youth jobs in March.

Unlike other macro indicators, however, the LFS should not be impacted by the different timing of the Good Friday and Easter holidays since they landed in between the March and April LFS reference weeks and therefore should not have spawned debate about whether the seasonal factors would control for this.

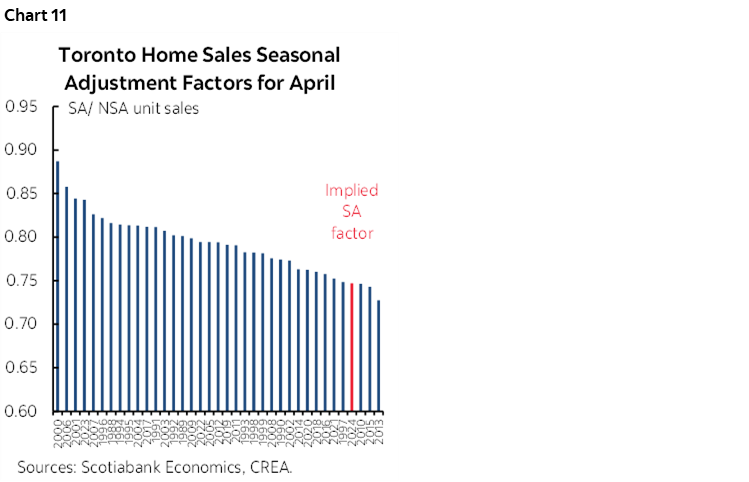

Even in other cases it’s unclear what’s going on with some SA factors. Take Toronto’s existing home sales figures. Real estate agents still worked and were available throughout the Good Friday and Easter holiday weekend so it’s unclear how many sales were lost due to the holiday and pushed into April instead, and yet the Toronto Real Estate Board applied one of the lowest SA factors for a month of April on record while reporting a sales decline of over 3% m/m SA (chart 11). Going with a higher SA factor more in line with history would have registered an SA gain in April.

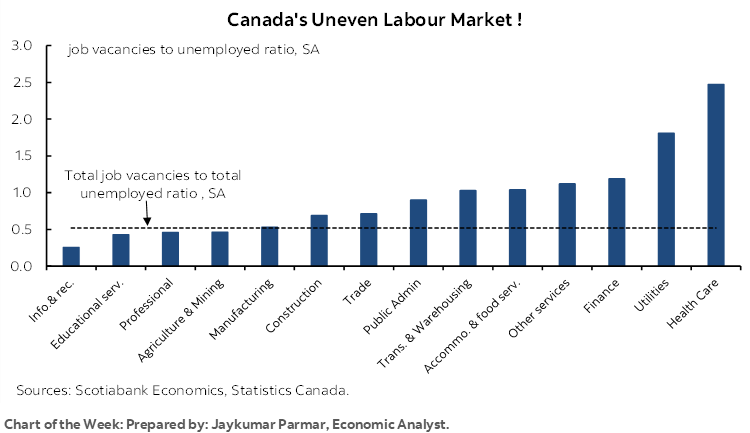

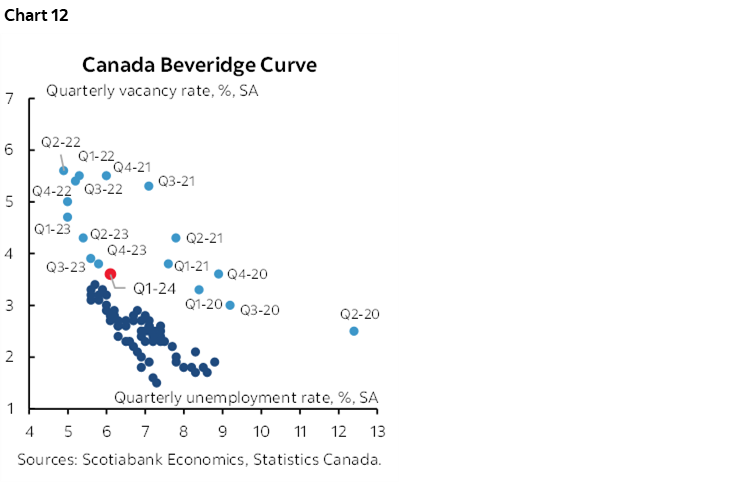

In any event, Canada’s labour market is gradually rebalancing. We see that in measures like the so-called Beveridge curve that relates job vacancies to unemployment rates over time (chart 12). The extreme imbalances in the upper left of the chart back in 2022 (ie: high vacancies, low unemployment) are gradually giving way to the red dot showing 2024Q1 and more of a movement toward less excess demand for labour.

