Next Week's Risk Dashboard

- US nonfarm: still beating consensus?

- Canadian jobs expected to rebound

- FOMC minutes: back-to-back?

- Can the RBA surprise a third time?

- Bank Negara likely to hold

- PMIs: US, Canada, Japan, Brazil, Mexico, Sweden

- LatAm and Asian CPI

- Global Indicators

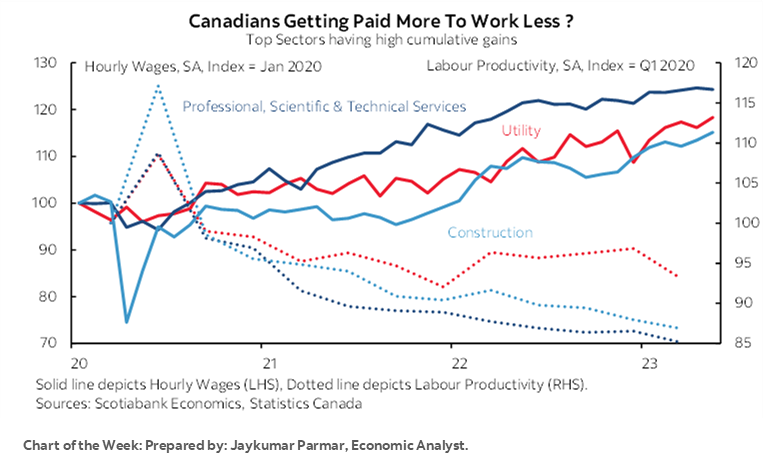

Chart of the Week

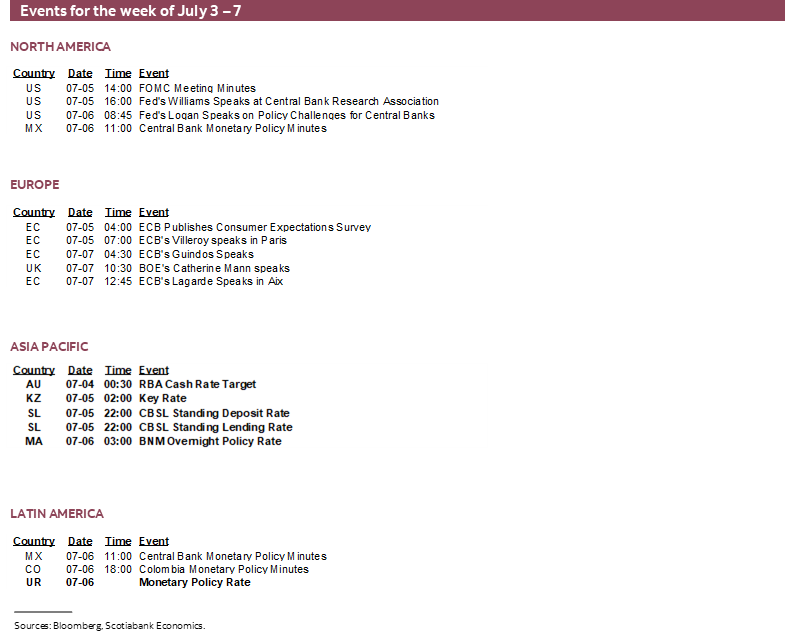

This weekend, Canada will celebrate its 156th birthday since the British North America Act was passed on July 1st 1867 with Monday being a statutory holiday, and then on Tuesday, the US will celebrate Independence Day that marks the Declaration of Independence that was ratified by Congress on July 4th 1776. Both occasions are likely to mean limited participation in global markets from clients across the northern two-thirds of North America until at least mid-week. With the spirit of the holidays in mind, this issue of the Global Week Ahead is going to be a lighter one. Enjoy your BBQs or however you plan to spend a well-deserved break. The fact that this will also be a lighter than usual week for global calendar-based market risks doesn’t hurt.

