Next Week's Risk Dashboard

- The BoC may sound hawkish this week…

- … and faces three options…

- …including an update of its policy framework

- US nonfarm & wages unlikely to affect the Fed

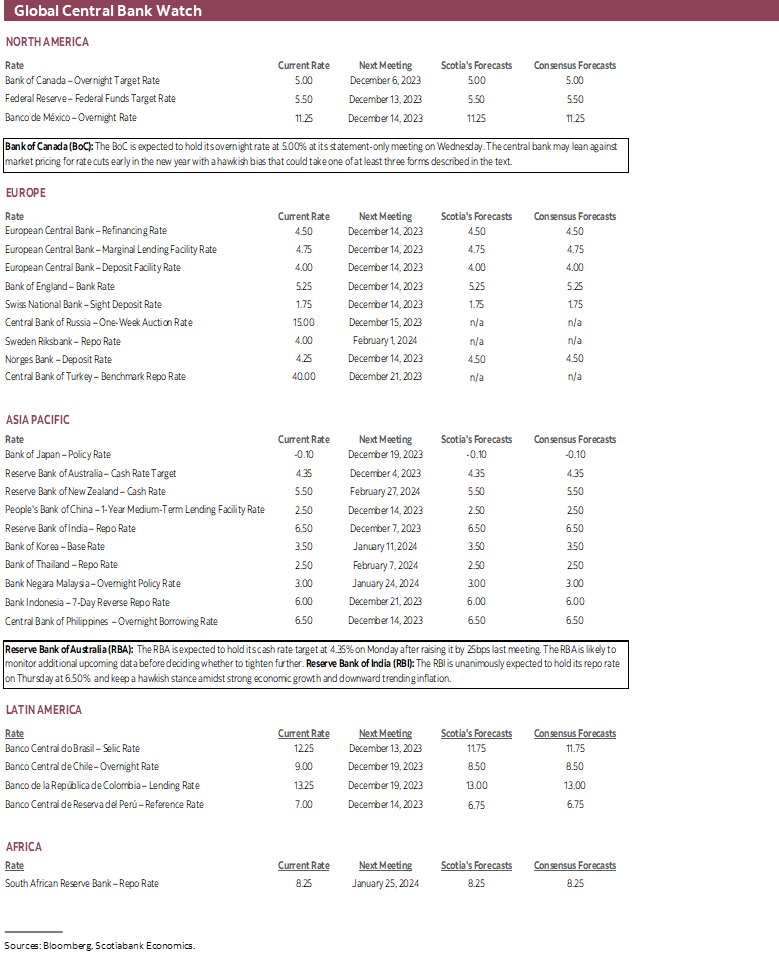

- RBA expected to hold

- RBI is also expected to stand pat

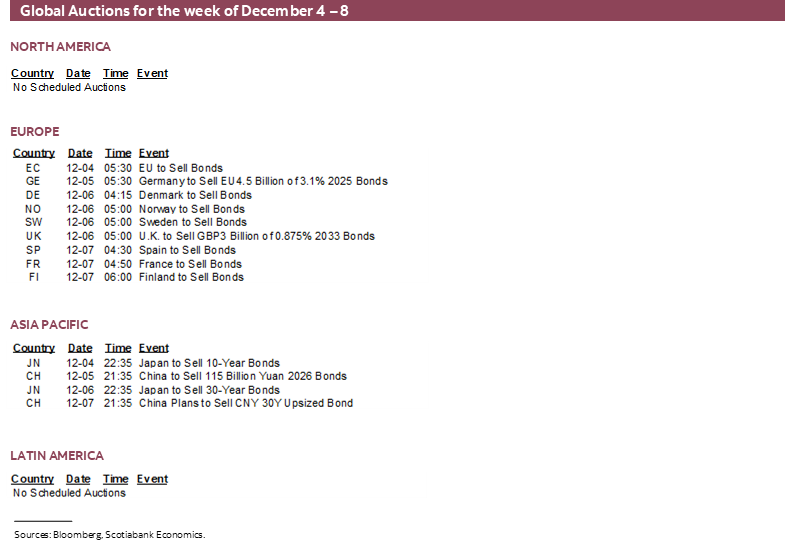

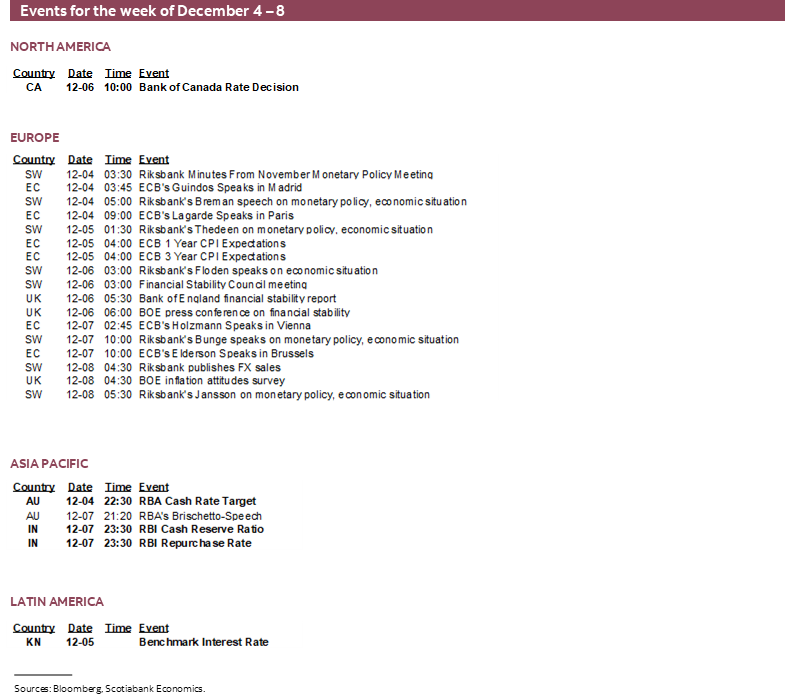

- Global macro indicators

Chart of the Week

While the coming week will offer numerous developments to consider, I’ve chosen a different approach for this issue of the Global Week Ahead that is, well, less global this time.

I think there is such a crowded consensus of opinions across market participants and economists on what the Bank of Canada may do going forward that it’s worth dedicating this issue to a different narrative. While there is a strong case for what follows, the minimum hope is that it at least generates greater diversity of debate and discussion around the risks. I feel strongly that market pricing is on the wrong path and a little less strongly that the BoC is feeling uncomfortable about it and by enough to do something about it.

Other developments will also be noteworthy and I’ll write about them as the week progresses. Indicator forecasts and expectations for a few other central bank decisions are available in the accompanying tables. Friday’s US nonfarm payrolls and wages, decisions by the Reserve Bank of Australia and the Reserve Bank of India, a round of inflation readings mainly focused upon Asia-Pacific and Latin American markets plus inflation surveys from the ECB and BoE will be among the key highlights.

BANK OF CANADA—MARKETS MAY BE CAUGHT OFF GUARD

The BoC delivers a statement-only outcome on Wednesday morning (10amET), but the following day’s speech might be the more insightful part of it. They are likely to come across sounding a little more hawkish and I’ll lay out three possible ways in which they could do so below including the likelihood of each scenario.

