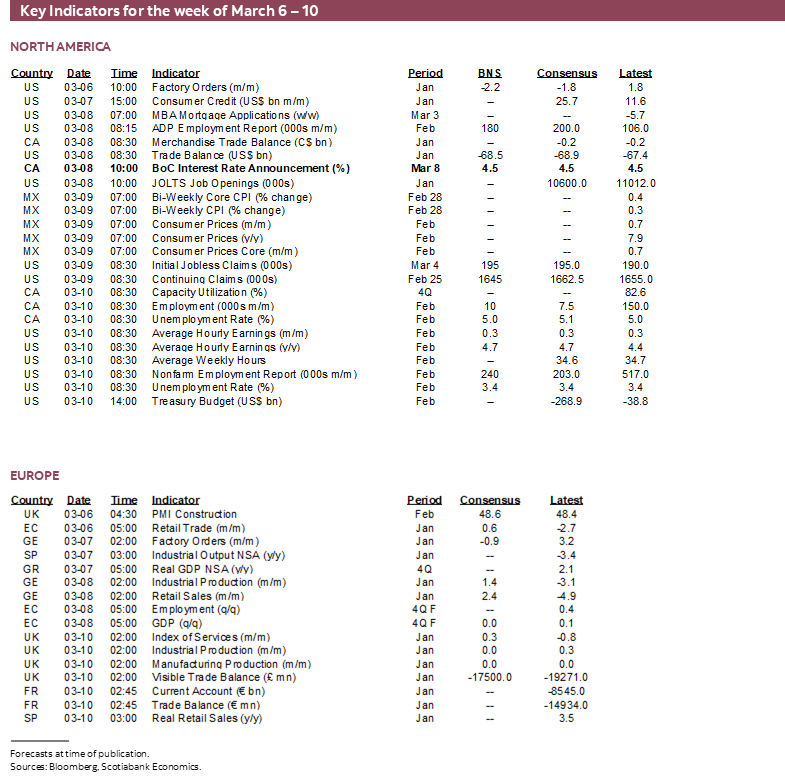

Next Week's Risk Dashboard

- Powell may guide markets into the March FOMC

- China’s NPC could fiscal plans…

- …plus GDP and inflation targets

- US nonfarm payrolls still resilient?

- BoC to pass but is still in play

- Playing the odds on Canadian jobs

- BoJ’s Kuroda to exit with honour

- RBA sheds prior pause, likely to hike again

- Peru’s central bank expected to stay on hold

- Bank Negara to stand pat amid currency risk

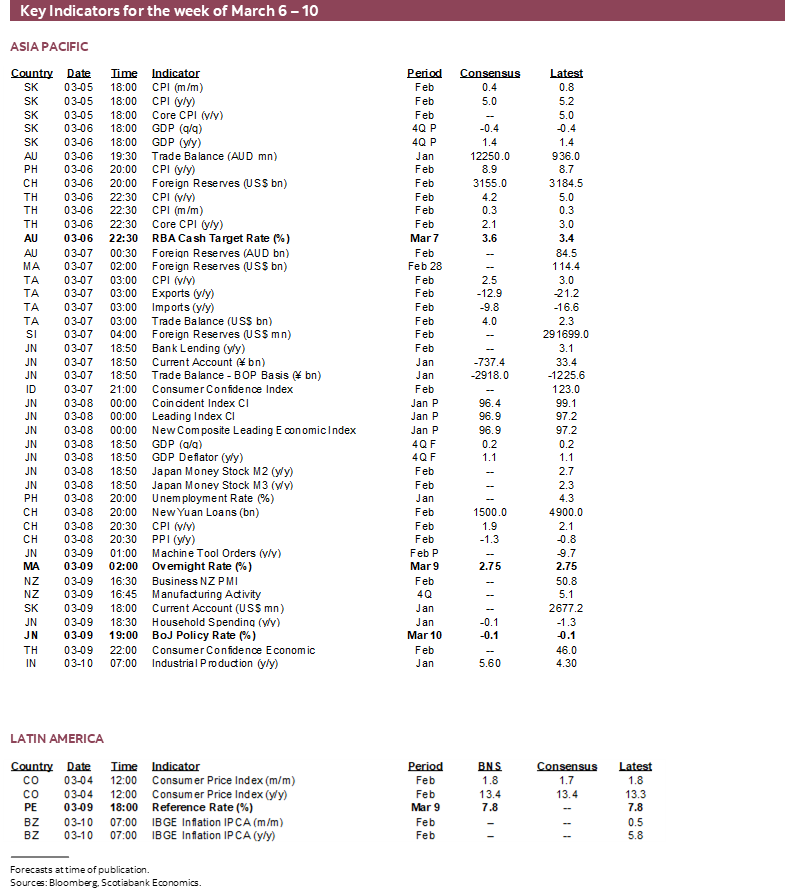

- CPI: Latam, Asia-Pacific, Norway, Switzerland

- UK, German macro reports

Chart of the Week

The coming week’s assortment of macro risks to global markets can be lumped into three broad categories.