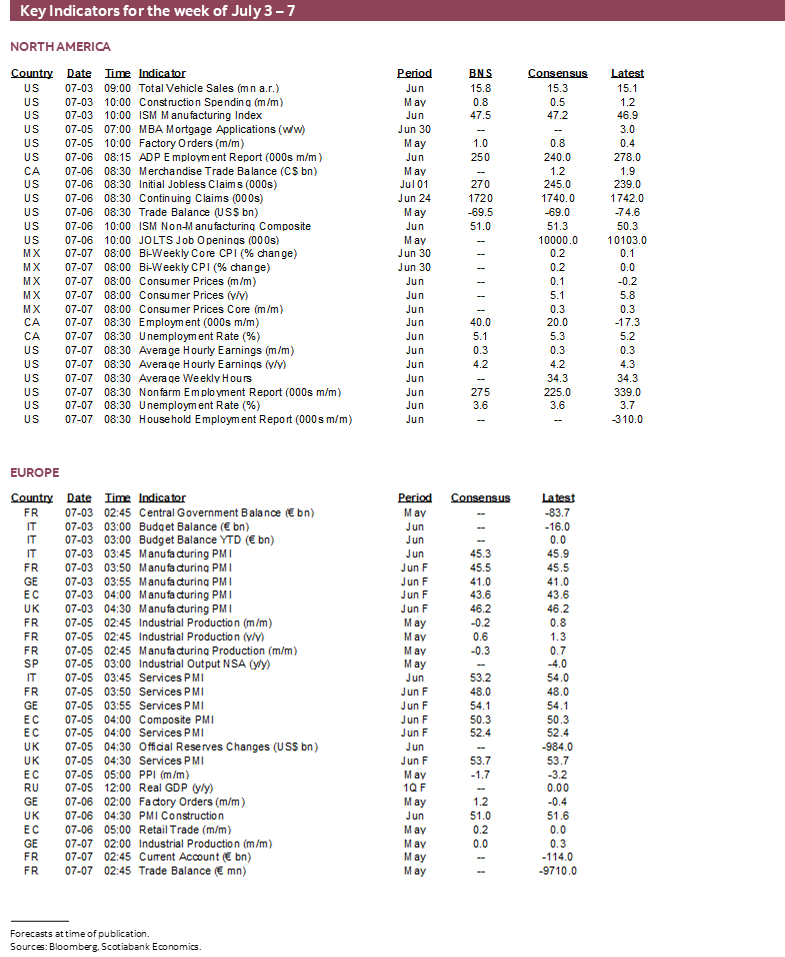

Much of the week’s risk will be back-end loaded to Friday’s US and Canadian hopefully sizzling job market updates. Key highlights for the week’s expectations are laid out below.

CANADIAN JOBS AND WAGES—RRRRRREBOUND?