The Cost of Doing Nothing

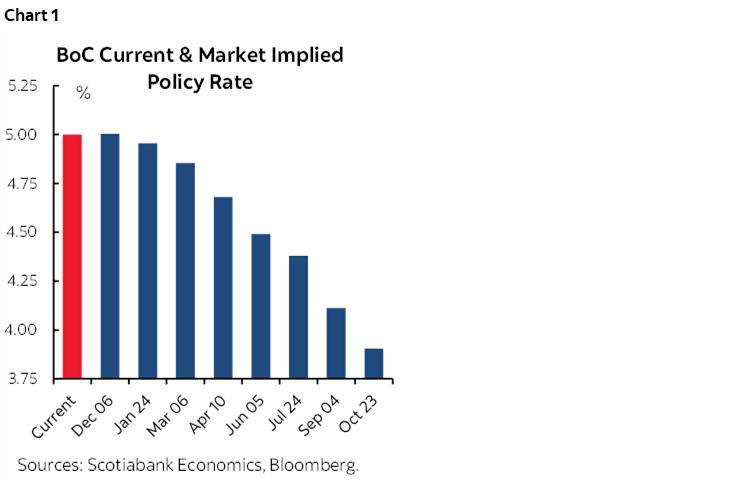

If they choose none of these options, then it’s game on, and the market will continue to push the BoC toward pricing early and aggressive cuts which I think would be a mistake given only very nascent evidence of progress against inflation (here) amid still high inflation risk. Markets are pricing cuts early in the new year (chart 1).

Market pricing is assigning significant probability to a rate cut at the January 24th meeting such that a mere indifferent shrug of the shoulders this week could leave the BoC vulnerable to runaway cut pricing over the ensuing seven long weeks. If they’re wise, they won’t treat this week’s communications as a mere placeholder. They will view it as a seminal moment in determining how and when to ease up and as such are approaching their own Rubicon. Depending upon how they behave this week, the BoC could seal its fate with markets.

It’s Happening Again

Why a hawkish bias? For one thing, the bond market—and hence the mortgage market—has got to be catching their attention again. If it isn’t, then somebody needs to wake them up. They are at risk of repeating what happened earlier this past Spring all over again.

Some time ago, Governing Council had a little more bounce in their step because they thought markets might have been listening to their higher for longer narrative when their October forecasts pushed out achievement of 2% inflation until the back half of 2025 and implicitly guided that they wouldn’t be easing until perhaps late 2024, maybe early 2025 in anticipation of such an achievement. The 5-year Government of Canada bond yield had pushed up to a peak of 4.4% at the start of October. There were other catalysts behind this including external drivers like US Treasury issuance that was overshooting in order to replenish the Treasury’s deposits at the Federal Reserve. Still, they could claim that the higher for longer narrative was being believed and so they didn’t need to hike again even if they exaggerated their role in the outcome.

That’s no longer the case if it was ever due to their efforts in the first place. Mortgage rate cuts are back in vogue now and thanks to the fact that a key driver of fixed term mortgage rate pricing—the five-year GoC yield—is down by almost a percentage point from the peak and back to levels unseen since early last June. This is exactly the scenario I was most worried about in terms of containing pressures on housing affordability and holding inflation risks at bay should the BoC waffle.

The BoC needs to be very careful to avoid doing anything this week that would drive 5s richer yet. We could wind up plumbing the sub-3% depths into the Winter mortgage pre-approvals and Spring housing markets and unleash greater inflationary pressures through another powerful housing boom with spillover effects on related consumption. I can just imagine the phone call from the PM’s office inquiring about what the BoC is doing by overstimulating housing demand while they are trying to improve housing supply through limited measures.

That period also coincides with the Winter budget season across federal and provincial governments and believe me, in this country, they need no reasons whatsoever to go out an borrow to spend more while the cost would be even greater fiscal pressures upon inflation. The BoC needs to lean against this scenario absent any compelling evidence whatsoever that they’ve licked underlying inflation.