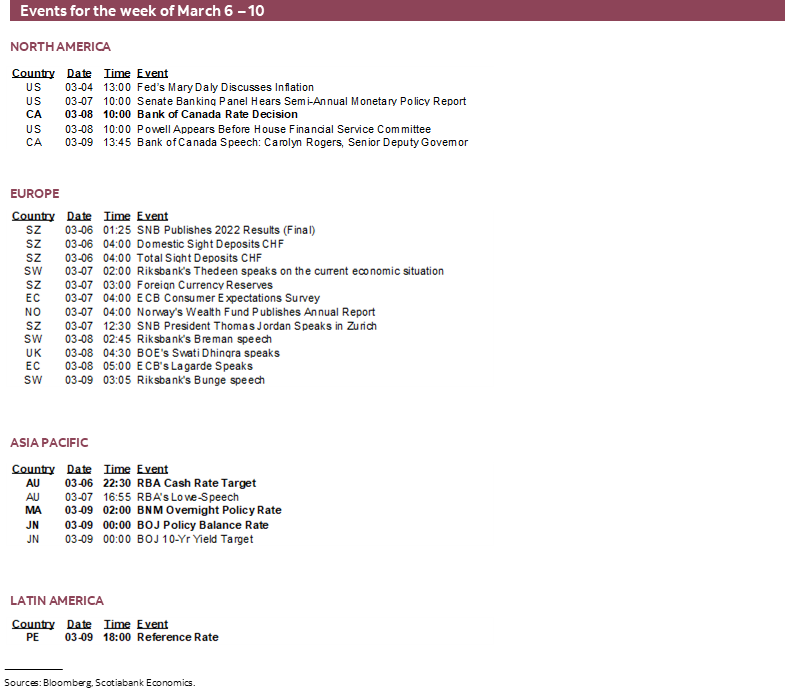

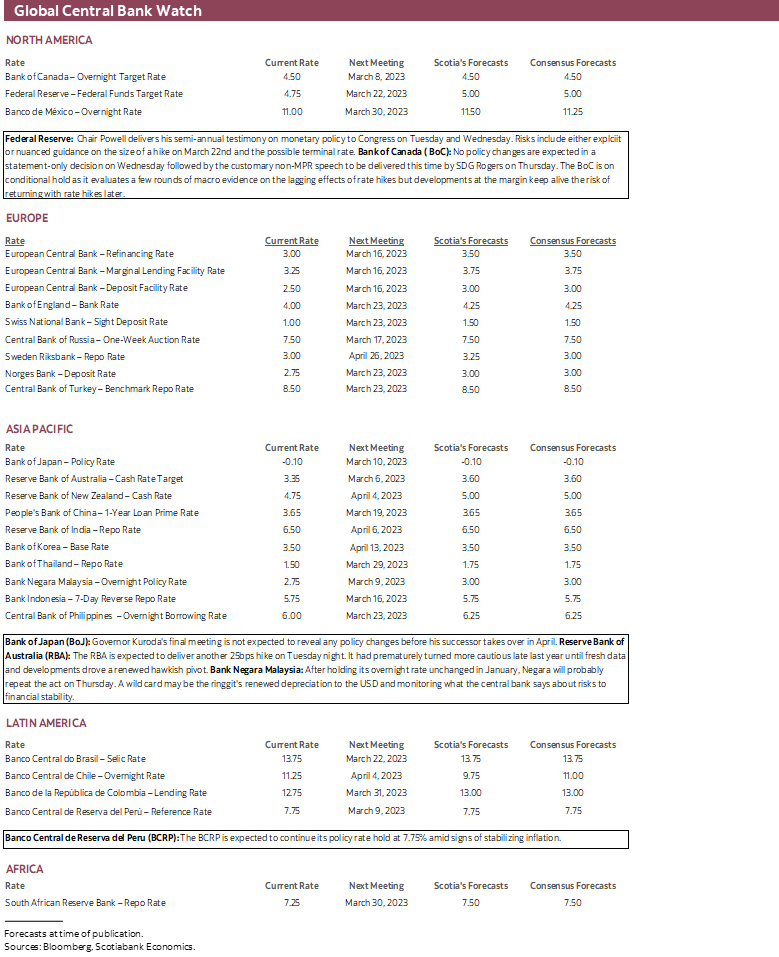

After a short reprieve, central banks jump back into the fray again this week and start assessing the damage to wishful hopes that inflation risk had perhaps once been ebbing. Potentially key testimony by Fed Chair Powell will lead the way. Central banks that may have prematurely turned hesitant to hike further—like the RBA and Bank of Canada—will also weigh in. Governor Kuroda will mark the end of an era at the BoJ in probably quiet fashion and deserving of much credit. The BCRP and Bank Negara round out the central bank calendar.

Second, the week ends with fresh key macroeconomic reports after the central bankers are done. At the top of the list will be US nonfarm payrolls with a side order of Canadian jobs. Wages may matter at least as much in both reports.

Third, commodity markets will be focused upon China’s National People’s Congress as it lays out new budgets as well as growth and inflation targets.

POWELL’S LAST CHANCE TO INFLUENCE MARCH PRICING

Federal Reserve Chair Powell delivers semi-annual testimony before Congress on Tuesday and Wednesday before the Senate Banking Committee and the House Financial Services Committee respectively.

This is key because if he wishes to influence market pricing for the decisions that will come out of the March 21st – 22nd FOMC meeting then this is his last and best chance to do so. The FOMC goes into communications blackout just days later on Saturday March 11th.

There will be two principal risks. First is whether he wishes to guide pricing for the next policy rate decision. Markets are presently pricing in about a one-in-four chance that the Fed could hike by 50bps. A wave of strong data has nudged pricing about 11bps higher for this meeting than was the case at about this time last month.

The second risk is whether Powell indicates his bias with respect to the terminal rate this cycle. Market pricing is on the fence between a peak fed funds upper limit rate of between 5½% and 5¾%.

BANK OF CANADA—QUIET QUITTERS?

The Bank of Canada delivers a statement-only decision on Wednesday morning at 10amET. There will be no forecasts, MPR or press conference. No policy changes are expected, but I’ll explain why I think the BoC has perhaps halted its hiking cycle prematurely. Recent developments have emphasized that a choice lies at hand in terms of further rate hikes in order to make sure that inflation will be brought durably lower, or a higher policy rate for longer which may rule out cuts for a long time, or higher inflation risk for longer. My preference would be for the BoC to return with further hikes and we may have enough information to evaluate this risk by either the April MPR or July MPR meetings.

The next day’s customary economic progress report that follows non-MPR decisions will be delivered by SDG Rogers this time. She is the last scheduled BoC official to speak before the next decision on April 12th. It’s possible that additional speakers could always be added and there will also be the publication of the summary of deliberations during the current process on March 22nd and the BoC’s next quarterly business and consumer surveys on April 3rd that will include updated measures of inflation expectations among other variables.