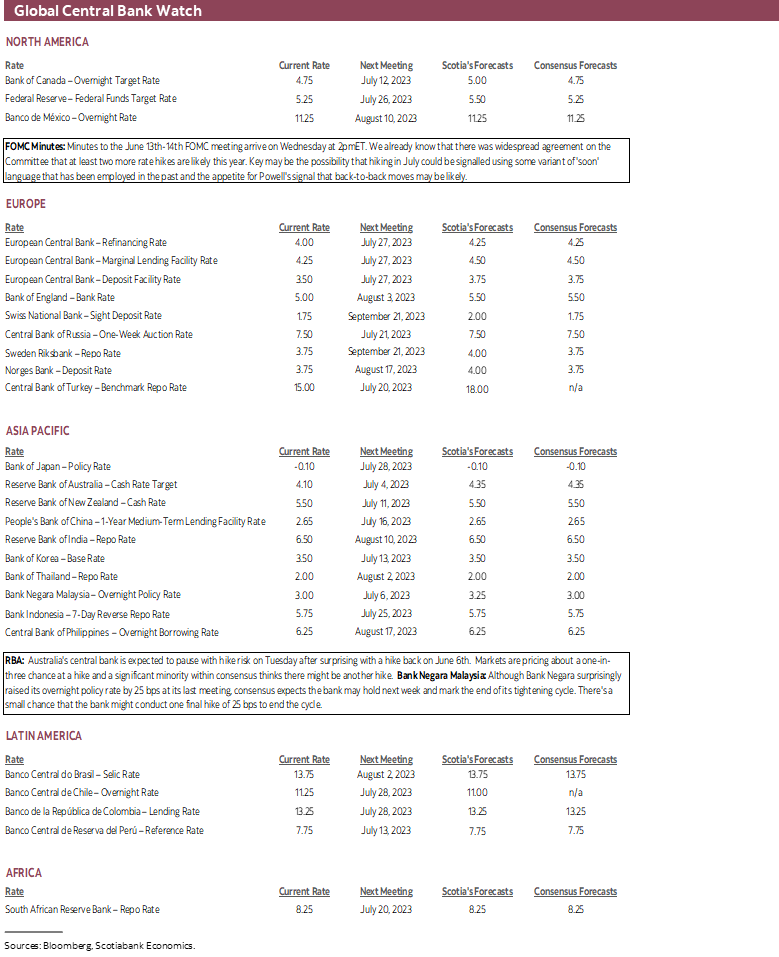

Canada updates jobs and wages for the month of June on Friday. This will be the final piece of the puzzle to be laid in place ahead of the following Wednesday’s statement, Monetary Policy Report and press conference to be delivered by the Bank of Canada.

Recent data has been somewhat mixed but generally supportive of hiking when coupled with a forward bias concerned about renewed upside risk to inflation and unmoored inflation expectations. Perhaps the strongest argument for hiking in July, however, is that a whiff could motivate easier financial conditions and a pile-on into the front-end relative to what is currently priced. Markets are pricing another 25bps hike and part of another over coming meetings and may take a pause as a sign of wavering with the next move more likely to be down. That could be a setback to the focus upon containing inflation risk.

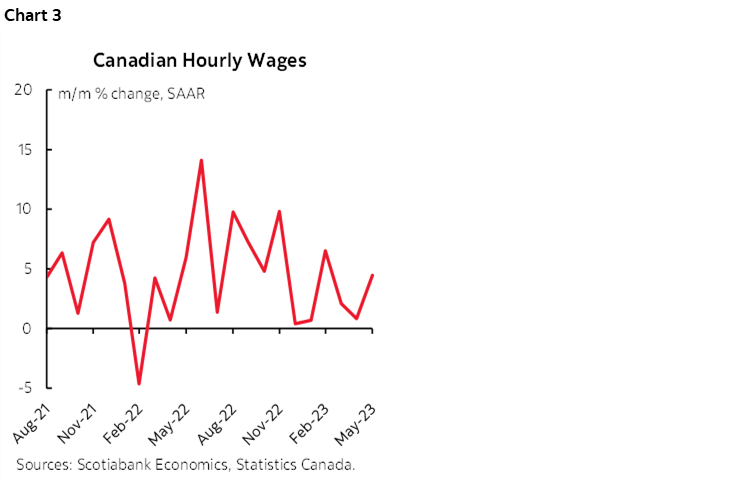

I’ve gone with an estimated 40,000 increase in jobs with a slight downtick in the unemployment rate to 5.1%. Wage growth will be a wildcard after the strong 4.5% m/m SAAR rate of increase in May.

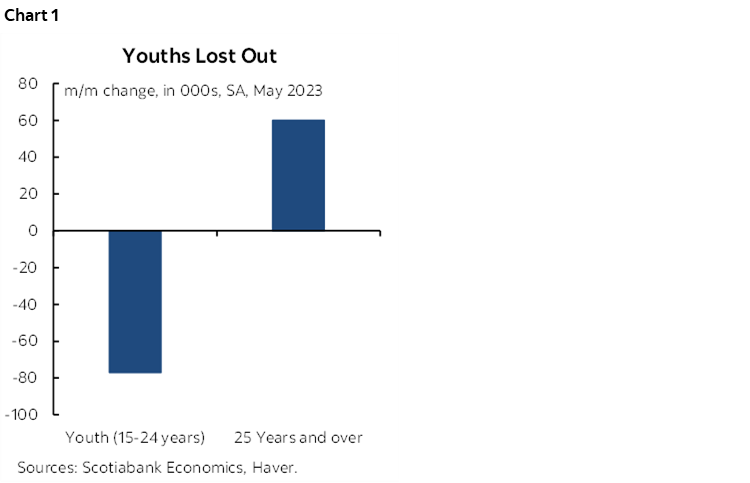

Among the reasons for expecting a rebound are that the prior month’s narrowly based shocks that drove a mild 17k drop in jobs are expected to shake out. Recall that a weaker summer jobs market drove a 77k drop in youth employment aged between 15–24 (chart 1). That was likely a one-off at the traditional start of the summer jobs market and offers a stronger springboard effect off of which to rebound in June.

There was also a 40,000 drop in self-employed positions during May whereas payrolls were up by 22k. Self-employed jobs are an important part of the Canadian economy, but it’s shakier and more volatile data such that this effect should also stabilize into June.

