Next Week's Risk Dashboard

- Are markets getting too aggressive pricing BoC cuts?

- US bond auctions will test appetite for the recent drop in yields

- RBA could resume hiking

- Banxico expected to pause

- Peru’s central bank expected to cut

- BoC’s not-minutes probably won’t add much

- Inflation: China, Mexico, Chile, Colombia, Brazil, Philippines, Taiwan, Norway

- Inflation expectations: Eurozone, New Zealand

- Global macro readings

Chart of the Week

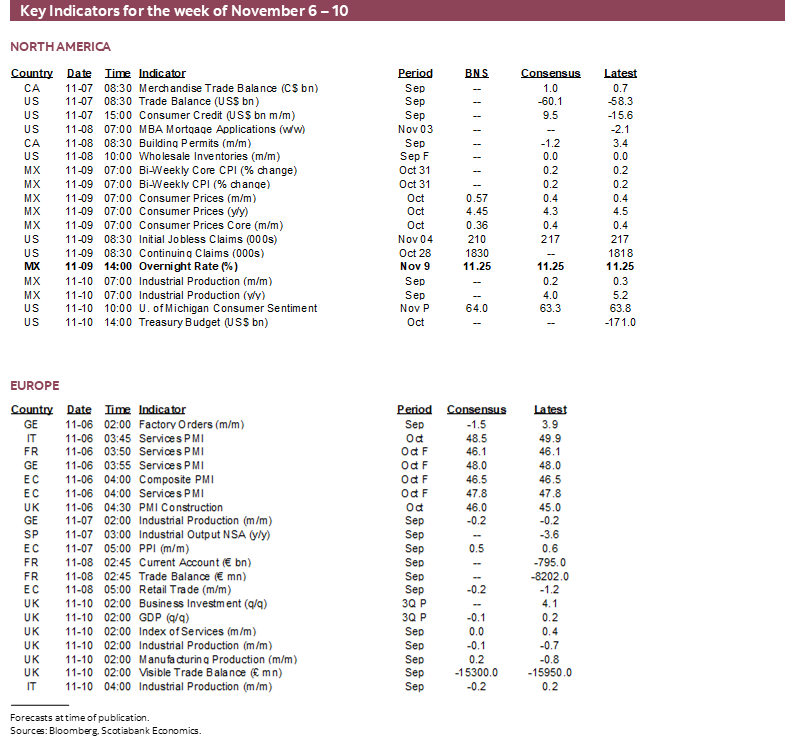

The coming week will be a much lighter one than recent weeks but there will still be a few developments to keep it interesting. We’ll hear from Fed Chair Powell again, the RBA may hike, and two LatAm central banks may hold (Banxico) and cut (Peru) while even more BoC communications lie in store. Data risk will be more subdued, with a few gems mixed in including a round of readings on global inflation and inflation expectations, plus Chinese and UK macro data.

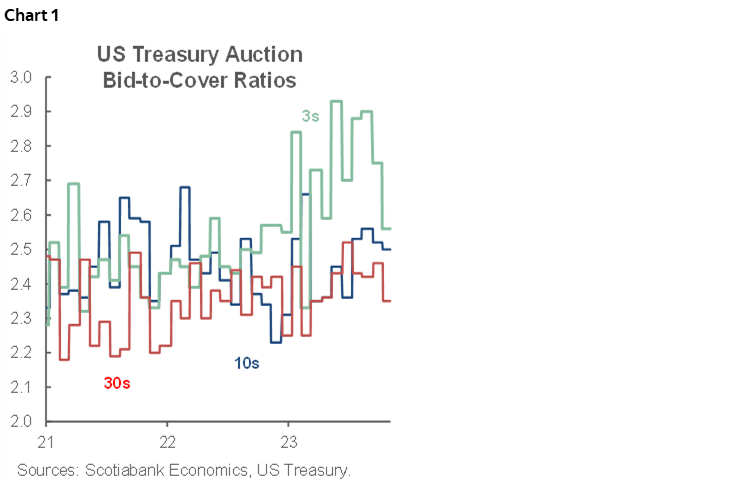

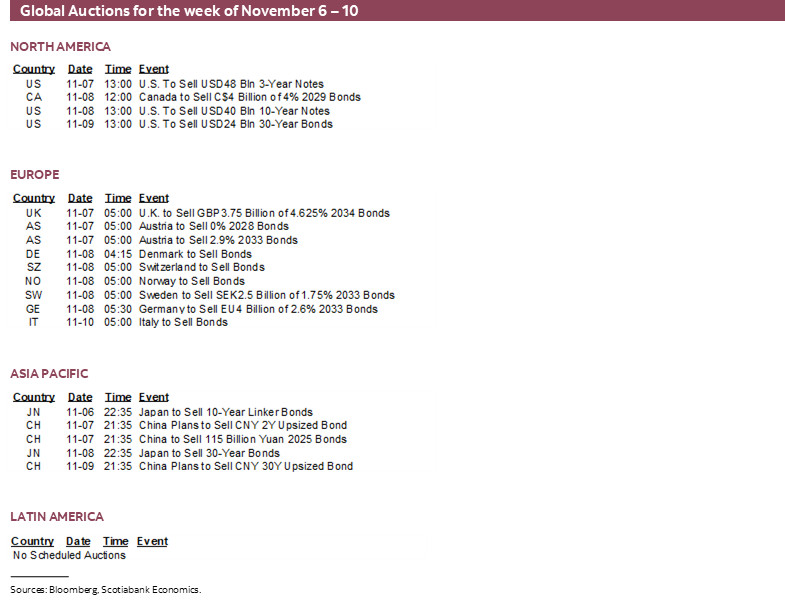

After this past week’s Treasury announcements on marketable debt issuance and the Quarterly Refunding statements allayed some bond market fears, the real test may come in this coming week’s US Treasury auctions for 3s (Tuesday), 10s (Wednesday) and 30s (Thursday). There are many gauges of auction strength, but one is bid-to-cover ratios that have recently ebbed as bonds sold off (chart 1). We’ll see if market participants now chase lower yields with stronger bid-to-cover ratios. That could be more consequential than anything else in an otherwise lighter than usual week.

A lighter than usual week of developments affords the opportunity to assess prospects for Bank of Canada moves given how rapidly the market is turning.

