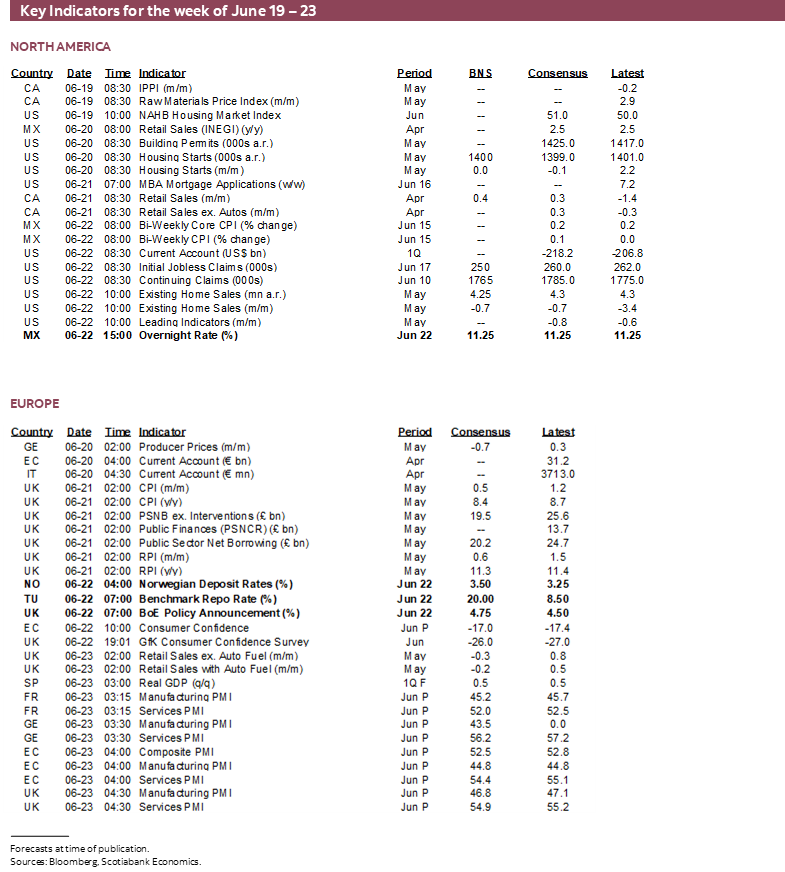

Next Week's Risk Dashboard

- AI may pose nearer term inflation risk

- Supply chains remain pressured across multiple sectors

- BoE: Frontload more and do less later?

- Fed’s Powell returns

- The BoC’s not-minutes minutes

- The PBoC’s aftereffects

- Estimating Banxico’s holding period

- Chile’s central bank nearing policy easing?

- Brazil’s central bank slowly pivoting

- Could Norges Bank upsize again?

- SNB tail risk

- Bank Indonesia landing on target

- Philippines CB on a ‘prudent pause’