Expect a short statement this time. It may more succinctly spell out the BoC’s conditional pause that has been expressed in clearer fashion in speeches and press conferences than the somewhat muddled message in the final paragraph of the January statement. That paragraph said that if their forecasts evolve as expected then they will hold the policy rate unchanged while assessing lagging effects of rate hikes, but they are prepared to hike again if needed depending upon how inflation evolves. I think the intent was well placed because saying more clearly that they were done would drive a pile-on into the front-end of the Canada rates curve and further depreciate the currency with cutting bets derived from clearer evidence that the BoC has greater conviction that it is done. They should repeat this tactic either by leaving the paragraph intact or with a simpler sentence.

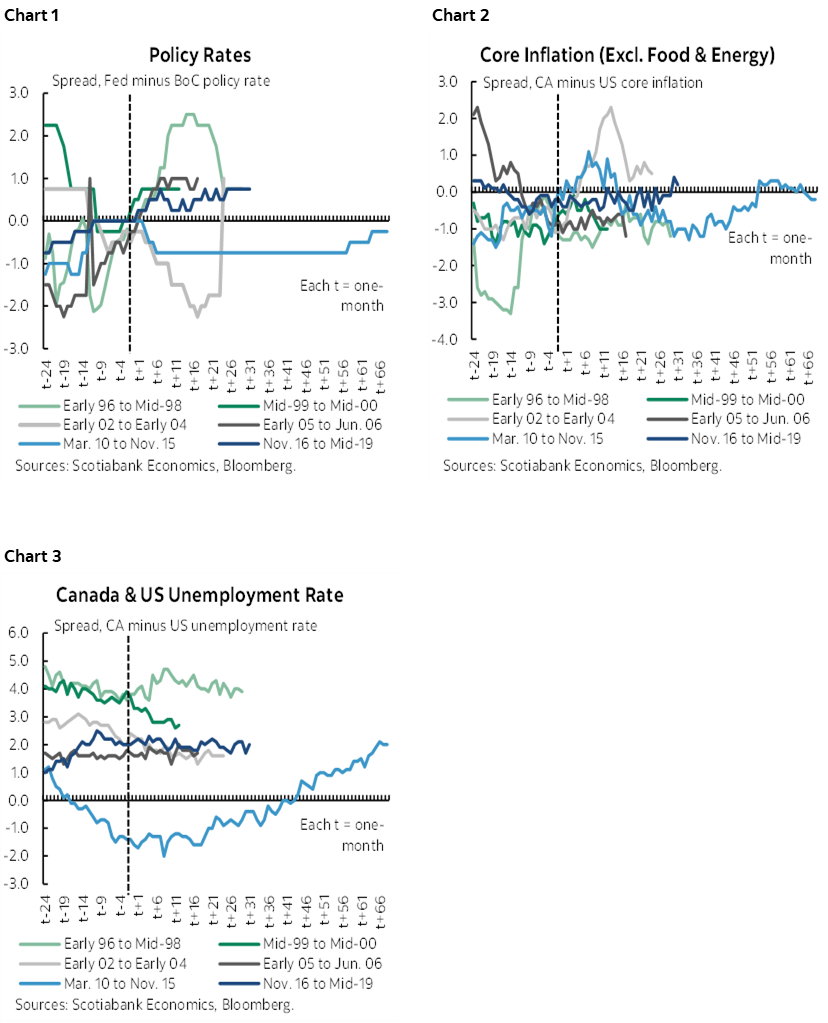

Historical Fed-BoC Deviation

The magnitude of the policy rate deviation between the Fed and the BoC relative to differences in their macroeconomic circumstances makes me concerned about the extent to which it is assumed the BoC can fall behind the Fed.

In the past when the BoC has undershot the Federal Reserve’s peak policy rate by as much as markets are pricing it has tended to be because of lower core inflation north of the border. Charts 1–3 help to illustrate this point. Chart 1 shows the spread between the Fed funds upper limit and the BoC’s overnight rate leading up to time t=0 which is defined as being closest to policy rate convergence and thereafter in past cycles. Chart 2 shows the Canada-US core inflation spread during these same time periods and chart 3 does the same for the unemployment rate.

The punchline to these charts is that usually when the BoC undershoots the Fed it is because Canadian core inflation is lower than the US. That is not the case today as the inflation rates are similar. I think inflation risk is higher in Canada as explained through the rest of what follows.

What Has Changed Since the Conditional Pause?

There has nevertheless been a lot of new information since that set of communications on January 25th. The BoC will acknowledge some of it this time around, while market participants will need to be mindful toward the rest even if the BoC dodges the issues in the statement and the next day’s speech and presser. A deeper dialogue is likely come the April MPR meeting or July.

1. Inflation—Still Too Hot

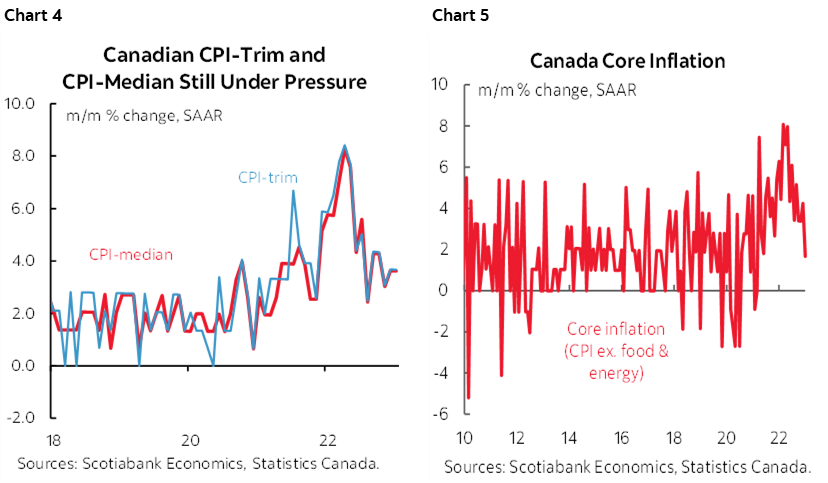

Expect acknowledgement of domestic progress but with continued caution that it is very tentative. My hope is that the BoC wouldn’t emphasize year-over-year inflation gauges especially after the whole base effects disaster they committed throughout 2021. In my view the risks are still slanted higher and the BoC should remain focused upon inflation risk given the minimal faith it should have in inflation forecasts whether its own or the street’s. Trimmed mean and weighted median CPI continue to rise at a fairly aggressive above-target pace in terms of the freshest evidence of pressures at the margin. Chart 4 shows m/m annualized gains. Traditional core CPI (ex-food and energy) has been ebbing in month-over-month terms (chart 5). See the recap of January’s CPI figures here.