CUTTING BY SPRING COULD BE POLICY ERROR

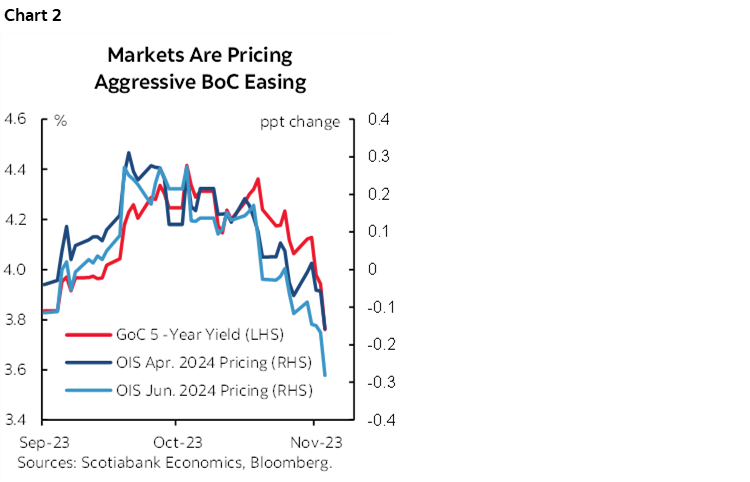

Will the Bank of Canada cut when Spring is in the air? That seems rather optimistic, yet it is exactly what markets are leaning toward in the wake of a jobs report that was generally in line with expectations (here). As chart 2 shows, a full 25bps rate cut is now priced for June and markets are pricing a significant portion of such a cut by the April MPR meeting.

Markets haven’t stopped there. The 5-year Government of Canada bond yield has dropped by over 60bps very recently and to the lowest levels seen since earlier this summer. Since this is a key determinant of the popular 5-year fixed mortgage rate, people looking to renew their fixed rate mortgages or take out a mortgage to finance a first foray into the housing market may rejoice.

To go against markets can be dicey but is hardly without precedence throughout the whole pandemic era. Recall last Spring when markets were convinced that the BoC would be cutting after its premature pause in January and as the US regional bank crisis was unfolding. They didn’t cut, and the BoC came back with two more hikes in June and July.

Cutting Would Embolden Free Spending Governments…

One reason to be leery toward Springtime easing is the signal that it would send to governments.

As they embark upon the Winter budget season that typically runs from about February to April at the Federal and provincial levels, governments would be getting a message from the BoC that their interest expense may not turn out to be as elevated as feared. I doubt very much that would be tucked away for deficit relief, especially with elections ahead in British Columbia, Saskatchewan and New Brunswick by October 2024, and then the Federal election on or before October 2025. In this climate, governments are heavily inclined to increase spending and would likely deploy any relief on interest expense toward such purposes.

That, in turn, could add more to inflation risk when the BoC has already signalled concern about government spending fighting the effort to control inflation.

…and Reignite Housing Again…

Canada’s housing market is highly seasonal with the Springtime environment a beehive of activity. Last year when the BoC went on premature pause in January and then the US regional banking crisis unfolded, the result was to drive the 5-year GoC bond yield sharply lower and take the key 5-year mortgage rate down with it. The result was to light up home sales that jumped by a whopping 11% m/m SA in April as one of a series of five monthly gains. House prices were bid higher and inflation risk pivoted higher along with them. That was one of the motivating factors for the BoC to return to rate hikes in June and July.

I think the BoC is loathe to go through that experience again. The impact of easing prematurely could be to either thwart prospects for more easing later with higher inflation for longer than otherwise, or to risk an erratic path of having to come back with renewed tightening later.

…While Adding to Other Sources of Inflation Risk

A complementary assumption to the above is that the other drivers of inflation risk will remain elevated. Before turning to them I think it’s important to downplay two points that others are making.

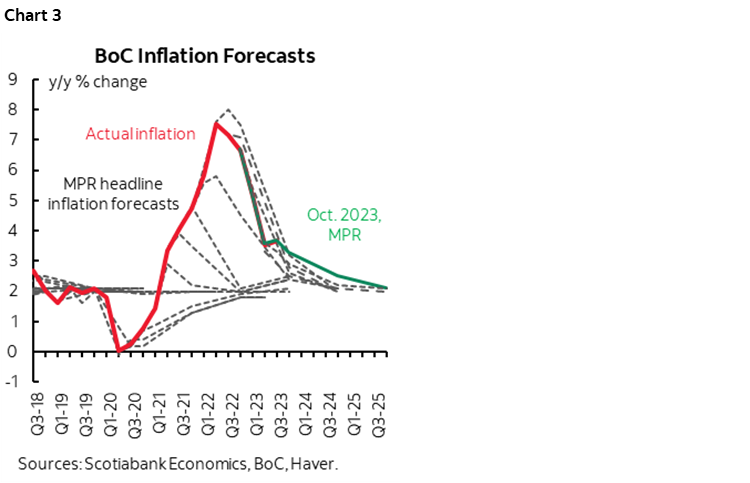

Consensus is putting a lot of stock in weaker GDP growth tilting inflation risk to be lower, not higher. I’m less convinced. Output gaps and augmented Phillips curves have performed poorly as out-off-sample predictors of inflation throughout the pandemic. That’s one reason why the BoC’s track record at forecasting inflation has been so poor as indicated by the pattern of actual inflation versus what they have actually forecast in successive MPRs (chart 3).

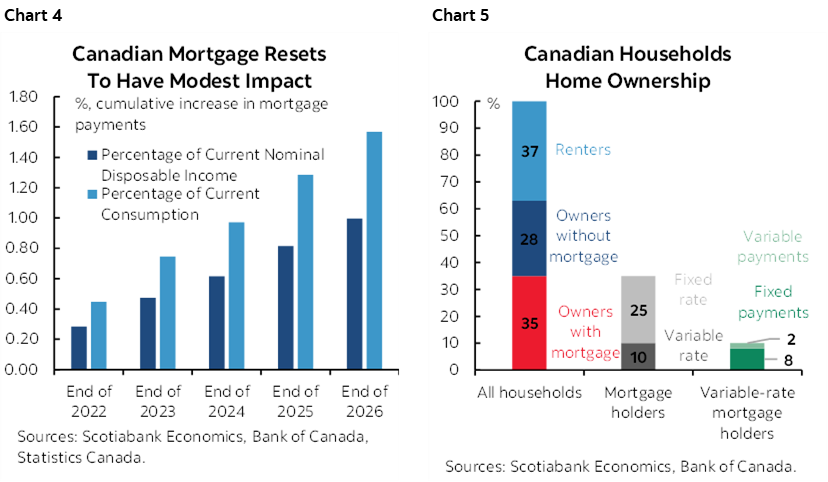

Consensus is also putting a lot of stock in how mortgage rate resets will bring the house down, so to speak. I think their views are exaggerated. The sum total hit to mortgage payments as fixed rate mortgages are reset higher over 2024–26 amounts to about 1% of total household income between now and then (chart 4). That is a calculation that took mortgage rates at their recent peak and allowed for no income growth over this period. In reality, the shock effect is likely to be lower as incomes rise and fixed mortgage rate relief may emerge by then even if it’s perhaps too early now while households and lenders adapt. It will be acutely felt by the most leveraged fraction of the 40% of households that own their home and have a mortgage (chart 5), but it is not enough to tip the apple cart in a macro sense.