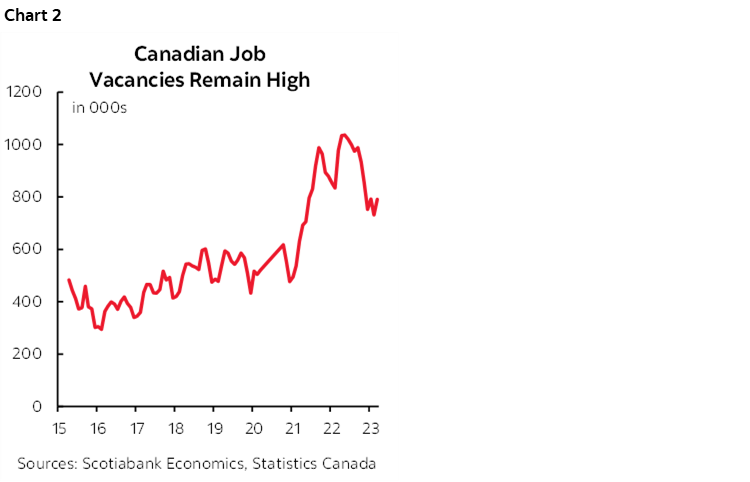

At the same time, job vacancies remain high but have pulled off the peak (chart 2). This probably reflects ongoing appetite for hiring at an above-trend pace.

Canada’s job market has nevertheless been on fire this year. A net 231k jobs have been created on a year-to-date basis. Because the labour force has expanded by slightly more (+280k ytd), the unemployment rate has edged up a touch to 5.2% from entering the year at 5%.

As for volatile wage growth (chart 3), key may be when several collective bargaining agreements in the public and private sectors begin to show up. For instance, the recent pay agreements for Federal civil servants can take up to 180 days to be implemented by the Treasury Board. Wages, however, must be viewed in relation to productivity growth that remains abysmal in Canada such that any trend wage gains in relation to poorer productivity pose inflationary risk to the economy.

US NONFARM AND WAGES—CONTINUING UPSIDE RISK?

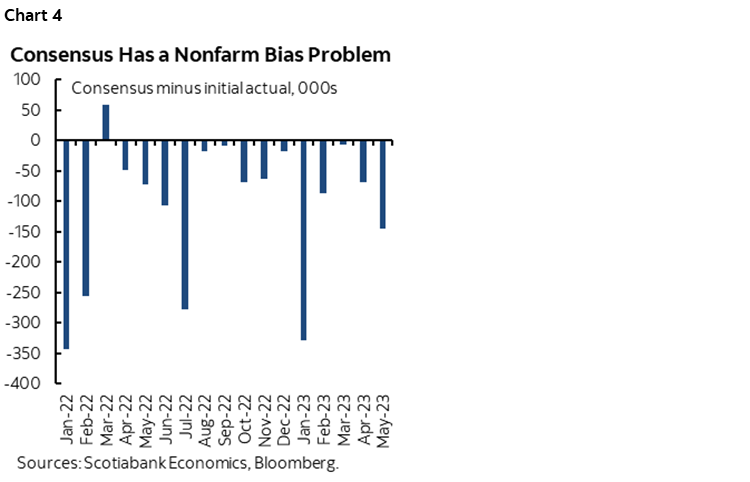

The US updates nonfarm payrolls and wages along with broader labour force metrics for the month of June on Friday. Given that consensus has persistently underestimated growth in nonfarm payrolls for an extended period (chart 4), it would seem that recent history is on the side of going above consensus again.

I’ve guesstimated a gain of 275k with a slight downtick in the unemployment rate to 3.6% and trend wage growth of around 0.3% m/m SA. At the time of publication, that is a modest 50k above the median estimate with most forecasters ranging between about 200–250k.