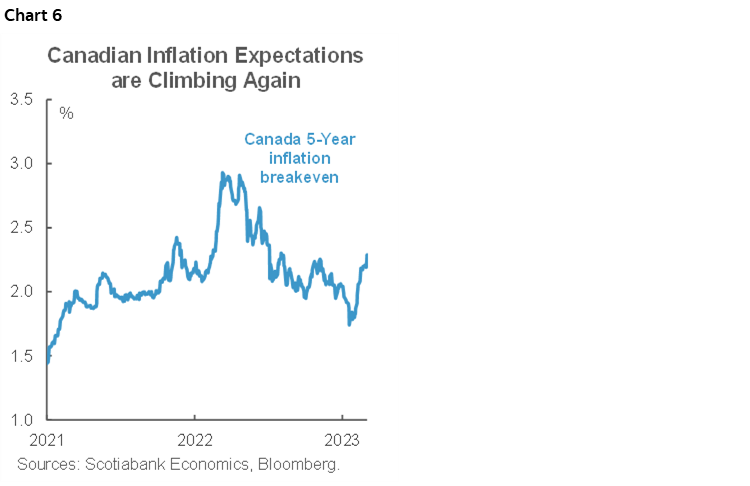

2. Inflation Expectations—On the Rise Again

Market-based measures of inflation expectations have been rising again and this time in the absence of higher oil prices (chart 6). US purchasing managers are indicating a broadly-based resurrection of price pressures across labour, non-energy commodities and electronic components that may include the rise in proxies for semiconductor prices since last Fall as indicated by the Philadelphia Exchange Semiconductor Index.

3. External Conditions—Looking Up

The US economy continues to perform better than many expected. China continues to rebound with PMIs rising at a faster than expected clip. Global inflation in key markets remains highly resilient, such as in the US and the Eurozone.

4. The Currency—BoC’s Warnings Could Come Back

Currency depreciation is signalling a limit to the extent to which the BoC can fall behind the Fed and this raises the risk of returning to past warnings from the BoC.

Governor Macklem and SDG Rogers were surprisingly candid about their concerns last October when USDCAD had risen toward 1.39 and was threatening the 1.40 mark. Macklem said in a speech (here) that the depreciation of the C$ could add to price pressures. He separately remarked that if CAD weakness persists “that will mean that, other things equal, we’re going to have more work to do on interest rates. We’ll be watching that closely.” At 1.36 today the currency has been back on a depreciating path over the past month and risks making the BoC uncomfortable again.

5. Jobs—Strength on Both Sides of the Border

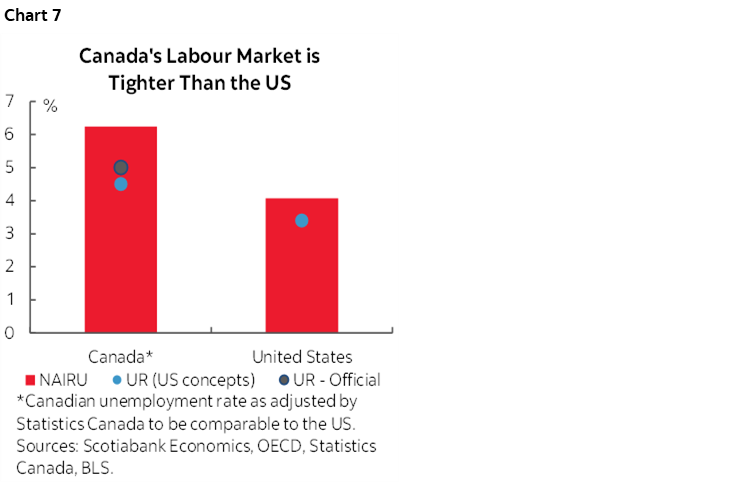

220,000 jobs created in two months. 150k of them in January alone and arriving after the BoC’s last decision. Figures like these have continued to tighten the job market. Canada’s job market is much tighter than the US defined as the spread between the official unemployment rates and reasonable proxies and ranges around equilibrium Nonaccelerating Inflation Rates of Unemployment (chart 7).

6. Wages—Unions Going for Gusto

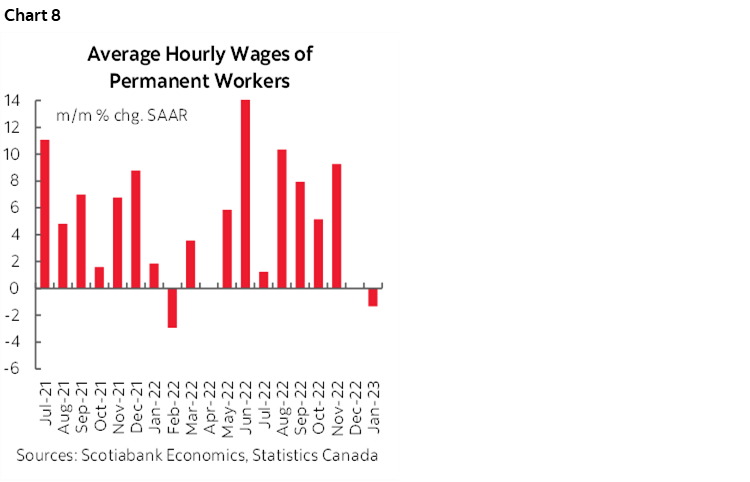

Mixed signals are being provided on wage growth. Average hourly wages of permanent employees have stalled out again over the past couple of months (chart 8). We’ve seen soft patches before during the pandemic and Friday’s update will further inform the trend. By contrast, figures for major wage settlements continue to showcase significant trend gains.