Instead, I still think that inflation risk is pointed higher and that the BoC will be challenged to sustainably achieve 2% inflation. Among the drivers of this view are the following points.

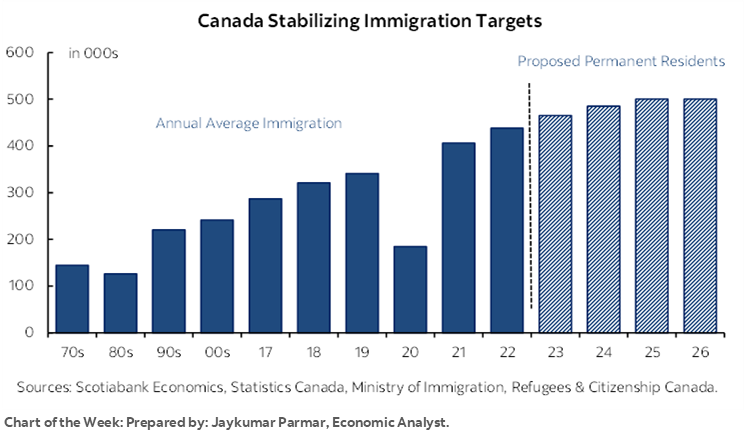

- Even with the slight curtailment on the temporary/nonpermanent side, immigration remains unsustainably high in relation to shortages in housing, consumer markets like autos, and infrastructure shortfalls (see front cover chart).

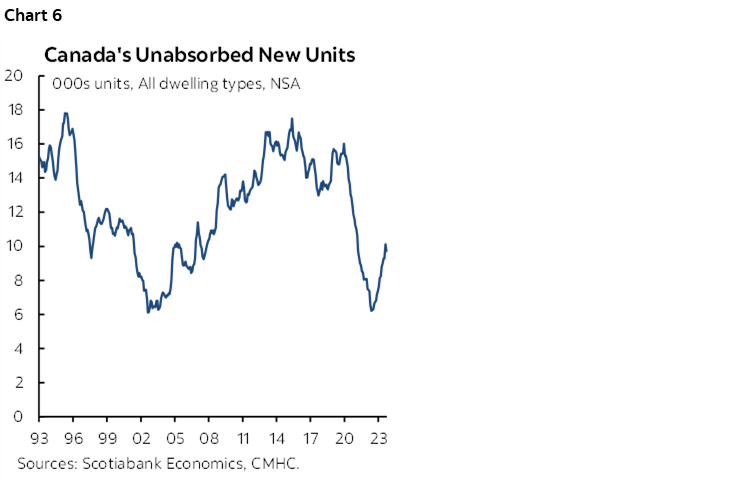

- New housing inventories remain tight (chart 6) and the pace of homebuilding is adequate to meet demand. The result is that rent overall shelter costs continue to put upward pressure on CPI.

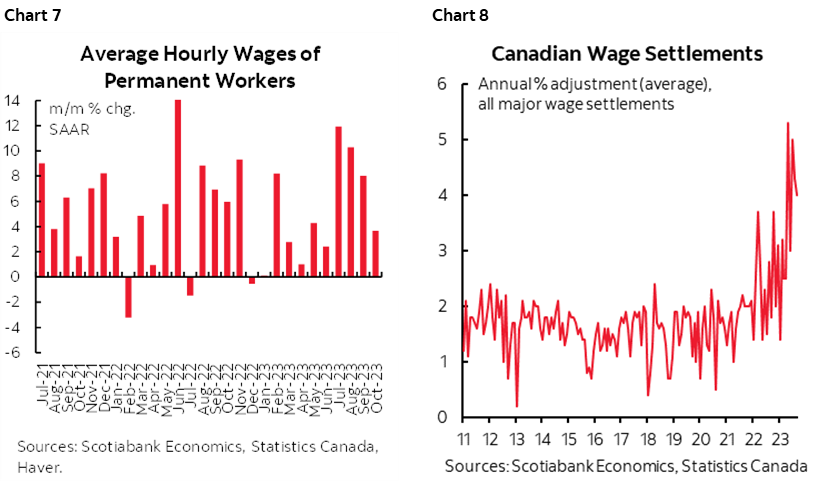

- Wage growth ebbed in October but was still too high and is volatile. The three-month moving average increase remains at about 7% m/m SAAR (chart 7). Wage settlements in the unionized sector that represents one-in-three Canadian workers (three times the US rate) remain hot (chart 8) with high spillover risk into nonunionized sectors and at rates well above the BoC’s inflation target.

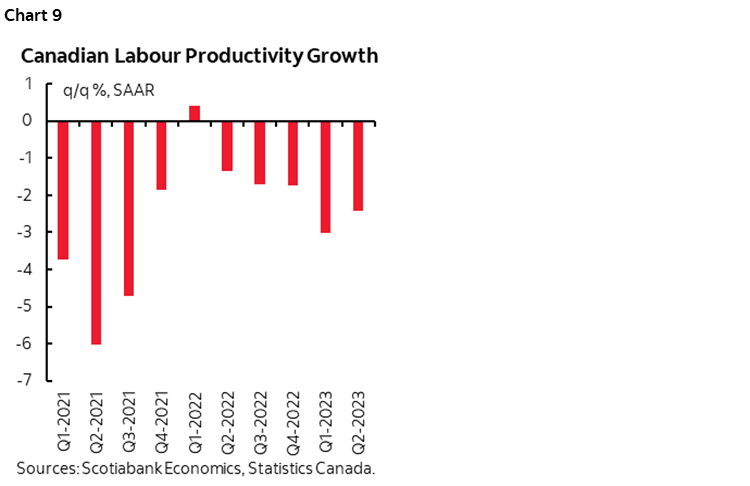

- Labour productivity stinks and is in sharp contrast to the evidence of a productivity rebound in the US over the past couple of quarters (chart 9). Canadians are getting paid more for producing less, the combined effects of which challenge the BoC’s inflation target as companies continue to pass on the costs.