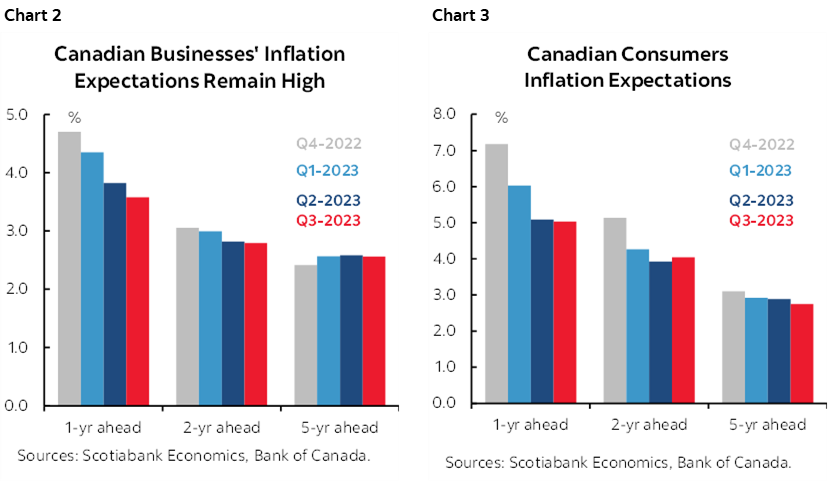

The other drivers of a hawkish bias include still high inflation expectations for years to come in their survey measures (charts 2, 3), and a much better fundamentals picture than portrayed by some of my more depressing competitors. As argued here, the job market remains hot and while there are signs that balance is being restored, the country is cementing years of wage gains through collective bargaining and spillover effects at rates far above the BoC’s 2% inflation target. That is going to make it difficult to contain inflationary pressures especially as productivity has been tumbling. The economy is not in recession (here) especially when we do a little more of our homework by digging beneath the headlines. Immigration remains excessive relative to housing availability and infrastructure and so housing-related inflation is soaring. There are reasons for falling per capita real GDP that mitigate some of the more alarmist coverage of the topic as laid out in the aforementioned jobs note. Fiscal stimulus is ongoing. CAD is undervalued and the terms of trade remain favourable.

So what might they do this week?

HIKE?

A low, but non-zero probability is that they decide to hike in order to lean against this easing of financial conditions. That would shock markets, but they wouldn’t so much care if they felt it was the right thing to do. The BoC does have a tendency to surprise markets as we’ve seen several times during the cycle. It’s an aloof organization that couldn’t care less if traders wind up drowning their sorrows at the local watering hole.

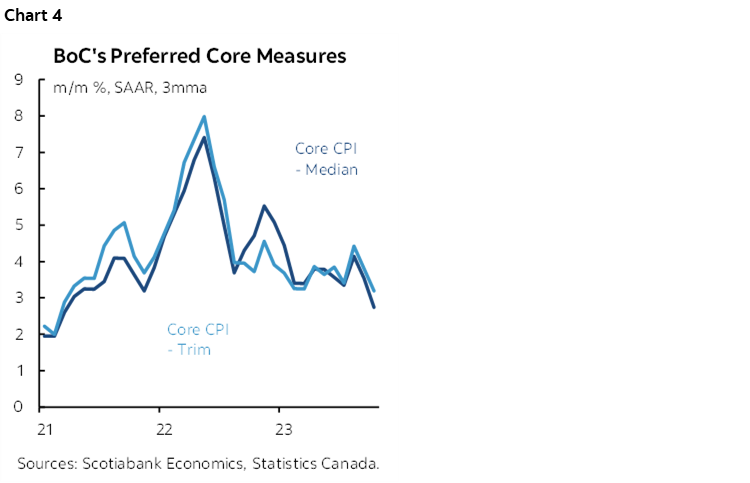

The question is whether Governor Macklem has the wherewithal to do so especially after a very recent soft patch on trimmed mean and weighted median CPI inflation despite still hot trending core measures (chart 4). He recently guided that the policy rate might be restrictive enough, but they were not sure and were prepared to tighten again if needed. He’s also getting a lot of political flak and while it’s a generally, mostly, kind of independent central bank, I don’t view Macklem as John Crow redux.

Strengthen a Hike Bias?

Another option would be to tee up a willingness to hike again with a little stronger language. That approach buys a bit more time to assess conditions, get through the holiday season, and to evaluate more data and issue another forecast round in January. It could spark some second thoughts in markets and give a shove back to rate cut pricing. This approach is higher probability than an actual rate hike.

Update the Framework

A third approach—and my favourite one—is that the BoC could rely upon the speech the day after this decision in order to indirectly guide that markets are getting too aggressive in pricing rate cuts as soon as the March meeting. They could do this by updating their framework of understanding regarding the order of operations in terms of adjusting their balance sheet and policy rate tools together.