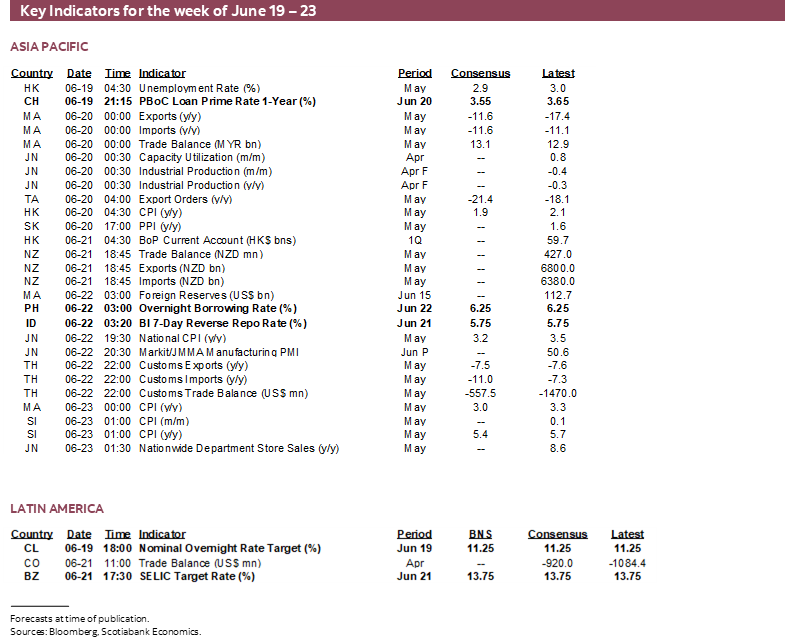

- CPI: Japan, UK

- PMIs: EZ, US, UK, Australia, Japan

- Global macro: UK, Canadian retail sales, US housing

- US markets shut on Monday for Juneteenth

Chart of the Week

Is it happening all over again? For that matter, did it ever really end? Are supply chains faced with another round of deteriorating conditions, or have they even posted as much improvement as one might think? Part of the outlook for inflation depends upon the answers and so does the outlook for yet another wave of global central bank decisions that will be upon us over the coming week.

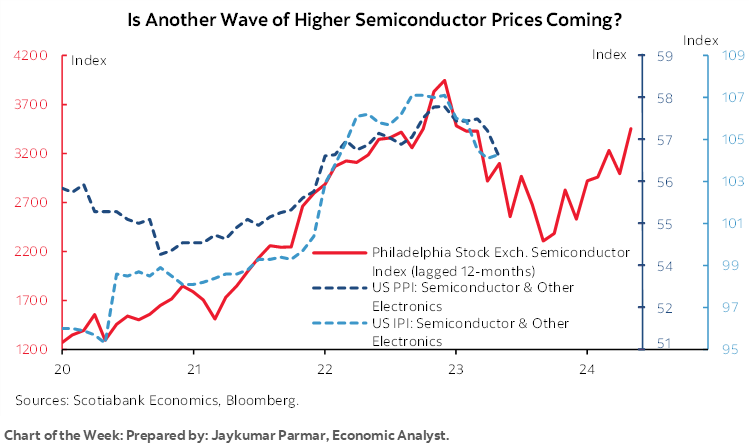

For starters, the narrative around semiconductors may be rapidly changing as the drivers shift from pandemic shortfalls to AI-induced shortages that are also driving positive wealth effects across equity markets. Enter chart 1.

The Philadelphia Semiconductor index (SOX) is a capitalization-weighted market measure derived from share prices of firms aligned with the semiconductor business. The SOX gauge is up by 70% since the low in October and about 25% over just the past month or so. There has recently been about a one-year lag between movements in this market index and movements in more direct measures of semiconductor prices in the US producer price index and the US import price index. That relationship was more mixed historically as pre-pandemic changes in SOX were correlated with import prices of semiconductors but not with persistent declines in the PPI semiconductors gauge. That mixed pre-pandemic period could have been because the USD was generally strengthening over the second half of last decade.

It's possible—not assured—that the surge in demand for semiconductors that is significantly related to AI is priced into equities before either the prices for semiconductors themselves fully adjust and/or before supply shortages creep back into the picture. It’s also possible that SOX is simply getting frothy. But even if the truth lies in between, the recent downdraft in the PPI and import price gauges for semiconductor prices could be temporary and could give way to higher prices should this market sentiment be followed by renewed supply shortages.

If that happens, then the warning here is to brace for potential rolling announcements about production disruptions across sectors that are already dealing with supply challenges. In short, AI could be replacing the pandemic as the source of supply disruptions given how omnipresent semiconductors are across so many of today’s products and computing services. At least in the short-term, this narrative could turns on its ear the notion that AI offers disinflationary effects. In last week’s Global Week Ahead I expressed healthy skepticism toward the longer-term effects while leaving the door open to the disinflationary possibility, but the shorter-term pressures within the realm of central bank policy horizons may be very different.

Charts 2–8 offer other perspectives on supply chains.

- Supply chains are not improving in housing, they're going the other way as evidenced by tight inventory and sales-to-listings in several countries.

- Supply chains are not materially improving in terms of labour scarcity. The Beveridge Curves across major countries continue to point to simultaneously high job vacancies and low unemployment rates.