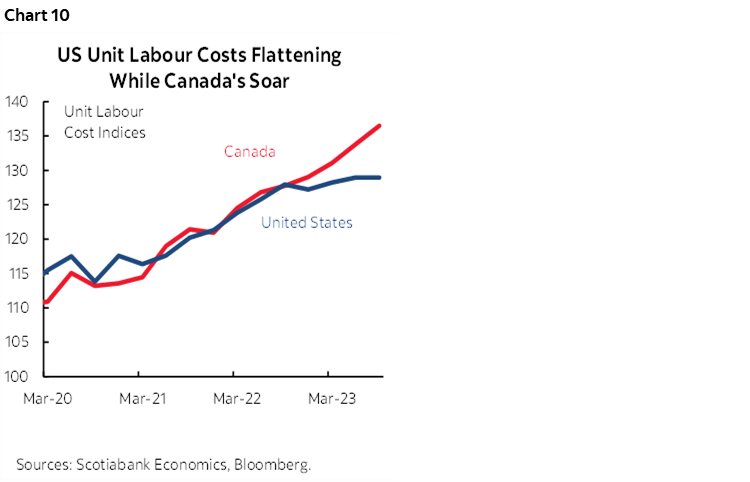

- As a result, Canadian unit labour costs are rising while they are starting to flatline in the US (chart 10).

- The Canadian dollar remains undervalued in our view. Easier monetary policy would destabilize the currency when many central banks around the world are concerned about the resulting potential to stoke import price inflation especially in a country that imports much of what it consumes. So, while some suggest that BoC easing will drive a tumbling CAD, I think they will seek to avoid that especially given the next point.

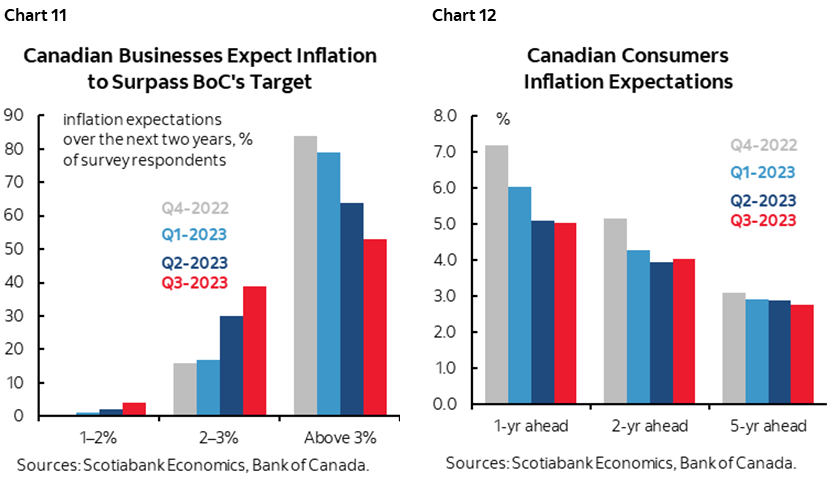

- Inflation expectations remain far above the BoC’s 2% target for years to come in consumer and business surveys (charts 11, 12). It’s easier to downplay upside risks to inflation if inflation expectations are aligned with the BoC’s target but that is not the case. Instead, high expectations are motivating changed behaviour as indicated by the prior comments on wages.

- The external backdrop for the Canadian economy remains buoyant. The terms of trade is still supported by fairly elevated commodity prices and the US economy remains strong.

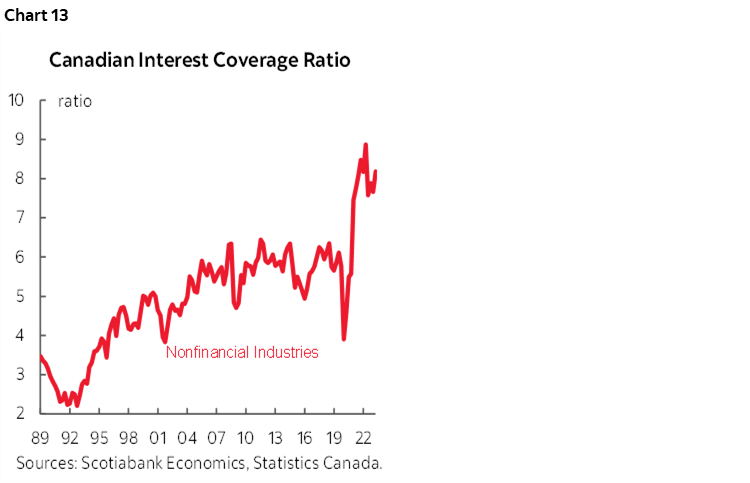

- Nonfinancial corporate balance sheets remain strong (chart 13). That could provide support to the job market compared to periods of time when corporate balance sheets were more strained. So could the fact that government hiring has driven so much of the job growth during the pandemic and in the absence of any likely austerity programs going forward as noted here.

CENTRAL BANKS—A HIKE AND TWO CUTS?

This will be a lighter but not uneventful week for central banks compared to the deluge of decisions by the Fed, BoE and BoJ this past week.