Enter Deputy Governor Toni Gravelle’s speech on Thursday with remarks due by 12:35pmET and a press conference to follow. Gravelle heads the BoC’s Financial Markets Department and the Banking and Payments Department. Macklem speaks the following week in the Governor’s usual pre-holiday appearance. This tag team approach has been used before to inform market thinking on the policy framework and its expected evolution and it could well be the plan once again. While there are no guarantees they will do this, if the BoC wants to update market thinking on the order of operations and the mechanics of monetary policy actions, then Gravelle has been the one they’ve sent out to do so in the past which then gets reinforced by the boss.

At issue are two things. One is to possibly refresh their guidance on how long to continue balance sheet shrinkage. Second—and related to the first one—is how the BoC views the interplay between balance sheet adjustments and changes to the policy rate which could be insightful to guiding the timing of rate cuts relative to market expectations.

Whereas Federal Reserve officials and ex-officials divorce the two by saying they could well cut before stopping balance sheet shrinkage, I think the BoC chooses to be much more methodical in its framework of thinking. At times, they’ve seemed to be rigidly methodical to a fault. The optics of cutting while they are still heaping maturing bonds back into the market and tightening conditions through that mechanism might be too awkward for them. It’s like pushing and pulling at the same time.

Recall that the BoC felt a need to begin tightening balance sheet policies before hiking coming into the start of the tightening cycle. Ending balance sheet tightening before cutting would be a perfectly symmetrical approach this time.

As a refresher, the BoC was among the first to step away from quantitative easing in December 2021 when they tapered bond purchases, albeit for technical funding market reasons. They continued to taper at each MPR meeting until shutting down purchases one year later and thus ending quantitative easing. The BoC only continued to reinvest maturing bond holdings for a few months before guiding on March 3rd that they were moving toward ending reinvestment (here) before doing so one month later when they embraced full QT with no reinvestment of maturing bonds (here) at which point they hiked by 50bps. Note the interconnectedness of their tools.

They probably need to update their balance sheet plans. Gravelle laid out the framework back on March 29th this year (here). At that time, he said they would continue to allow full 100% roll-off of maturing holdings of Government of Canada bonds through to late 2024 or early 2025. At that point, the concomitant guidance for the magnitude of liquidity withdrawal from the banking system was to get settlement balances—or reserves—down to between C$20 billion and $60B, or 1–2% of nominal GDP.

Gravelle also, however, noted that this was a target that would be informed by market developments. I felt at the time that this sounded very aggressive and in stark contrast to the Fed’s goal of reserves equal to 10–12% of NGDP. You could argue that reserves can be leaner in Canada’s banking system that is inherently more stable than the US system especially across regional banks that frequently blow up. You could, by contrast, also argue that at turning points in risk appetite and market volatility Canada tends to get hurt more and so that would counsel having high liquidity in the banking system.

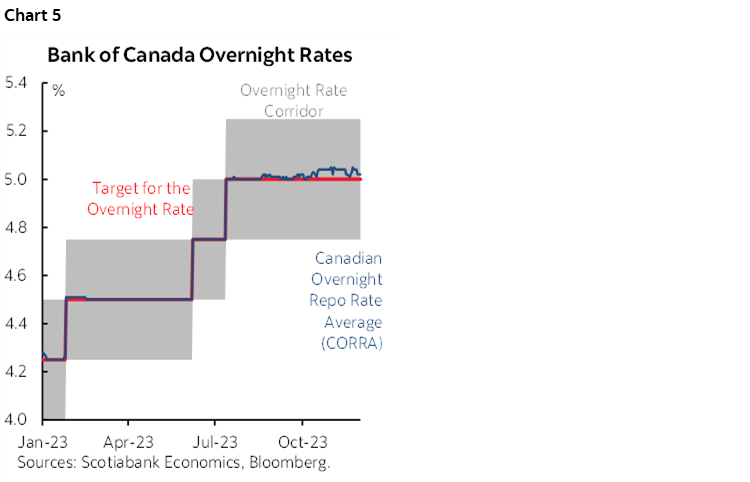

Apart from the theoretical arguments, one such measure of how markets have adapted to this plan is starting to flash red. The Canadian Overnight Repo Rate Average (CORRA) has been slightly above the BoC’s overnight rate since late Summer (chart 5). Not alarmingly so, but it is providing a market signal that the BoC is closer to the point of optimal reserves than it may have initially guided. The BoC does not want to court funding pressures that drive the CORRA spread over the overnight rate higher as that could be very destabilizing to funding markets.