Large public sector wage settlements are a material risk to further wage growth that could carry spillover effects into other sectors. One example is that the Canada Revenue Agency’s 35,000 workers may strike before the tax filing deadline in order to secure large wage gains of over 30% both retroactively and going forward. Another example is that the Ontario government awaits the ruling on its appeal of a lost court decision that declared the 1% imposed wage settlement upon its workers to be invalid and subject to retroactive and forward adjustments.

7. Productivity—A National Embarrassment

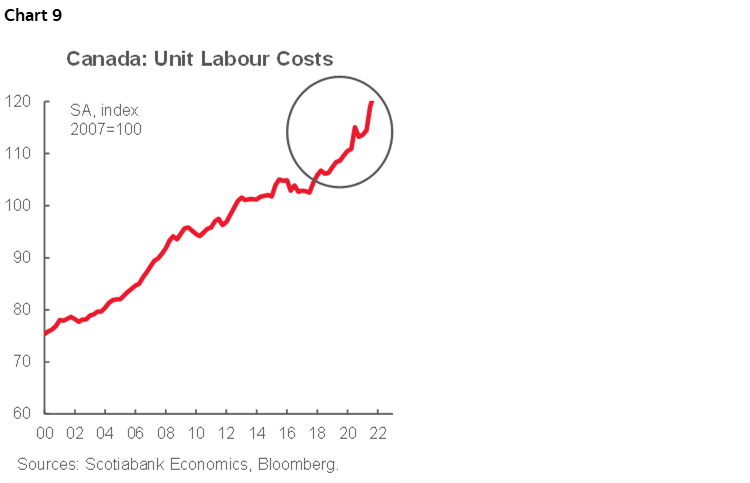

Output per hour worked fell again in the final quarter of 2022. Just when a couple of quarters of miserly productivity growth were starting to offer some hope, bang, the country goes back to the stretch of seven consecutive quarterly declines in labour productivity from 2020Q4 through to 2022Q1. Wage growth has to be evaluated in the context of soft productivity trends since getting paid more to produce less would be an inflationary impulse through labour markets. The result has been an ongoing acceleration of unit labour costs—a proxy for productivity-adjusted employment costs—that began years before the pandemic (chart 9).

8. GDP—Better Under the Hood

The BoC’s forecast for Q4 GDP growth (1.3% q/q SAAR) was surprised to the downside when it came in unchanged. There will be a statement reference to this, but in the past, they have also pointed out when there were distortions to figures such as happened this time.

December was a highly distorted mess of transitory influences that weighed down growth and we already have preliminary guidance that January rebounded by 0.3% m/m. We can also point to strong tracking for hours worked into Q1 (chart 10) which matters since GDP is an identity defined as hours times labour productivity. Q4 GDP growth was weighed down by the biggest inventory drag effect in over four decades and partly offset by an import addition to growth that on net involved a substantial 1 ¼% hit to GDP growth. Expect the BoC to instead reference a mild 1% gain in final domestic demand, defined as consumption plus investment plus government spending, while also referencing a mild gain in exports.

They could reference expectations for stronger Q1 growth than their 0.5% q/q annualized forecast in the January MPR. The largest inventory drag effect on growth in over four decades may be unlikely to return as a further drag in Q1. Please see a full recap of these arguments here.

BANK OF JAPAN—FAREWELL MR. KURODA

No policy changes are expected when the Bank of Japan’s latest decision arrives on Friday. It may matter only for sentimental reasons as this will be Governor Kuroda’s final meeting at the helm.

Kuroda deserves high accolades for aggressive experimentation in an effort to confront decades of disinflationary pressures in Japan’s economy. The extent to which it worked is mixed. We can’t observe the control experiment of what might have happened to Japanese inflation and its economy in the absence of massive stimulus, but we also can’t say decisively that Japan has durably emerged from disinflationary pressures. It is very unlikely that Kuroda will embrace change in his final meeting which is likely to be of more ceremonial significance than anything else as potential changes are likely to be left to his successor.

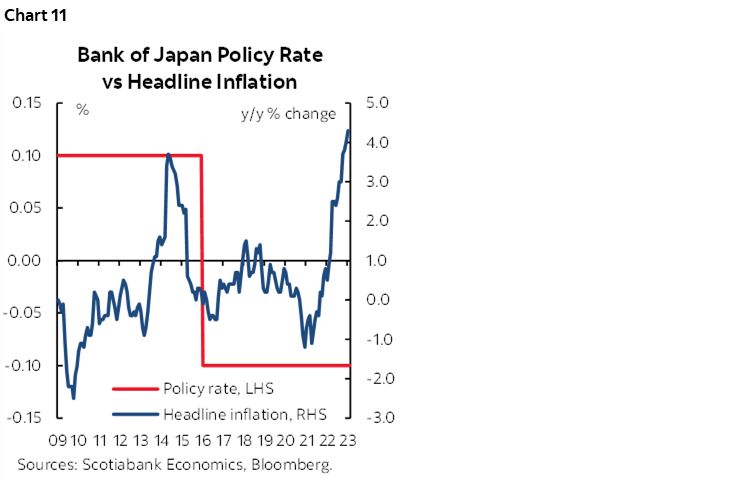

A holding pattern is likely in place at least until Spring wage negotiations with unions have been completed and Governor-designate Ueda perhaps launches a policy review. For now, Ueda’s confirmation testimony on February 24th brought guidance on inflation by saying “This should be the peak for now” and that more time was needed to durably hit 2% through broader forces than cost-push influences like the lagging effects of yen depreciation and oil prices on inflation (chart 11). Recall that BoJ staff research has shown that yen depreciation and higher oil prices have lagging but transitory effects on inflation that are likely to wane this year into next. Ueda also leaned against any need to raise interest rates barring surprising developments that achieve 2% inflation for longer.