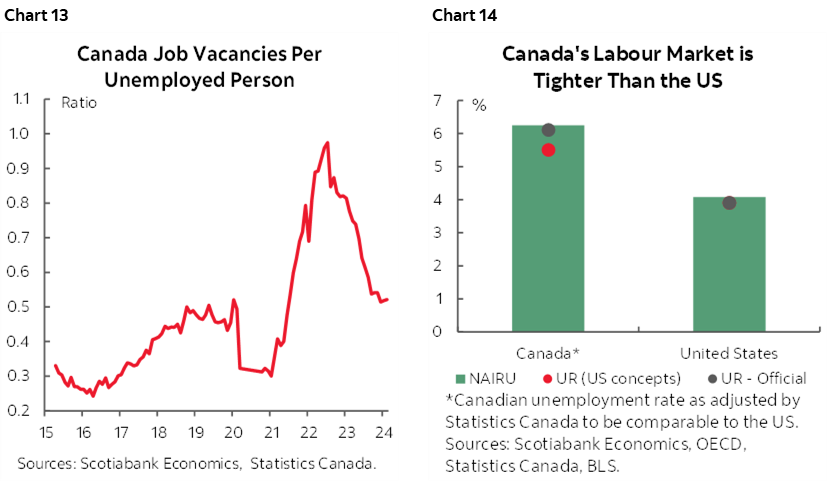

The same is true in chart 13 that makes the same point in a slightly different way. And chart 14 shows that the official unemployment rate is now close to the OECD’s guesstimate for Canada’s natural equilibrium rate of unemployment that speaks to the rate at which the labour market would be judged to be in equilibrium given structural factors.

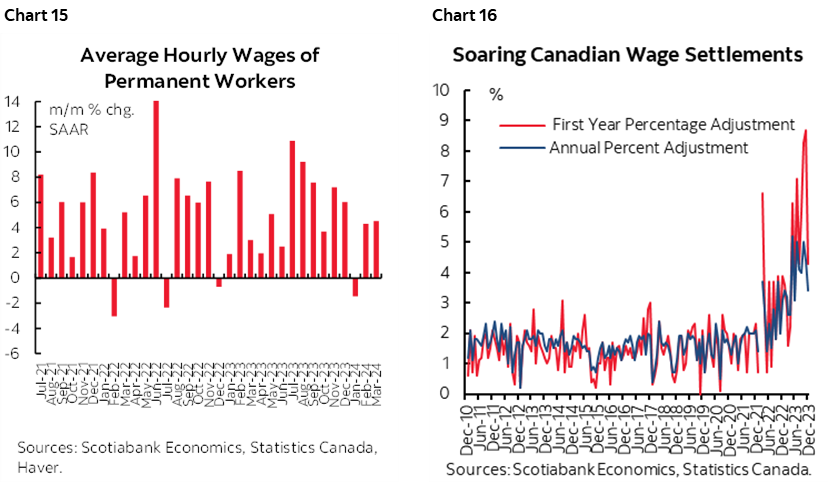

That could mean that wage growth may soon peak, but it isn’t yet as the pace of m/m seasonally adjusted wage gains at an annualized rate is still tracking at about double the Bank of Canada’s 2% inflation target (chart 15). Furthermore, Canada is still in the midst of a wave of renegotiations of expiring labour contracts in a labour market in which one-in-three workers are unionized (10% in the US). The trend in wage settlements remains pointed sharply higher and since it sets wages for coming years this has yet to begin showing up in backward-looking wage data (chart 16). The unfortunate thing about wage settlements data is how long it takes the government to report the figures as they only go up to December.

It might not peak either. The narrative that more unemployed new arrivals will drive wage growth lower is somewhat naïve. For one, it ignores the role of collective bargaining that is a much bigger issue in Canada. For another, it assumes that the new arrivals are direct competition for the rest of the workforce rather than reflecting a different blend of skilled and unskilled workers. Another point is that there may be lags as new arrivals find work while it’s unclear at what wages.