Powell to Reappear

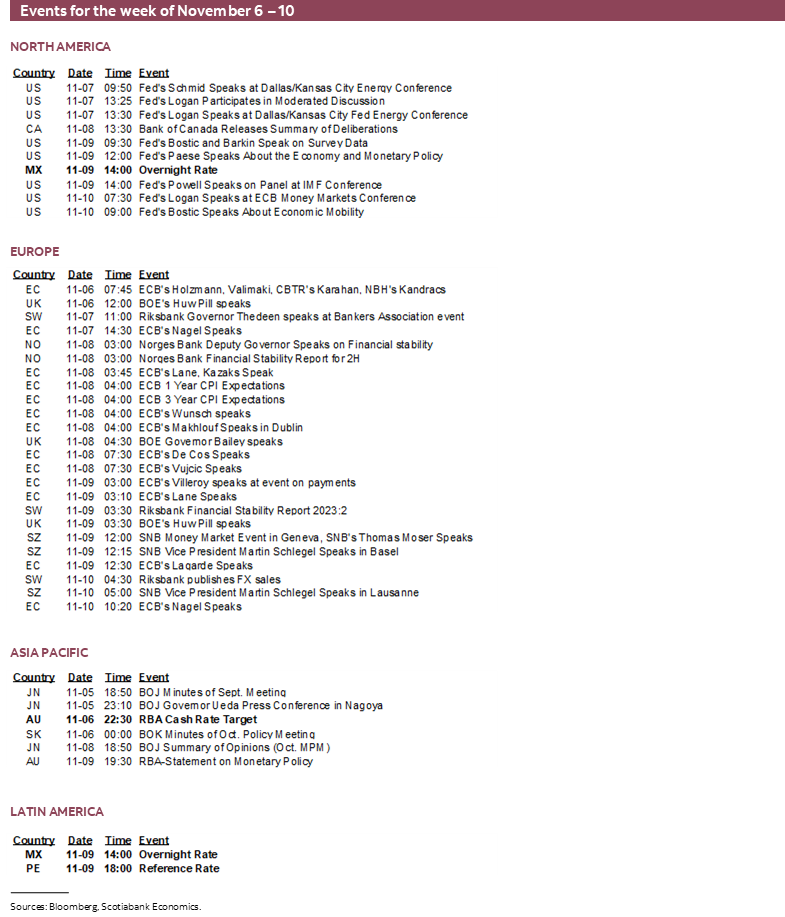

The Federal Reserve added a panel appearance by Chair Powell at an IMF conference on Thursday at 2pmET for 90 minutes. He will share the panel on monetary policy challenges in a global economy with the IMF’s Gita Gopinath, academic Ken Rogoff, and Bank of Israel Governor Amir Yaron. If he wishes to clarify anything that he said this past week when his remarks prompted an easing of financial conditions, then this would be an opportunity to do so.

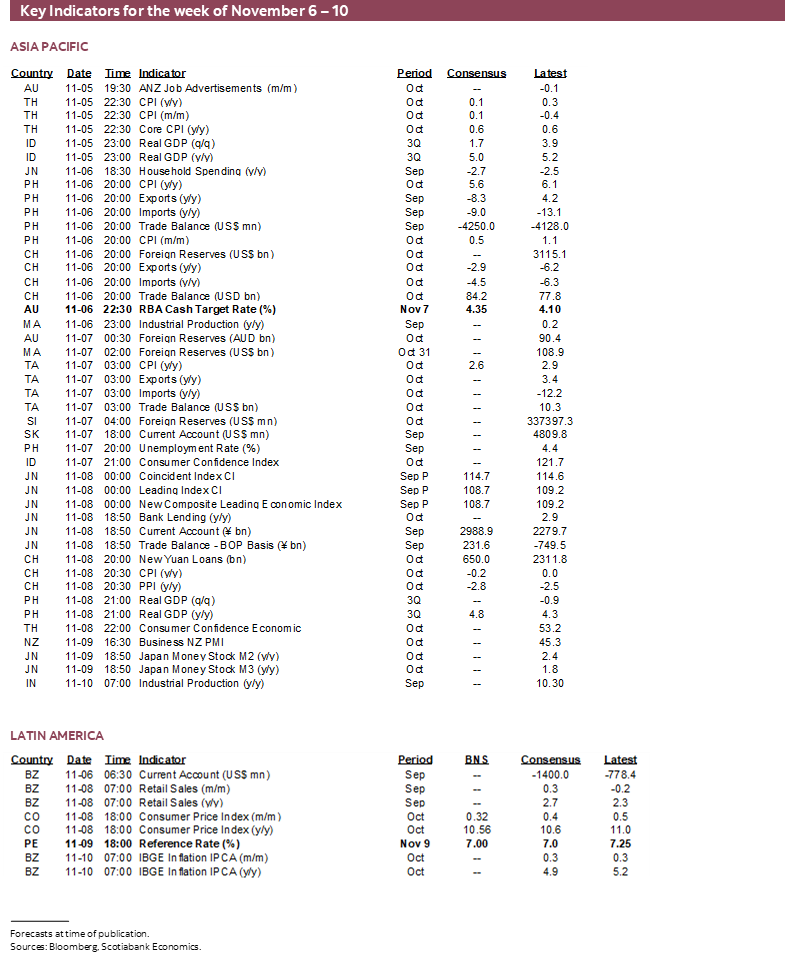

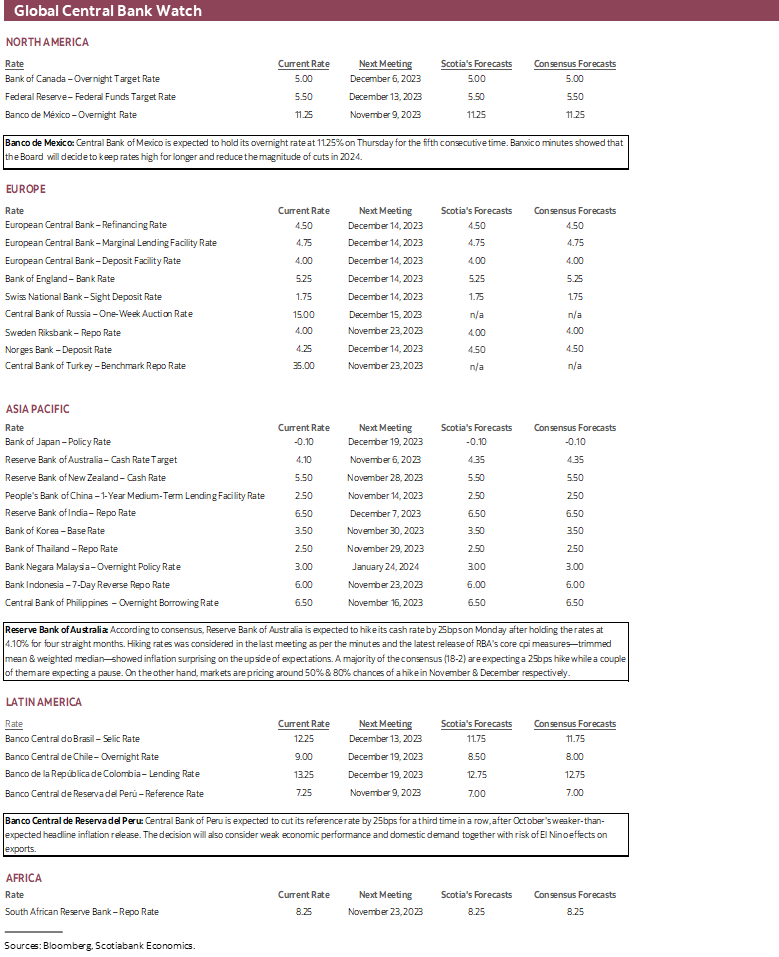

RBA—Resuming Hikes?