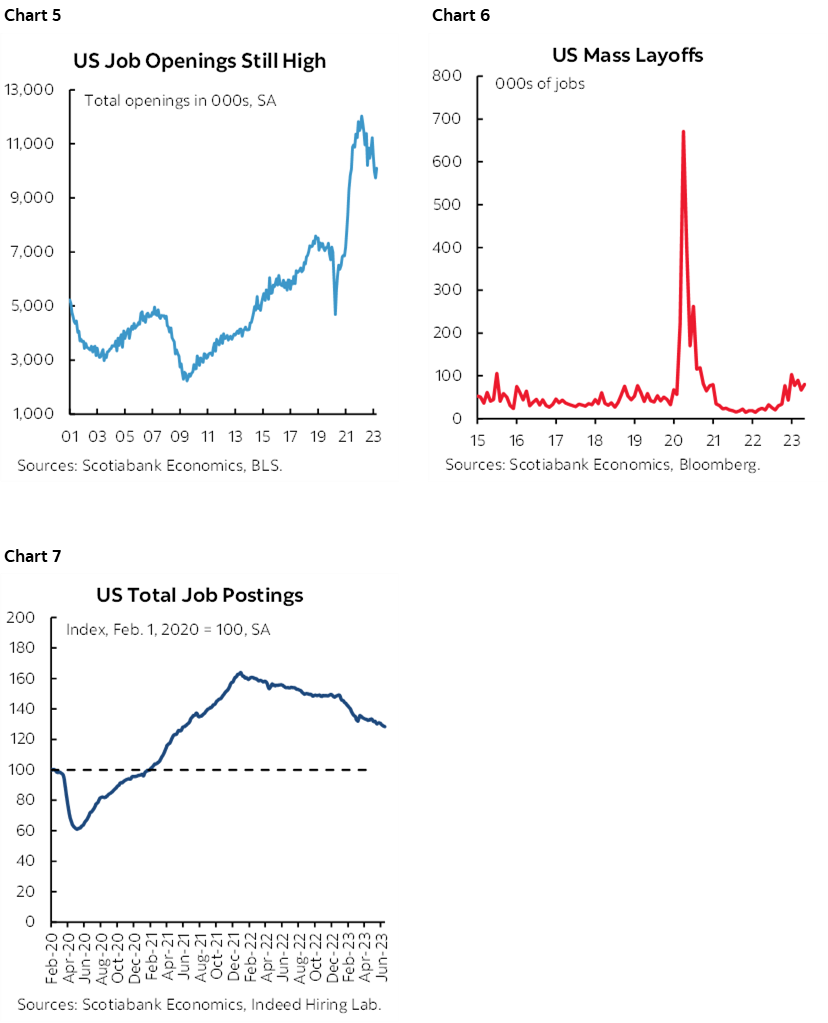

A supporting factor is that job vacancies still remain high (chart 5). Layoffs remain low (chart 6). Job postings are trending softer but are still supportive of job gains (chart 7). Initial jobless claims were modestly higher between the May and June nonfarm reference periods defined as the pay period including the 12th day of the month.

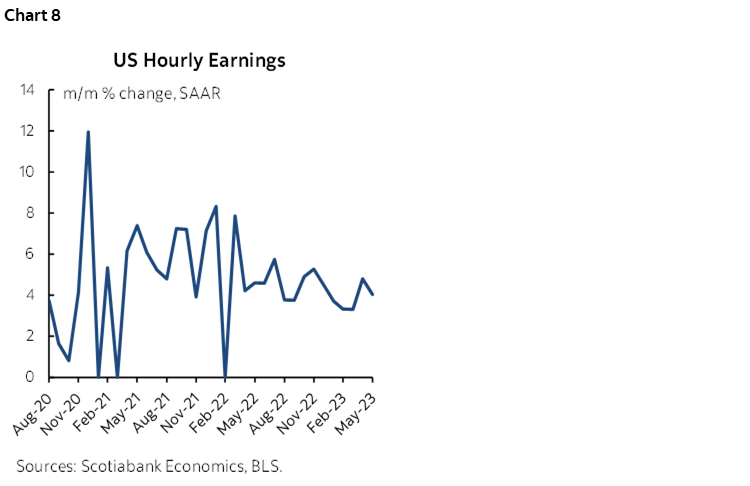

As in Canada, key may be wage growth that really hasn’t been doing all that much this year (chart 8). Wages have been up by 0.3% m/m in four of the five months to date this year (0.4% in April) and this has kept nominal annualized wage growth elevated but without posing material gains in real wages.

Other readings throughout the week may further inform payrolls expectations. JOLTS job openings during May arrive on Thursday. ADP payrolls land on the same day and usually only matter to nonfarm expectations if there are wild swings. The week’s ISM-manufacturing and ISM-services releases may also contain useful information in terms of hiring attitudes.