RBA—SOMETHING IN COMMON WITH THE BoC

Consensus unanimously expects the Reserve Bank of Australia to hike its cash rate target by another 25bps on Tuesday night (eastern time as always in this publication). Markets are a little less sure with almost 80% odds of a 25bps hike priced into futures markets.

Key may be forward guidance albeit that the RBA is between forecast cycles and has already indicated that further hikes are ahead. Markets are pricing cumulative rate hikes of between ¾% and 1% from the present 3.35% target rate.

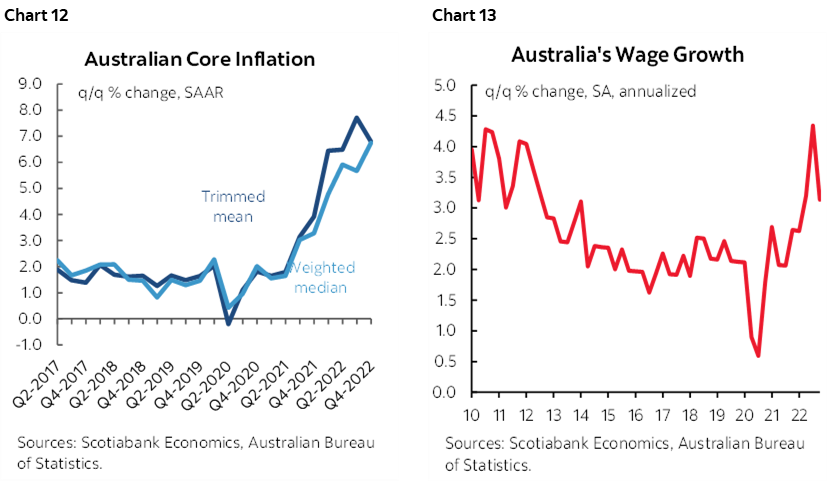

The RBA had embraced somewhat of a more moderate bias toward the end of 2022 only to return with a further 25bps hike on February 6th with a hawkish bias that followed hot inflation and wage readings (charts 12, 13). The dangers of prematurely halting hike cycles only to have to return with more later offer a common parallel between the RBA and the BoC.

PERU—A HOLDING PATTERN

No change is expected when Banco Central de Reserva del Perú delivers its latest policy decision on Thursday. This would be the second consecutive pause after the surprise hold on February 9th.

Our Lima-based economist Guillermo Arbe argues that inflation is showing signs of stabilization after CPI landed below consensus at 8.65% y/y while the pace of month-over-month changes has been gradually ebbing over the past year.

BANK NEGARA—RENEWED RISK?

Bank Negara Malaysia is also expected to hold its overnight policy rate unchanged at 2.75% on Thursday. Inflation has ben gradually cooling to 3.7% y/y in January. A wild card risk may be focused upon the ringgit’s renewed depreciation to the USD and monitoring risks to financial stability. The currency had been gaining ground since November but has resumed a weakening path over the past month as the Federal Reserve’s hiking plans became repriced in markets.

NONFARM PAYROLLS—RESILIENT JOB MARKETS

Time for another swing at forecasting US job growth! Good luck. I’ve guesstimated a gain of 240k with wage growth of 0.3% m/m or 3.7% at an annualized pace.

Multiple readings point to continued resilience in the US job market including the following.

- ISM-services indicated that job growth picked up with a reading of 54 from 50 the prior month. A number above 50 indicates expansion.

- ISM-manufacturing indicated that employment growth in the manufacturing sector cooled with a slightly sub-50 reading.

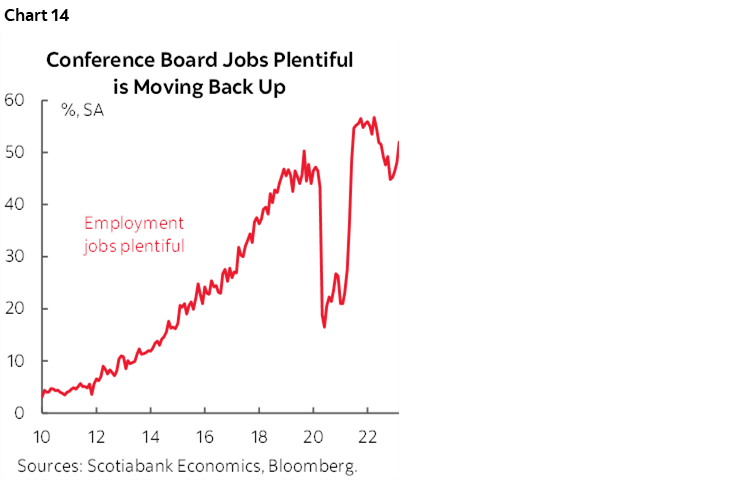

- The Conference Board’s consumer confidence measure of ‘jobs plentiful’ continued to rise in February (chart 14).

- Weekly initial jobless claims were stable at low levels between the January and February nonfarm payroll reference periods.

This week will also bring out a few additional measures. ADP payrolls for February (Wednesday) will only matter if it sharply deviates from consensus expectations for nonfarm payrolls. When it does so, there are improbable odds of achieving the consensus expectations for nonfarm in whatever direction ADP surprises. Otherwise, ADP is too unreliable as a nonfarm leading indicator.

JOLTS job openings for January (Wednesday) and Challenger job layoffs during February (Thursday) will round out the job market readings. The National Federation of Independent Business will update its measures for small business hiring plans and job openings that are hard to fill sometime this week.