Economists and markets are somewhat divided on the prospects of hiking the policy rate for the first time since June after a four-meeting pause. The RBA’s decision arrives on Monday night eastern time. Markets are on the fence with 50–50 pricing (chart 14). The consensus of two-dozen economists is almost unanimous in expecting a hike. Economists have been wrong on the RBA before including when they were wrong in expecting the RBA to hike at the August 1st meeting when they held.

So what has changed to spark this speculation? A new Governor is one thing, as Michelle Bullock took the reins on September 18th, replacing Philip Lowe. She has generally been sounding a little more hawkish of late. Saying ‘we may need to go again’ on October 25th was a bit of a hint! She expressed uncertainty toward getting to the inflation target quickly enough.

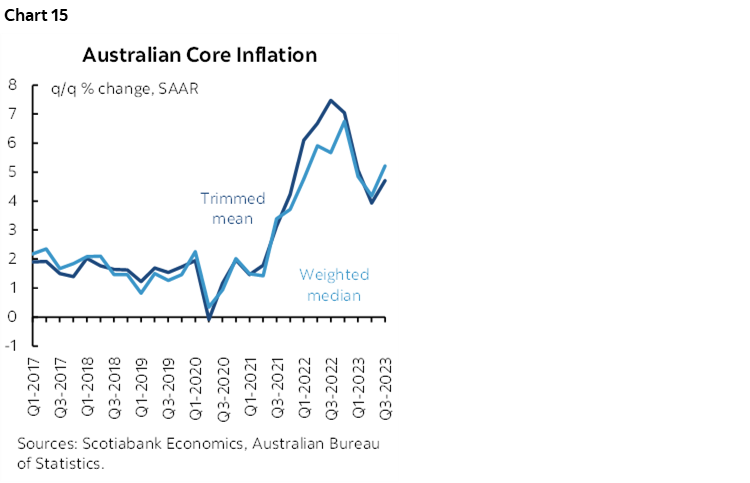

Data has also leaned toward the resumption of hikes, or at least one. A little over a week ago, Q3 inflation data was released that surprised to the upside across all of the measures especially the key trimmed mean and weighted median yardsticks (chart 15). The consumer has been doing well as retail sales were up 0.9% m/m in September. Private sector credit growth has continued to grow in uninterrupted fashion every month since September 2020 despite rate hikes. The Australian dollar has been depreciating from the early year peak of US$71.4 cents to about seven cents lower now and is trending around its weakest levels of the past twenty years. For an economy that imports a lot of what it consumes, that may be adding to inflationary pressures at the margin.

What will matter at least as much as whether or not they hike will be the bias; is it one-and-done, or the start of something more? I would think that there is little point to opening the bag of chips and having just one.

Banxico—Still on Hold

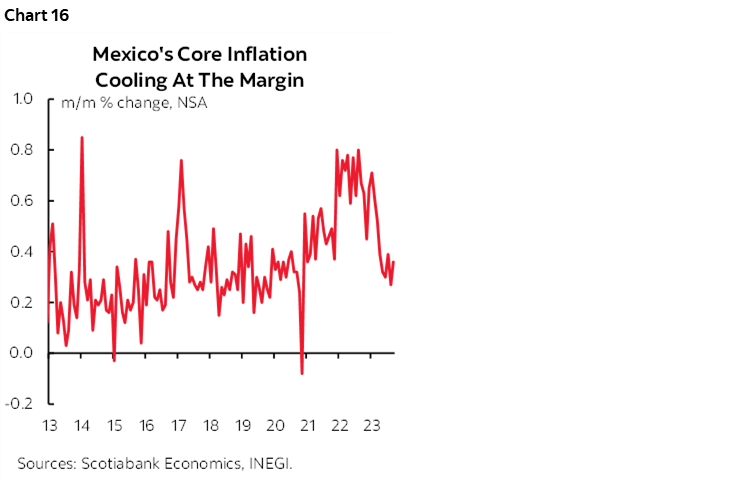

Mexico’s central bank is widely expected to stay on hold at an overnight rate of 11.25% on Thursday afternoon at 2pmET eastern time. That would extend the hold that has been in place since the last hike back on March 30th. Inflation has continued to make progress with September’s core reading falling to 5.8% y/y from a peak of 8.5% a year ago. That hasn’t only been driven by year-ago base effects either, as month-over-month core inflation has been cooling through a series of softer than seasonally normal increases in seasonally unadjusted core inflation since Summer (chart 16). Managing peso volatility in the face of an uncertain Fed outlook adds caution.

BCRP—Another Cut Coming in Peru

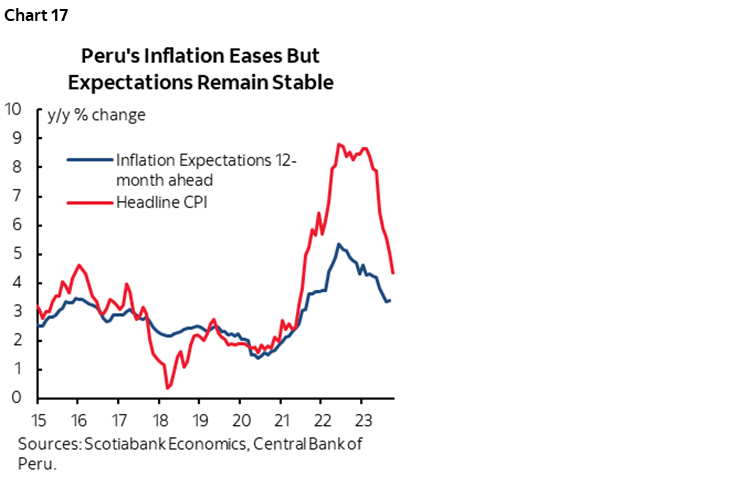

Further progress on inflation should give Banco Central de Reserva del Peru room to continue easing on Thursday. A 25bps rate cut is expected and would take the reference rate down 75bps since the first cut in September. Inflation fell by more than expected in this past week’s reading for November when it dipped to 4.3% y/y from 5% previously (4.9% consensus). Pressures on core inflation at the margin have also moderated this year compared to last year’s pattern of outsized month-over-month jumps (chart 17).