CENTRAL BANKS—UNCLE!

Only two central banks will deliver policy decisions over the coming week while the Bank of Canada goes into communications blackout ahead of the following week’s decisions and each of the Fed, Banxico and BanRep issue minutes to their recent meetings. This should be a generally welcome reprieve from the onslaught of central bank communications over recent weeks.

FOMC Minutes—How ‘Soon’?

Minutes to the June 13th–14th meeting land on Wednesday at 2pmET. A recap of that meeting is available here. We already know that there was widespread agreement on the Committee that at least two more rate hikes are likely this year. Key may be the possibility that hiking in July could be signalled using some variant of 'soon' language that has been employed in the past. Markets are mostly priced for a 25bps hike on July 26th. Also key may be appetite for compressing the two hikes shown in the dot plot into back-to-back decisions given Chair Powell's recent remarks versus the uncertainty that accompanies being data dependent.

RBA—You Started It!

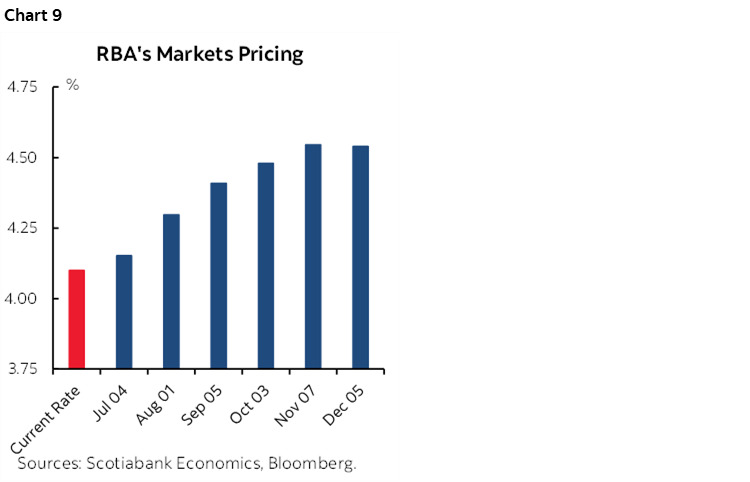

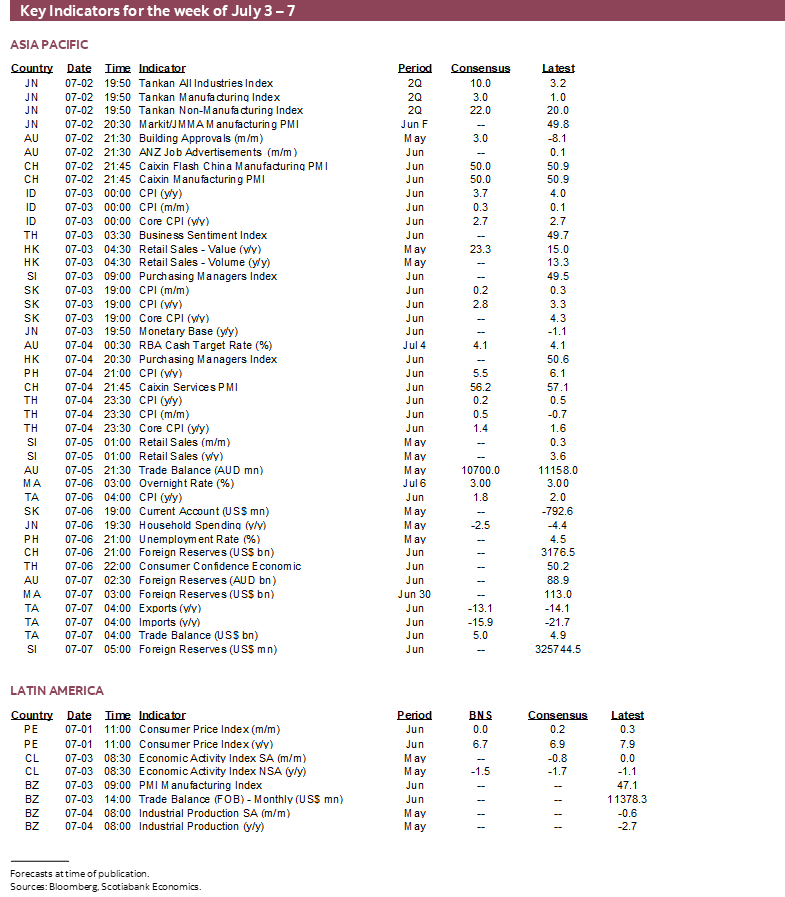

Think back to May 2nd and June 6th. On both occasions, the Reserve Bank of Australia surprised consensus with 25bps hikes. Now here we go again with consensus once again expected no change to the cash rate of 4.1% this Tuesday but with markets pricing a return to hiking later (chart 9).