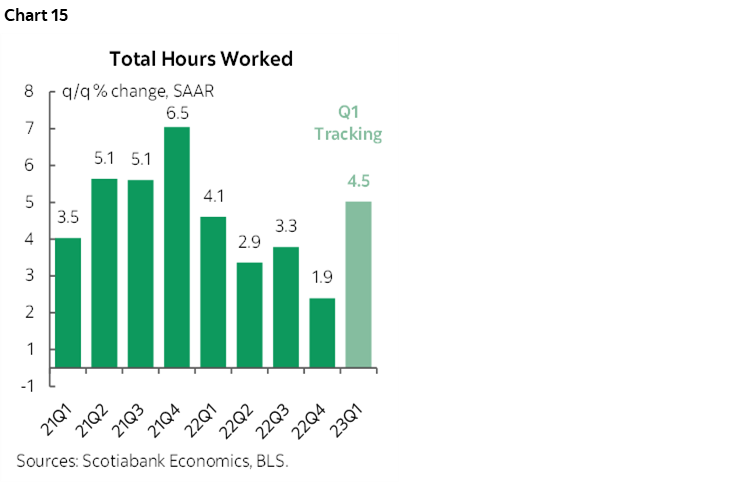

In the overall set of nonfarm and household survey figures one of the added gems will be additional tracking of hours worked. 2023Q1 is tracking a powerful gain that indicates strong GDP growth since GDP is an identity defined as hours times labour productivity (chart 15).

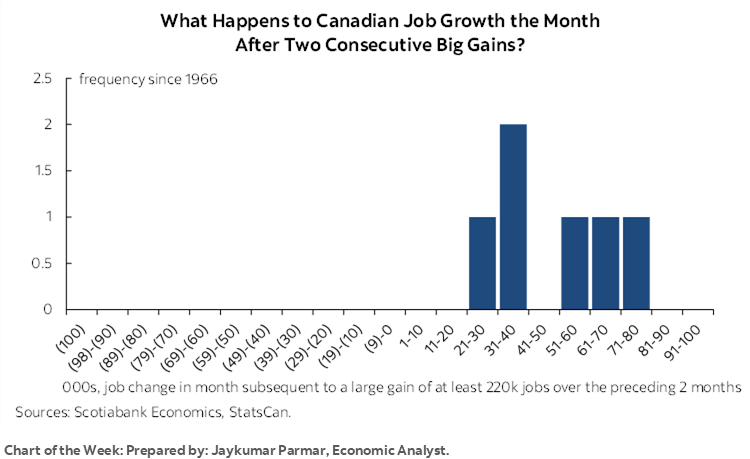

CANADIAN JOBS—MOMENTUM FAVOURS THE BOLD

Canada updates job market conditions during the month of February on Friday. Key will be whether momentum can be maintained and further evidence to inform whether wage growth has hit a soft patch or something more durable. I have tentatively gone with a gain of 10k jobs and a stable unemployment rate.

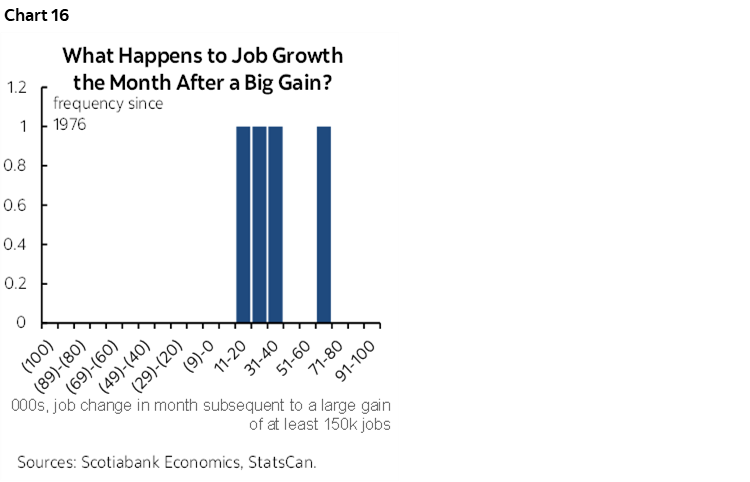

After 220k jobs created in two months the next figure must certainly be lower, right? Well, not so fast.

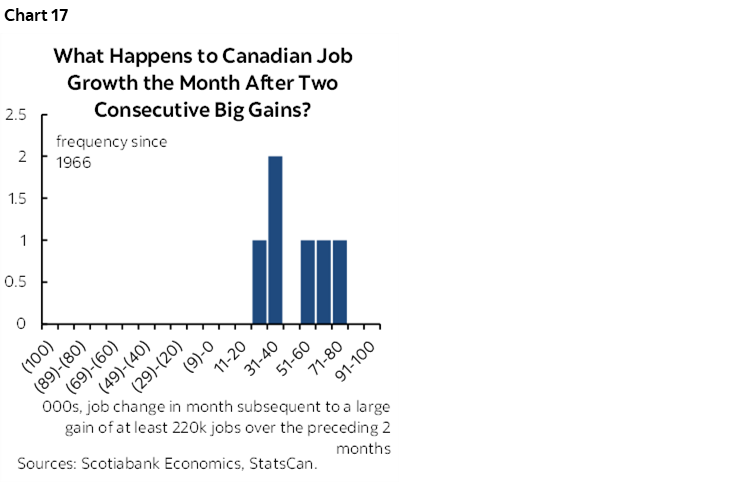

Momentum favours the bold among employers it seems. First, every time jobs have risen by 150k (as in February of this year) or more, the next month has always been higher (chart 16).

Second, when back-to-back gains have totalled 220k (as in December and January this time) or more, the next month has always been another gain (chart 17).