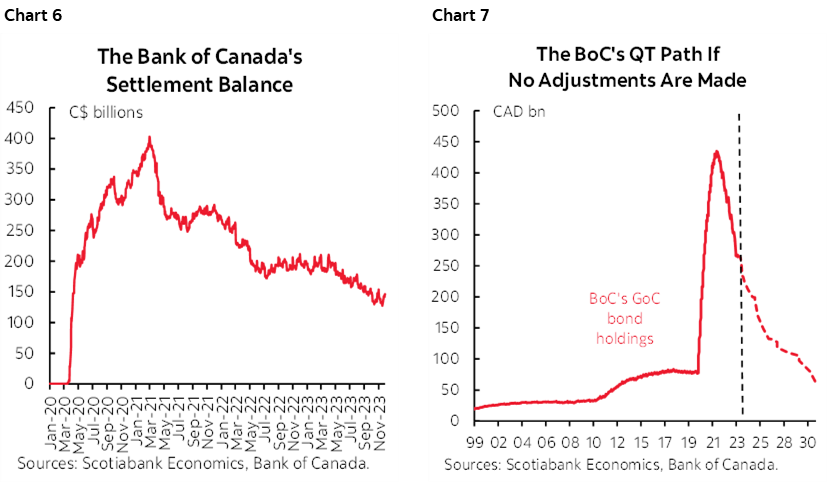

Gravelle may indicate that the market signals are suggesting they went too low with their estimates of optimal reserves. At just under $150 billion, reserves are well down from the peak of $400 billion (chart 6), but rapidly shrinking. At the present 100% roll-off pace for QT, the BoC’s bond holdings would drop another $40B+ within six months from now (chart 7) and push reserves closer toward $100B.

One scenario could have the BoC updating guidance that it may have to end QT earlier than previously thought and leave it at that. Another scenario may be to provide more explicit and earlier guidance on when it thinks it may end QT. It could be 6+ months earlier than initially thought.

Depending upon how they play this, the end of QT could coincide with beginning rate cuts, or doing so shortly after ending QT as the reverse analog to what they did when they began to tighten monetary policy. The advantage to this approach is that the BoC could declare that it wishes to see how markets respond to ending QT and to evaluate further data in the meantime before deciding when to cut. I think markets would respect such an approach and it would reassert the BoC’s primacy over markets if it feels there is a compelling reason to do so.

At the same time, the BoC’s January MPR forecasts will update the other key framework which is the BoC’s beloved output gap and inflation forecasting framework. They put too much stock in it in my opinion but bringing forward rate cuts to mid-2024 could require bringing forward the sustainable achievement of 2% inflation from 2025H2. To cut earlier than mid-2024 would have to be driven by high conviction that the output gap will achieve 2% inflation probably by early 2025 or late 2024 which would fan possible cuts by Springtime next year. I think that’s unlikely, and the market effects are uncertain. Signalling a sudden rush to end QT and begin cuts as soon as 3–4 months from now could be taken as a negative confidence signal in the outlook by the BoC and do more damage than good.

It's especially unlikely for anyone who knows anything about seasonal influences in Canada. Cutting into March/April would light up the housing market, which was something former Governor Poloz was far too eager to do and unabashedly so. I don’t view Macklem as having the same willingness when other policy measures are trying to improve housing affordability and given today’s very different inflation backdrop and risks going forward.

I would rather the BoC set a framework that makes it clear what the order of operations and timing will be such that they avoid prematurely easing. Cutting too early could thwart chances at bigger rate cuts later if they wind up reigniting housing imbalances and broader inflationary pressures. Patience could pay more handsomely by waiting until they have conviction to deliver bigger and more durable cuts later.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.