- Risky Road Ahead: Recent stronger U.S. economic data have slightly lifted our expectations for both the U.S. and Canadian economies, but the outlook is subject to multi-dimensional risks that have intensified in the last few weeks. Risks related to geopolitical tensions, fiscal policy, monetary policy independence, and trade policy are making forecasting particularly challenging.

- Growth Diverges: Assuming none of these risks materialize in any meaningful way, the broader trend remains one of slowing U.S. growth over the forecast. Canada, in contrast, should see growth accelerate in 2027. The U.S. should remain in excess demand while the excess supply in Canada should fade (chart 1).

- Stubborn U.S. inflation: Tariffs effects and persistent excess demand should continue to exert some pressure on inflation in the U.S. Rising costs and trade policies are still important risks to our profile.

- Policy Paths Split: The Federal Reserve is expected to deliver three additional rate cuts this year, with mounting political pressure and an apparent near-term bias towards shoring up the labour market and a willingness to tolerate modest deviations of inflation. We forecast the Bank of Canada to hold its policy rate steady in the near future at least until CUSMA is renegotiated, withdrawing some stimulus towards the end of the year as growth improves and inflation gets closer to target.

Recent U.S. data indicate that the economy has shown greater resilience than anticipated. Robust equity markets and reduced drag from trade policy uncertainty have supported consumer spending, which has remained strong over the past few quarters.

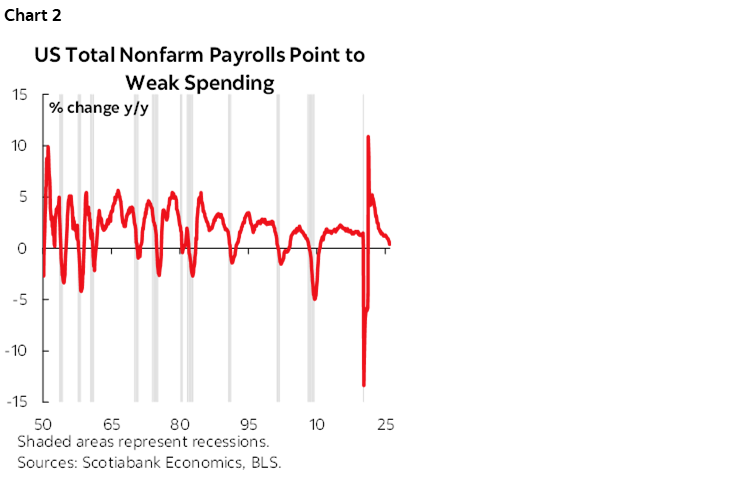

However, this resilience is unlikely to fully offset a broader slowdown in momentum. The cumulative impact of elevated interest rates, a softening labour market, and persistent trade policy uncertainty is expected to weigh on activity. Household spending, in particular, is expected to slow significantly in the coming year. While consumers have been remarkably resilient so far, spending growth should moderate and align more closely with labour market weakness given the drop in the personal savings rate (chart 2). That said, lower interest rates should provide some partial support, especially in 2027. Business investment has been a key driver of growth recently, fueled by strong tech-related outlays. We expect this to moderate in 2026 as firms adopt a more cautious stance amid slowing demand. Finally, against the backdrop of tariffs and trade policy uncertainty, imports are likely to decline in 2026, providing some offset to weaker domestic demand growth in measured output.

Overall, we project U.S. real GDP growth to ease somewhat from about 2.1% in 2025 to roughly 1.9% in 2026 and recover slightly in 2027 at 2%.

Slowing growth, however, is not sufficient to bring U.S. inflation down to 2%, as the economy is expected to remain in a state of excess demand throughout the forecast period. We project core inflation to hover in the mid-2% range through 2026 and reach about 2.3% in 2027. Tariff-related cost pressures remain in the pipeline, compounded by lingering excess demand in part reflecting the too-accommodative stance of U.S. monetary policy. Meanwhile, underlying domestic price growth, particularly in services, continues to be sticky, driven by rising wages and other input costs. Importantly, as the economy decelerates and uncertainty fades, these inflationary pressures should gradually ease.

A key uncertainty for the growth and inflation outlook relates to productivity. A sharp and sustained increase in productivity could raise the economy’s non-inflationary growth. While this should be accompanied by an increase in aggregate demand, it could put downward pressure on inflation while also leading to stronger growth.