- Supply chains are not improving in autos, such as seen in record low US vehicle inventories.

- Supply chains are not improving across airplanes, whether we're talking manufacturing or airlines. Boeing, for instance, has a 10+ year order backlog. Pilots’ wages are going sharply higher across several N.A. airlines. China is scrambling to hire pilots and seeking more openings in foreign flight training schools.

- Other indicators are mixed, such as ongoing improvements in Ocean transit times (here), or the improved Baltic Dry index of shipping costs, or the New York Federal Reserve’s measure of global supply chain pressures. Others are not really improving or not enough, like the Class 8 heavy truck order backlog that remains high in N.A. indicating high demand for heavy equipment, or the order backlog for Japanese machine tools.

CENTRAL BANKS—MORE SHOCKS?

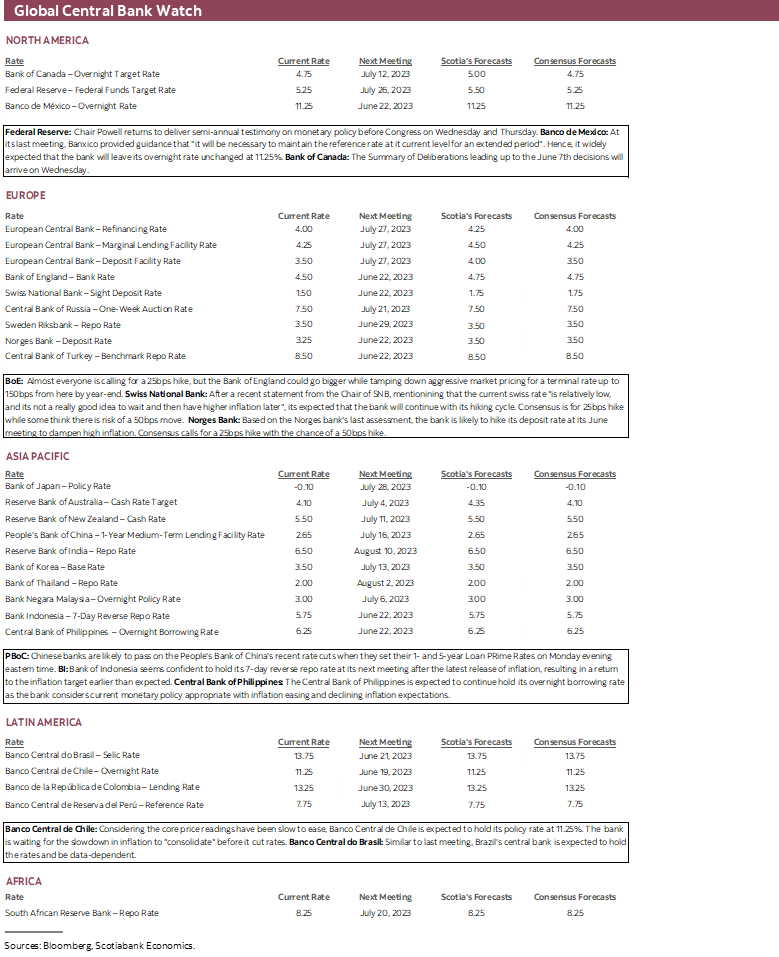

Global markets will not only have another chance to hear from the Federal Reserve and Bank of Canada in the wake of recent policy surprises, but will also take down potential further surprises across a wave of other central bank decisions. There is significant uncertainty around decisions and guidance from the Bank of England, the Swiss National Bank, Norges Bank, a trio of LatAm banks including Mexico, Chile and Brazil, plus a pair of Asian central banks (BI, BSP). The after effects of PBoC easing will bring lower rates to Chinese borrowers.

Bank of England—50 and Then Less?