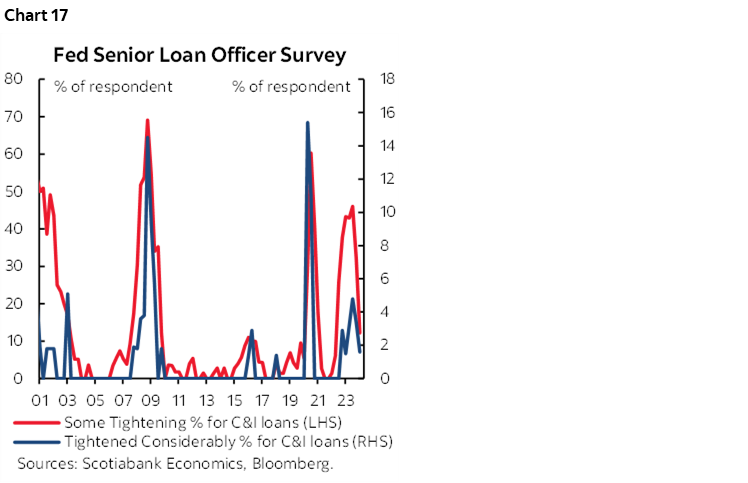

ARE US CREDIT CONDITIONS STILL TIGHTENING?

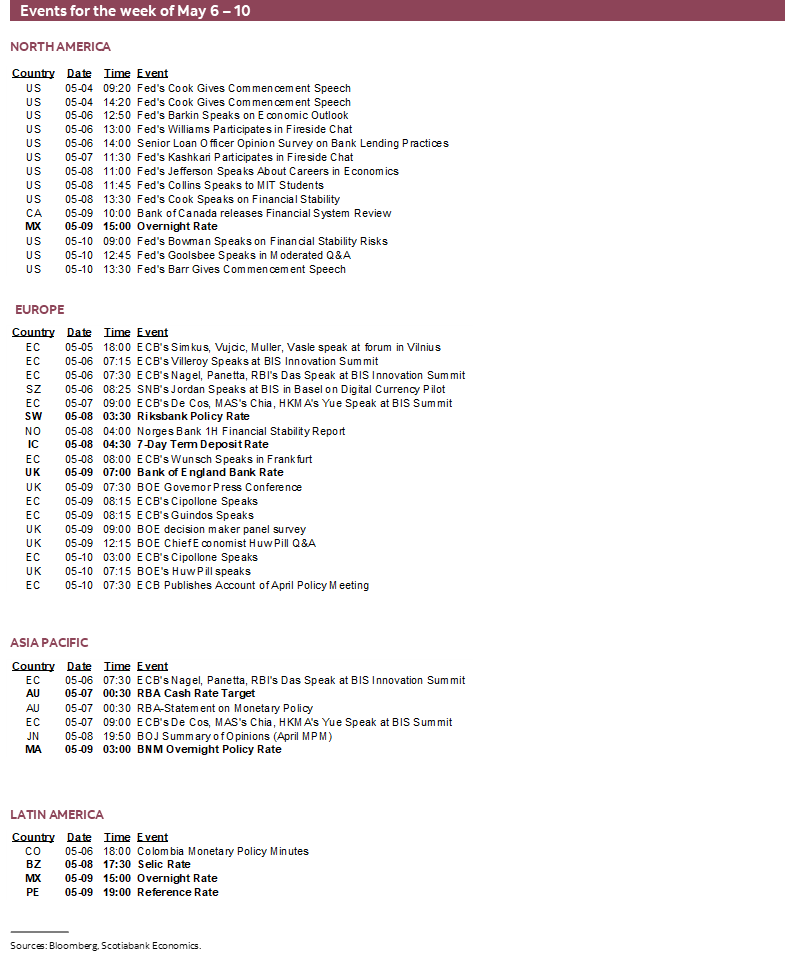

The Federal Reserve’s quarterly Senior Loan Officer Opinion Survey on Bank Lending Practices will be updated on Monday. It helps to inform credit conditions through the lens of lenders (as opposed to financial markets). It’s unlikely that there will be sizeable market effects, but the survey informs Fed thinking on credit conditions and therefore serves as input into discussing the path for monetary policy.

The prior edition for January covering responses over the December 18th to January 9th period (here and here) was released way back on February 5th. This updated survey will cover responses from late March to early April. Much of the recent bond market sell off and pushed-out easing bets accelerated after that period. Since late March, markets have reduced pricing for cumulative Fed rate cuts this year by half a percentage point and the 10-year Treasury yield has gone up by almost as much.