This time, however, it’s a razor thin divide between a hike expected by 13 forecasters and no hike expected by 14. Markets have been flirting with around one-in-three odds of a hike. Since the last hike, job growth smashed expectations at 76k (18k consensus) but monthly CPI for May landed shy of expectations. The labour market remains very tight with an unemployment rate hovering around a record low of 3.6% which may provide cover for a hike in the context of wage-Phillips curve and traditional wage-price Phillips curve connections.

Bank Negara Malaysia—No Surprise This Time?

Although Bank Negara surprisingly raised its overnight policy rate by 25 bps at its last meeting, consensus expects the bank may hold this Thursday and mark the end of its tightening cycle. Recently softer than expected inflation (2.8% y/y from 3.3% prior) could be pointed to as a further sign of progress. There's a small chance that the bank might conduct one final hike of 25 bps to end the cycle.

Minutes to Banxico’s decision on June 22nd to hold the overnight rate at 11.25% land on Thursday with little expected by way of guidance beyond a nearer-term pause. Minutes to BanRep’s decision this past Friday when they held the overnight lending rate at 13.25% also arrive Thursday.

GLOBAL MACRO—THE LEFTOVERS

There won’t be a whole lot else to consider over the coming week.

Other US indicators will include ISM manufacturing (Monday) and ISM-services (Thursday), both of which may improve somewhat given tracking for retail sales, vehicle sales and production, plus regional manufacturing surveys produced by Federal Reserve district banks. Construction spending may get a lift from housing (Monday). Vehicle sales are expected to jump by 5% m/m SA during June (Monday). Factory orders (Wednesday) should follow durable goods orders higher with the addition of nondurable goods orders. The trade deficit is expected to narrow as a stable services surplus is added to a modestly improved merchandise trade deficit (Thursday).

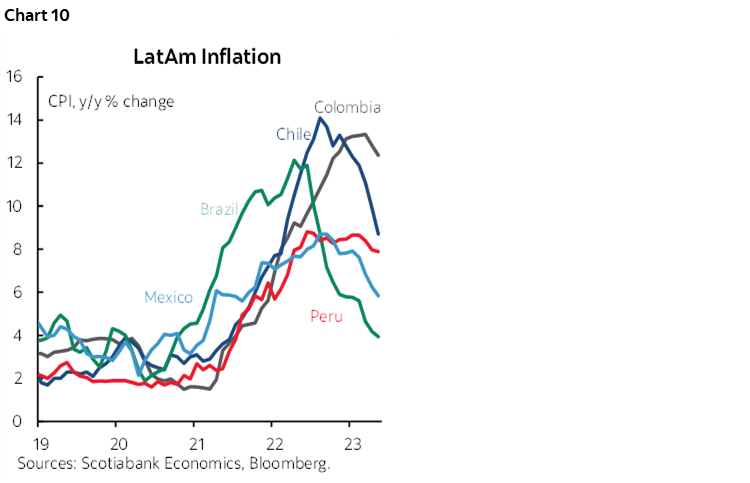

A wave of CPI inflation reports primarily across Latin American (chart 10) and some Asian markets will begin to arrive on Saturday (Peru) followed by Indonesia, South Korea, and Switzerland on Monday, Philippines and Thailand on Tuesday, Taiwan on Thursday and then Mexico and Peru on Friday.

Canada’s main focus will be upon jobs and wages, but trade figures for May (Thursday) could enhance Q2 GDP growth tracking. The Ivey PMI for June lands Friday.

European calendars will offer light risk primarily focused upon Germany trade (Tuesday) and factory orders (Thursday) during May.

Some survey-based readings on business conditions will include Japan’s Tankan Q2 readings (Sunday), China’s private PMIs following the recent declines in the state PMIs (Tuesday ET), and PMIs from Mexico and Sweden (Monday) and Brazil (Wednesday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.