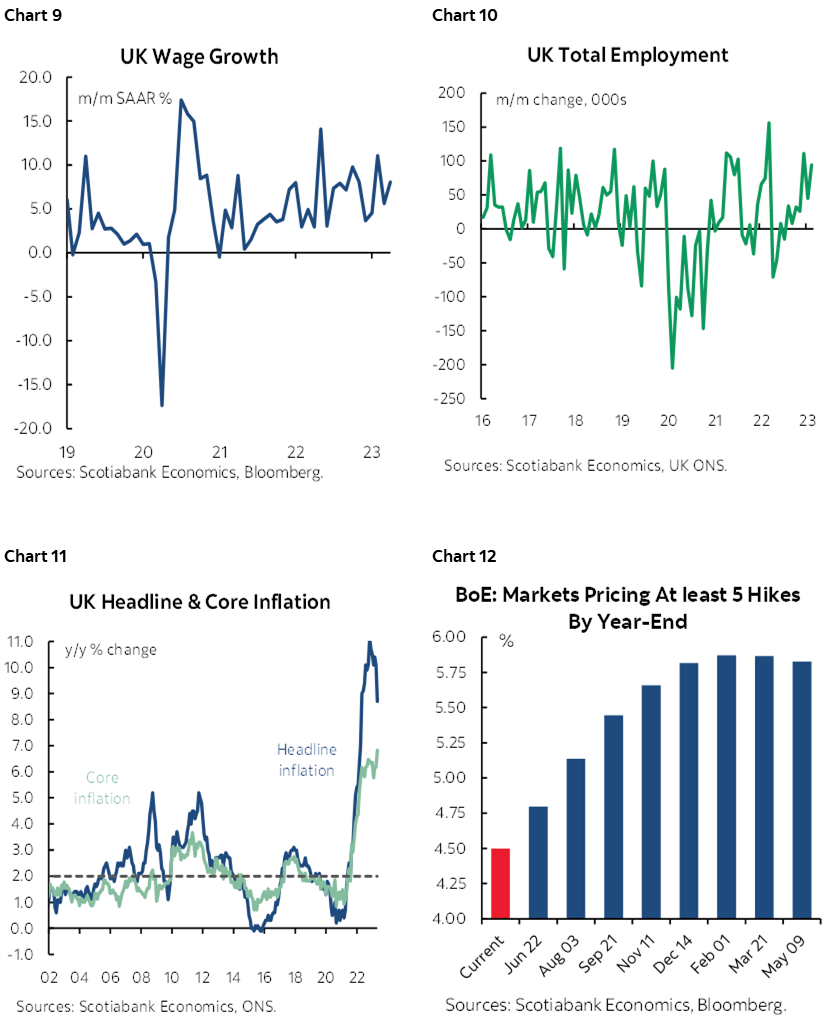

Consensus and markets are in universal agreement toward expecting a 25bps hike in Bank Rate on Thursday. Uh oh. This is, after all, a central bank that has surprised everyone on past occasions and that wears this with a combination of insouciance and honour. The scope for surprise, however, could take one or both of two forms.

In this case, the speculation for some time now has been whether 25bps would be enough, or if something bigger may be delivered. Many central banks have been surprising markets of late, including the Federal Reserve’s pause-but-two-more guidance, the fact that the ECB left the door open to more hikes than are priced, the BoC, the RBA and even hawkish forward guidance from the RBI.

How could they justify a bigger move? By pointing to accelerating wage growth (chart 9), job growth (chart 10) and core inflation (chart 11) and conditioning the move on their data dependence. The overall impact upon market pricing depends upon how the MPC manages forward guidance. OIS markets foresee another 125–150bps of tightening before reaching a terminal Bank Rate of up to 6% from 4.5% at present by the end of this year or early next (chart 12). Should the BoE be strongly of the view that such pricing is aggressive then it could provide such cues while frontloading a faster response to recent pressures.

Federal Reserve—Powell’s Second Chance

Chair Powell will be in the hot seat again when he delivers his semiannual Monetary Policy Report and testimony to Congress first to the House Financial Services Committee on Wednesday (10amET) and then to the Senate Banking Committee the next day at the same time.