Against this backdrop, we expect the Federal Reserve to continue its gradual policy easing, delivering three additional rate cuts this year and bringing the federal funds rate to around 3%. This would place the policy rate below what is prescribed by economic conditions, reflecting policymakers’ willingness to tolerate slightly higher inflation in the near-term in exchange for supporting growth and the labour market. This additional accommodation keeps the economy in excess demand over the forecast. Political pressure on the Fed could also influence decision-making, resulting in lower rates. Indeed, our models indicate that the policy rate should be higher than our forecast, but we incorporate the Fed’s dovish bias, erring on the side of more stimulus.

The U.S. administration is making forecasting extremely challenging these days and several elements could significantly derail this outlook. These include but are not limited to:

- Supreme Court decision on tariffs—striking down tariffs would be a positive for near-term growth, but could bring further uncertainty if the administration pursues alternative channels to re-impose trade restrictions.

- Mounting political pressure on the Fed—while we already account for this by way of additional easing, further escalations could lead to an even lower fed fund rate than currently assumed and risk de-anchoring inflation expectations. Market pricing of recent development has been largely muted, but this could be fragile to signs of renewed inflation pressures and economic stress.

- Geopolitical risks—while here too market responses have been limited, the risk is that recent events may signal a weakening of historical patterns of escalation and containment, increasing the likelihood of potentially destabilizing outcomes.

- Equity market (two-sided risk)—markets could continue to look through geopolitical and policy risks, and the boom could continue longer than we expect. Alternatively, a materialization of these risks or a reassessment of underlying fundamentals could force a rapid repricing or correction (see our earlier note on this scenario).

- Fiscal policy—proposed increases in transfers and defense spending remain unclear with respect to timing and scale, but a significant increase in spending has potential to significantly boost growth and may impact the Fed’s future decisions. With both spending plans underpinned by the promise of tariff revenues, implementation inconsistency arises considering the above-mentioned legal challenges and other trade-policy uncertainty.

CANADA

In Canada, the outlook is improving incrementally, partly thanks to the economic resilience south of the border. A stronger U.S. outlook and a reduction in global trade uncertainty will provide a welcome boost to Canada’s export-oriented sectors and business sentiment. However, CUSMA remains a significant wildcard for this forecast. Our base case assumes an orderly renegotiation with only minor changes that should have minimal impact on the economic outlook.

We now expect annual Canadian real GDP growth to stay roughly flat in 2026—averaging 1.5%—though this annual average is pulled down by household spending in 2025Q4, masking a gradual strengthening in most quarters. Growth should accelerate to 2% in 2027, supported in particular by the fading effect of trade tensions on growth and past effects of policy rate cuts. Ongoing government spending and investment initiatives at home are also expected to lend support to growth. Even so, Canada’s growth will remain moderate by historical standards, still restrained by structural factors such as weak productivity growth and low population growth.

Canadian inflation should continue to trend downward gradually. With the economy operating below full capacity in recent quarters, excess supply is exerting some negative pressure on prices. We expect headline inflation to ease toward the 2% midpoint of the Bank of Canada’s target band over the course of 2026. However, much like in the U.S., core inflation in Canada is proving sticky, lingering in the upper half of the BoC’s target range. Rising input costs mean that inflation risks haven’t completely vanished, even as demand cools.

We maintain our view that the Bank of Canada will stay on hold in the near-term. The BoC is unlikely to move until CUSMA renegotiations are settled and the policy backdrop clears. Assuming an orderly outcome as per our base case, the BoC should be finished with its rate cutting cycle and the next move will be toward normalization. The BoC delivered considerable easing in 2025, and we interpret some of the stimulus as insurance against a sharper slowdown. Now, with growth holding up and inflation remaining sticky, we think further rate cuts should be off the table. Consistent with our previous guidance, we expect the next move will be a rate hike in the second half of 2026, bringing the policy rate closer to its neutral stance. By that time, we anticipate the economy will be on firmer footing which will allow the BoC to start to withdraw some stimulus.

Canada is exposed to many of the same uncertainties surrounding the U.S. outlook. In particular, the upcoming CUSMA renegotiations could have a significant impact, as failure to reach an agreement would sharply raise the low effective tariff rate that Canada has benefited from so far.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.