Communications Overload at the BoC

The Bank of Canada delivers its Summary of Deliberations to the process leading up to the October 25th hawkish hold. There are not ‘minutes’ the way other central banks deliver their accounts of the discussions and they were forced upon the BoC by the IMF’s demands for greater transparency. I don’t expect much of anything new in the deliberations given that the BoC has been on communications overload with the full MPR meeting and press conference and then two rounds of testimony before parliamentary committees this past week.

GLOBAL MACRO—GLOBAL INFLATION READINGS IN FOCUS

Inflation updates will be a significant focus across a number of markets with updates to the following readings.

China’s Volatile Inflation

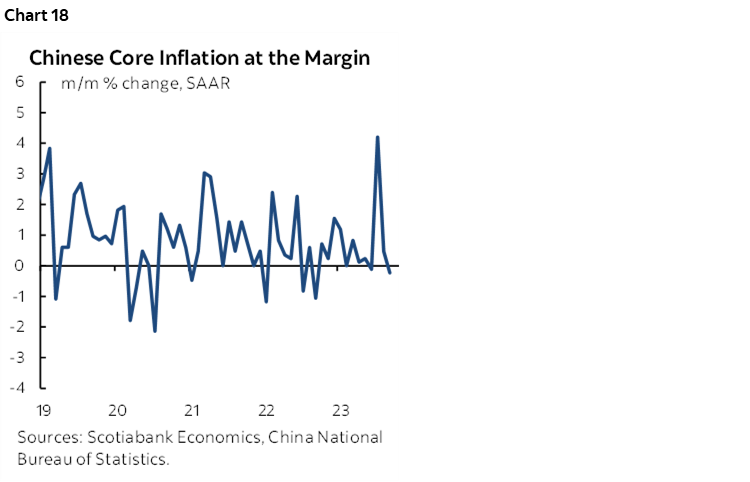

China updates CPI and producer price index gauges for October on Wednesday. Key will be core CPI on a month-over-month basis. That reading has been volatile as August’s reading was among the strongest compared to like months in history absent seasonal adjustments, only for September’s reading to be among the weakest (chart 18). Inflation is low and far below the PBOC’s 3% target such that it gives room to ease monetary, regulatory and fiscal policies, but deflation it is not. At least not the way most economists define it as a sustained, broadly based decline in prices that comes to be expected such that behaviour fundamentally changes including through postponement of consumer spending into an environment of cheaper prices. There is little evidence that this is what is happening in China and a great deal reason to believe that inflation will move higher into 2024.

ECB Inflation Expectations

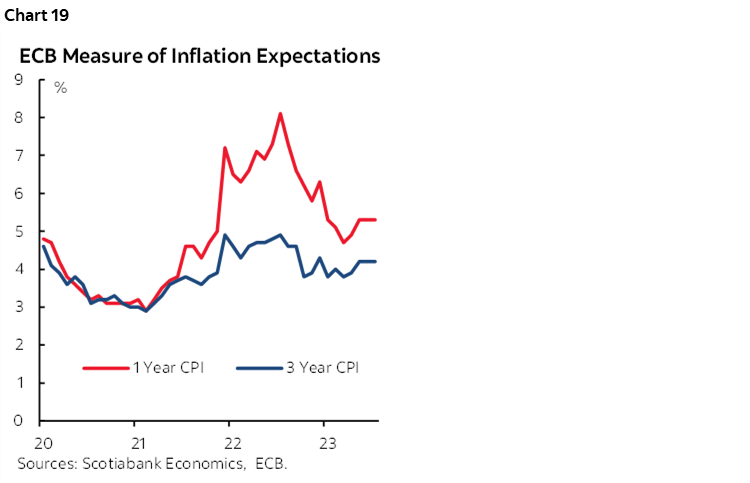

ECB measures of inflation expectations will be updated for the month of September on Wednesday over 1- and 3-year horizons. September’s readings moved a touch higher (chart 19) after a roughly year-long move lower. Both gauges remain above the 2% inflation target particularly in the nearer term. Any further rise would probably reignite concern among the hawks.

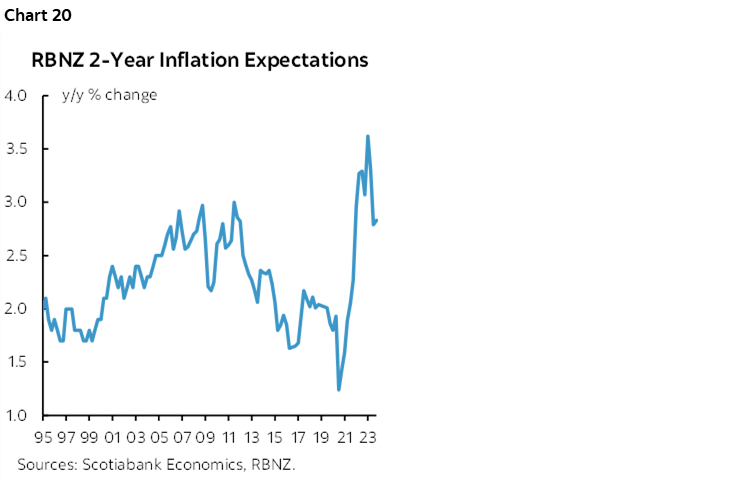

RBNZ Inflation Expectations

The Reserve Bank of New Zealand’s measure of two-year ahead inflation expectations will be updated with Q4 figures on Tuesday. Like the Eurozone measures, the RBNZ’s measure halted downward momentum in Q3 (chart 20). Any renewed rise when the reading is already stuck modestly above the 2% inflation target coupled with the risk that its neighbour hikes across the Tasman Sea as the NZ$ has been depreciating throughout the year could motivate the RBNZ to rebalance its perception of risks to the policy rate going forward.