A recap of the past week’s FOMC communications is available here. Markets are haircutting the revised dot plot both in terms of hike and cut guidance. Fed funds futures are pricing barely one out of the two hikes that were shown in the latest plot, while they are pricing earlier and larger rate cuts next year than the dot plot guides. The muddled messages that were aimed at appeasing the consensus opinion on the FOMC are therefore not terribly convincing to market participants. Powell may not have confidence to influence market pricing and is more likely to reinforce guidance that they are pausing to evaluate conditions before ‘nearly all’ FOMC members advocate returning with further tightening later.

Bank of Canada—The Not-Minutes Minutes

The Bank of Canada will deliver its Summary of Deliberations leading up to the decision that was delivered in the June 7th policy statement on Wednesday (1:30pmET). Recall that the BoC hiked by 25bps which sent shockwaves through global markets as the latest evidence that a significant central bank was resuming a tightening stance after the RBA had previously done so. Please go here for a recap of the statement and here for a recap of the next day’s speech and press conference.

The BoC stresses that these are not meeting minutes per se, which is consistent with a different decision-making process at the central bank than, say, the two-day formal FOMC meetings. The BoC’s explanation of its process commences with staff projections and analysis presented to Governing Council about three weeks prior to the decision day. Staff make policy recommendations two weeks later and hence one week before the decision at which point Governing Council goes into blackout. At this point, Governing Council takes over and of course is not bound to delivering what the staff recommend. GC meets several times stretching into the week of the decision at which point the statement is drafted for release.

So, when you hear of the BoC’s Summary of Deliberations—offered at the behest of the IMF’s demands for improved communications relative to peer benchmarks—bear in mind this point that it is not intended to be an account of any particular discussion. Rather, it’s a massaged account of a series of discussions that are generally distilled into an overall account that modestly embellishes the prior understanding of the decision that was offered by the statement and either the MPR and Governor’s press conference, or, for non-MPR meetings, the next day’s Economic Progress Report speech and press conference that is delivered on a rotating schedule subject to availability.

With that context established, I would watch for modest risk that the following issues may be further informed:

- does the GC have a bias toward having to tighten further or was this a one-and-done episode? A case for one-and-done could be the signaling value to markets that were at one point trying to push the BoC toward easing before it was prepared to do so and therefore the BoC felt it necessarily to get markets off its back. The broad communications nevertheless left the door very much open to possible further tightening in data dependent fashion. Markets are fully pricing another 25bps hike in 2023Q3 with much of that priced by the July 12th meeting. Markets are also pricing a solid chance at a further 25bps hike before year-end.

- We’ve heard from Deputy Governor Beaudry that the risks to the BoC’s estimates of the neutral policy rate are skewed higher and the deliberations may expand upon the broader GC’s discussion of this matter. I have to admit that while I agree with Beaudry, it was a bit of curious communications issue to have said this just after staff issued their 2023 update of the estimated neutral rate (here) and concluded that, nope, nothing’s changed in the world, it’s still 2–3% with a 2½% midpoint.

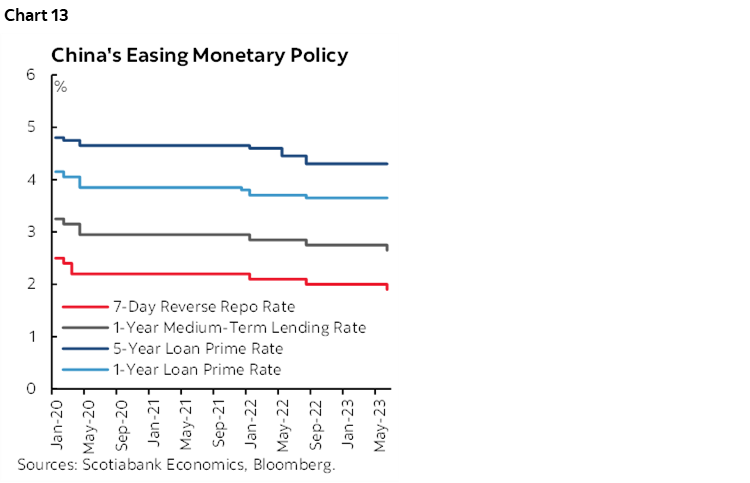

The PBoC’s After Effects

There’s one central bank that has been gradually going in the opposite direction of central banks elsewhere. (chart 13) That is the People’s Bank of China that has long failed to meet its 3% inflation target and presently is addressing downside risks to growth and near-zero inflation through a combination of spreading out rate cuts and reductions to required reserve ratios in order to encourage more bank lending.