The last survey continued to show tightening standards at an ebbing pace for commercial and industrial loans (chart 17), commercial real estate loans and consumer loans, but easing conditions for residential mortgages. Since then, the 30-year fixed mortgage rate has increased and this may translate into tightened mortgage lending conditions not fully captured in Monday’s release. Mortgage lending rates have risen further since.

The surveys matter because of evidence that tighter lending conditions can negatively impact broad GDP growth (examples, here, here).

Tighter credit conditions and their lagging effects on growth are part of the reason why markets should not give up on the narrative of slowing US GDP growth. Other parts include ebbing fiscal policy contributions to growth, the strong dollar’s lagging effects on US net trade in a softly growing global economy, recent tightening of financial conditions including the fact that rate cut pricing for this year has been dramatically reduced,

GLOBAL MACRO—A BIG WEEK FOR THE UK

The global calendar of macro indicator releases will be on the lighter side this week, but there will still be a few gems.

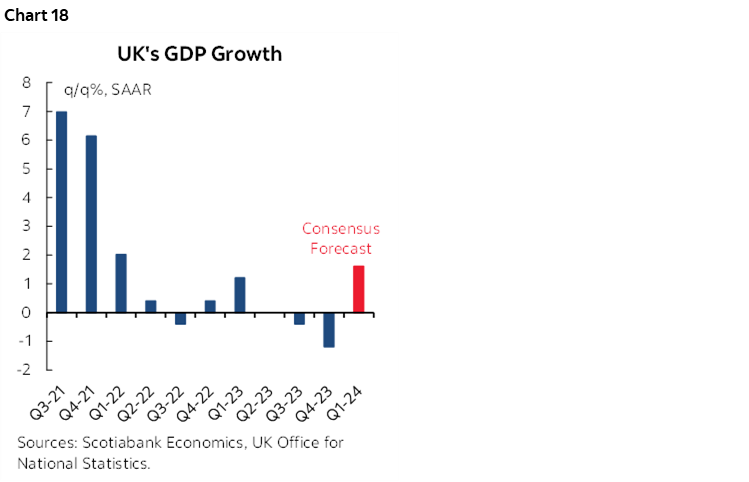

UK GDP Follows the BoE

This will be a big week for the UK not only in terms of the Bank of England’s decision but also macro releases. Q1 GDP on Friday is expected to post a gentle rebound from the prior quarter’s soft patch (chart 18). Higher frequency gauges for March will inform mathematical hand-off effects into Q2 with updates on industrial production that could step back from the prior month’s gain, and an expected flat reading for the services sector plus trade readings.

Global Inflation

A round of inflation reports will be offered by several predominantly Asian and LatAm countries. China’s CPI update doesn’t arrive until next Friday evening. Chile and Colombia (Wednesday), Mexico (Thursday) and Brazil (Friday) will release after Thailand, Philippines and Taiwan early in the week. Norway’s figures on Friday follow Norges Bank’s recent guidance against nearer term easing.

China also updates exports and imports for April by Thursday and we might get the latest batch of monthly financing figures for April either this week or the following week.

Canada—Beyond Jobs

Canada will be mostly focused upon the aforementioned jobs report with little else on the docket.

Watch for implementing legislation for the Federal government’s plan to increase taxes on capital gains and movement toward a parliamentary vote on the budget. This editorial from a guy who knows a thing or two about taxes should be read by anyone and everyone who thinks the relatively well off are tax freeloaders and that includes everyone in Cabinet and the Finance Department.

Canada-India relations are also likely to flare in the wake of developments late on Friday (here, here) which is unfortunate. We were met with warmth, kindness and professionalism on a recent trip to our valued clients in Mumbai. As important issues are addressed between sovereign governments, it is vital to maintain professionalism and warmth between the citizens and businesses of the two countries. On the path to India’s election in June may be heightened tensions with the international community should Canada’s allegations be proven.

The Ivey PMI for April (Tuesday) and the Bank of Canada’s financial system review (Thursday) won’t offer a whole lot of excitement.

US—A Nearly Empty Calendar

US macro risk goes dead quiet this week with only weekly initial jobless claims (Thursday) and the University of Michigan’s consumer sentiment update for May (Friday) on tap.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.