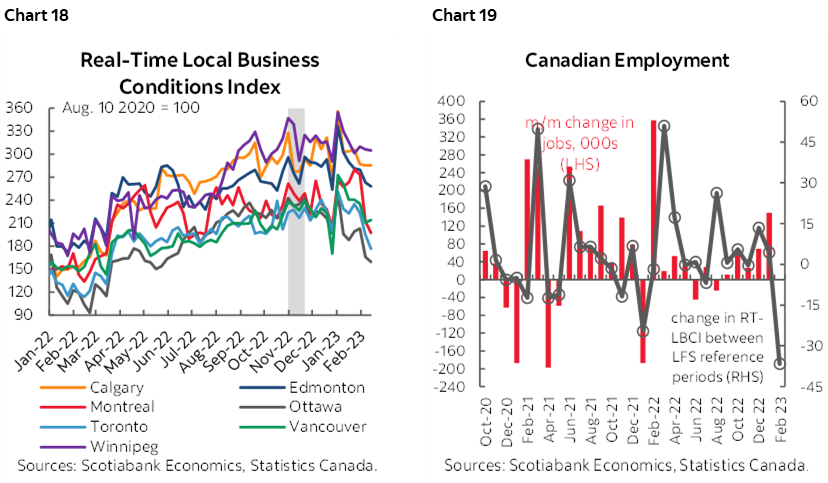

The fly in the ointment lies in the fact that measures of mobility and activity in opening and closing businesses have soured. This so called alt-data is not seasonally adjusted, but the turn lower in Statistics Canada’s real-time local business conditions index—a composite of mobility and business register figures—has been greater than seasonally normal and may portend softening (chart 18). Chart 19 takes a weighted average of the individual cities and turns them into a national gauge that is loosely correlated with monthly job growth.

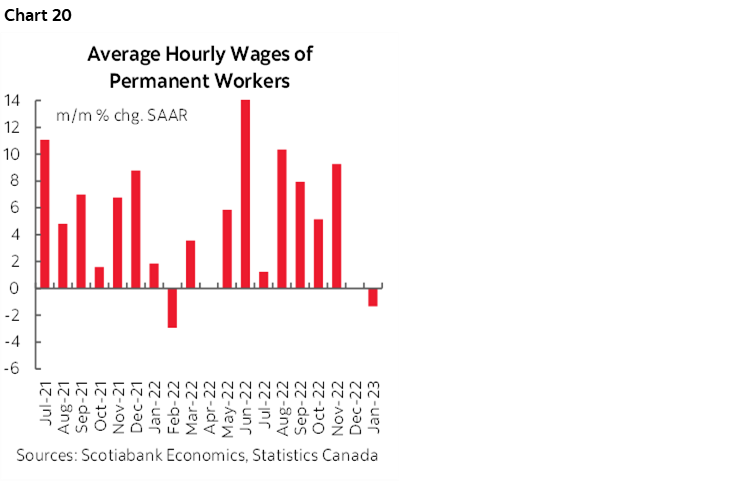

Also watch average hourly earnings during February after they have hit another soft patch in the past couple of months (chart 20) and wage settlement figures for large contractual negotiations for January that will arrive earlier in the week.

OTHER MACRO—CHINA THE MAIN ATTRACTION

China will figure prominently in terms of the rest of the global line-up of developments over this coming week.

China’s National People’s Congress (the NPC) commences its new annual session at the start of the week. A parliament in an undemocratic system, that’s a good one. Anyway, economy watchers will want to monitor the introduction of fiscal budgets and potential measures. An annual growth target will be set along with a fresh annual inflation target.

China will also update inflation figures for February. Headline inflation is expected to slip beneath 2% y/y and hence well below the 3% target, but core inflation will matter more. It has been gently rising to 1% y/y. Producer prices will be updated at the same time on Wednesday. Trade figures early in the week and perhaps a fresh round of social credit figures are due.

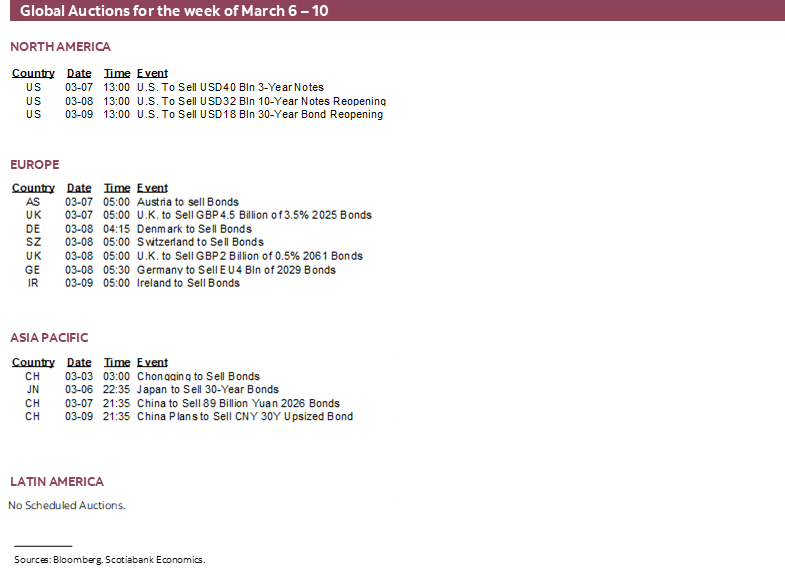

Canada’s calendar will be dominated by the BoC and jobs with only the Ivey PMI for February (Monday) and trade figures for January (Wednesday) to consider as well.

Apart from the BCRP’s policy decision on Thursday, Latin American markets will also take down a series of inflation reports. Colombia kicks it off with a February update on Saturday. Chile follows next on Wednesday and then Mexico the next day and Brazil on Friday.

A few other Asian CPI inflation reports will come from South Korea (Sunday), Thailand (Monday and Taiwan (Tuesday).

Europe’s macro calendars will be light. Highlights will include UK macro releases on Friday including January releases for GDP, industrial output, a services index, construction output and trade. Germany reports factory orders (Tuesday) followed by retail sales and industrial output (Wednesday). Also watch CPI from Norway (Friday) and Switzerland (Monday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.