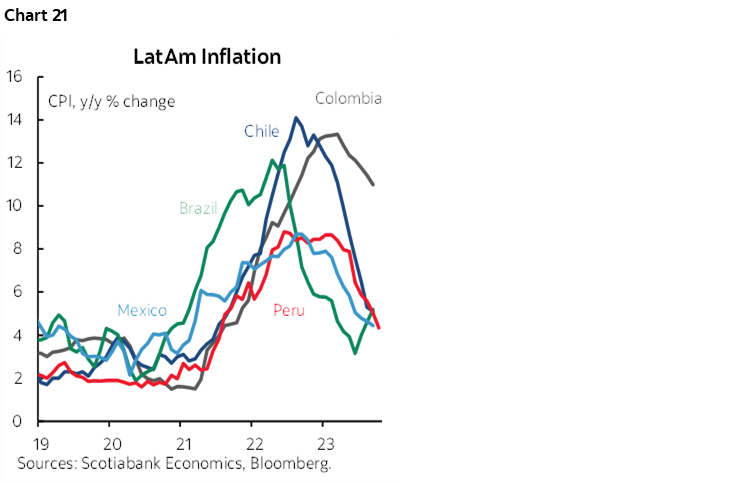

LatAm Inflation Updates

Chile and Colombia release updated CPI estimates for October on Wednesday and then Mexico follows on Thursday followed by Brazil on Friday. One quickly gets a sense of why the region’s central banks have had divergent stances over recent meetings by just looking at chart 21. Inflation remains very high in Colombia where BanRep remains on hold. It is making rapid progress in Brazil and Chile where the central banks have been cutting. Mexico has also been making progress, but concern about whether the Federal Reserve is done hiking and when it may begin easing motivates considerable uncertainty toward financial stability including the peso’s movements.

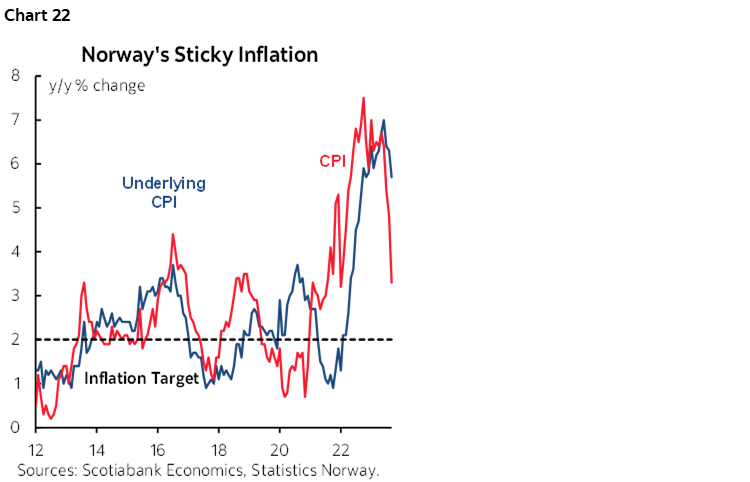

Norway’s CPI Could Impact Norges Bank

Norway will update CPI for October on Friday with underlying inflation still stubbornly high (chart 22). This reading may make-or-break Norges Bank’s commitment to hike again at its next meeting on December 14th after its recent conditional support for a hike.

Will Philippines’ CPI Inform BSP’s Stance?

The last inflation reading before Bankgo Sentral ng Pilipinas’ decision on November 16th lands on Monday and it could inform whether the central bank has done enough after its surprise 25bps hike in October following an extended pause. Taiwan also updates CPI for October on Tuesday with its next decision not expected until mid-December.

The Rest

Canada will update trade figures for the month of September on Tuesday. Export volumes are tracking higher while import volumes are tracking lower so far over Q3 based upon July and August readings plus the Q2 figure. The combined effects could offer a boost to GDP growth as estimated by expenditure-based accounts versus the monthly production-based GDP accounts. Canada will also update the Ivey purchasing managers’ index for October on Monday but its usefulness is limited because it’s a mish mash of everything across the public and private sectors and therefore we can’t tell what’s driving it.

US releases will be very light. On Tuesday, the overall US trade deficit is expected to be little changed at about -US$60 billion given that we already know the merchandise deficit increased by only about one billion and the slightly rising services surplus is quite stable. Weekly jobless claims (Thursday) and the University of Michigan’s consumer sentiment reading for November (Friday) are also due out.

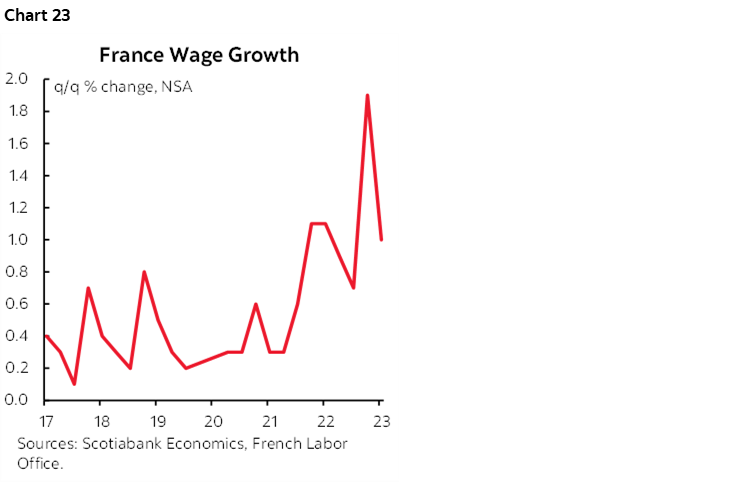

Wage measures from Japan and France are the only ones expected this week. The Bank of Japan is waiting for the Spring round of wage negotiations, but in the meantime it is likely to receive September estimates of labour cash earnings that are expected to be up by only 1% and down by over 2% in real terms. France’s Q3 wage figures (Thursday) will be monitored by ECB-watchers given the pattern of fairly strong quarter-over-quarter gains since the start of 2022 (chart 23).

The UK economy has been suffering from weak growth and Friday’s Q3 GDP estimate is expected to post no growth. This is part of the reason why the Bank of England has held Bank Rate unchanged over the past two decisions, along with job losses, moderating wage gains and inflation. The UK will also update monthly readings on industrial production, services activity, construction and trade for September on Friday that will inform hand-off momentum into Q4.

Other releases will include German factory orders (Monday) and industrial output (Tuesday), Chinese exports during October early in the week, and possible monthly financing and credit figures this coming week or the following one.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.