After beseeching banks to reduce their deposit rates, following by the PBoC’s actions that cut the 7-day reverse repo rate by 10bps on June 12th and then the 1-year Medium-Term Lending Facility Rate by 10bps two days later, it seems to be a cinch that Chinese banks will be reducing their 1- and possibly 5-year Loan Prime Rates by the same amount to start the week.

Swiss National Bank—Watch the Tails

The SNB is expected to hike by 25bps on Thursday with the tail risk of a 50bps move. The ECB’s 25bps hike may provide some cover to stick with +25bps. So could the challenges around combining UBS and CS. So may the fact that core CPI inflation ebbed to 1.9% y/y from 2.2% the prior month and with May’s reading landing a tick beneath consensus. Nevertheless, the Swiss government’s recent forecast update pointed to how “inflationary pressures remain high internationally and there are pronounced economic risks.”

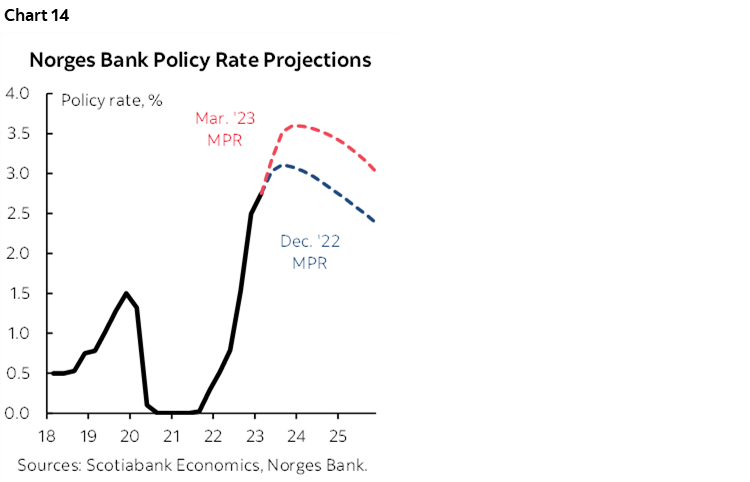

Norges Bank—Sound Familiar by Now?

Rinse, repeat? The same guidance that has been commonplace of late could apply to Norges Bank’s decision on Thursday. By that I mean most expect a 25bps hike, but a substantially minority think there is the risk of a more hawkish surprise with a 50bps hike.

One thing to hang the risk of a 50bps move upon is guidance from Governor Ida Wolden Bache who said “If the krone remains weaker than projected or pressures in the economy persist, a higher policy rate than envisaged earlier may be needed.” Righto, so what’s happened since the last decision on May 4th? The krone initially appreciated to the dollar but has since fallen back to that meeting’s levels. Inflation surprised higher in the early June reading for May with a 0.5% m/m gain (0.3% consensus) that pushed the year-over-year rate up three-tenths to 6.7%. Underlying inflation also surprised higher to 6.7% y/y from 6.3% prior and consensus. Wage growth has also accelerated to 4.4% y/y. So far, that evidence leans toward a bigger move, but what complicates the decision is that the economy has recently disappointed. GDP shrank by 0.4% m/m in April versus consensus at +0.1%. Updated explicit forward guidance will be offered and follows the pattern of upward revisions (chart 14).

Banco de Mexico (Banxico)—Holding Pattern

Banxico is widely expected to leave its overnight rate unchanged at 11.25% on Thursday. The central bank delivered a final 25bps hike on March 30th. It has offered guidance that “…in order to achieve an orderly and sustained convergence of headline inflation to the 3% target, it considers that it will be necessary to maintain the reference rate at its current level for an extended period.” Central bank officials have guided that this should be interpreted to mean holding for at least 2–3 meetings which means at least until the September or October meetings. The risks posed by potential further Fed tightening are mitigated by the fact that the peso has appreciated by about 4% since the last policy decision. Of greater importance may be any revised guidance around timing potential Banxico easing and magnitudes.

Banco Central de Chile (BCCE)—Easing in the Pipeline?

Chile’s central bank is expected to extend its policy rate hold at 11 ¼% where it has been since October. The decision is expected on Monday. Key here may be potential guidance toward timing monetary easing. Our LatAm economists expect a cut as soon as next month.

Banco Central do Brasil (BCB)—A Slow Pivot

Brazil’s central bank has been holding at a Selic Rate of 13.75% since last August. Consensus unanimously expects another hold on Wednesday this week. This is further informed by guidance that was provided in the May statement (here) that said the “Copom emphasizes that, although a less likely scenario, it will not hesitate to resume the tightening cycle if the disinflationary process does not proceed as expected.” Since that meeting, inflation cooled further to under 4% y/y from a peak of 12% last year. This brings inflation closer to the 3 ¼% nearer term inflation target +/- 1 ½%. A significant risk now and going forward concerns guidance around future easing.

Bank Indonesia (BI)—On Target

Bank Indonesia delivered 225bps of tightening starting last year into early this year but has held its 7-day reverse repo rate unchanged at 5.75% since January. Since the prior meeting on May 25th, core inflation ebbed by more than expected to 2.7% y/y with headline also falling more than expected to 4%. That takes inflation closer toward the goal of 2–4%. BI’s communications are likely to be cautious around future easing guidance and partly given uncertainty toward the external environment including the Federal Reserve’s stance over the remainder of this year.

Bangko Sentral ng Pilipinas—Holding On

After holding its overnight borrowing rate at 6.25% in May, the Philippines’ central bank is expected to extend its hold this Thursday.

Recent central bank guidance has said that the “current monetary policy stance is appropriate as inflation is easing”, and that prior moves merit “a prudent pause.” Guidance nevertheless also points to how the central bank “remains ready to resume any monetary actions” and this remark was delivered in the aftermath of the Federal Reserve’s guidance that it may deliver two more hikes this year.

GLOBAL MACRO—A LIGHTER WEEK

US markets will start off shut on Monday for the Juneteenth holiday, giving US market participants plenty of time to prepare for developments cited thus far plus a soft global release calendar.

US macro reports will focus upon housing including NAHB confidence and its model home foot traffic gauge (Monday), housing starts for May (Tuesday) and existing home sales for May (Thursday). Also watch initial claims on Thursday after they jumped somewhat higher over the prior couple of weeks.

The monthly wave of purchasing managers’ indices arrives toward the end of the week. They are useful for informing current-quarter tracking of GDP growth, supply chain developments such as production, hiring plans, order backlogs, new orders, inventories, and price pressures. Australia and Japan lead it off on Thursday followed by the Eurozone, US (S&P, not ISM gauges) and UK measures. Across all of these countries, the composite PMIs have remained above-50 and therefore signaling ongoing economic growth.

Inflation updates will concentrate upon the UK when CPI for May arrives the day before the Bank of England’s decision. Gasoline prices have been on the rise again of late and may buoy expectations for a ½% m/m rise in all-in CPI, but key will be whether the consensus estimate for a 0.5% m/m increase in core CPI that lands the year-over-year rate at 6.8% proves correct as base effects alone would drop this reading down to 6.3%.

UK retail sales will be updated for May the day after the BoE’s decision and they are expected to have a soft tone.

Japan updates CPI inflation for May on Thursday. Since we already know that the fresher Tokyo gauge for May decelerated in year-over-year terms to 3.2% most forecasters have gone with that for their national estimates even though m/m core CPI was up sharply.

Canadian retail sales were probably little changed in April (Wednesday) based upon advance guidance from Statcan.

While the LatAm markets focus will be upon central bank decisions, limited data risk will concentrate upon Mexican retail sales in April (Tuesday) and bi-weekly CPI (Thursday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.