- We continue to believe a mild recession is likely in Canada beginning in Q2 though economic indicators remain reasonably positive. We forecast only a modest increase in unemployment this year given the strength observed in labour markets so far this year and clear indications that labour shortages remain a major concern for Canadian employers.

- Core measures of inflation rose on a monthly basis in April leading to an upward revision to our core inflation forecast despite lower oil prices. We now expect core measures of inflation to average 3.9% this year. Our predictions for total inflation are largely unchanged and have been stable over the last several forecasts. That being said, our inflation forecasts have been higher than the Bank of Canada’s for quite some time.

- The rise in inflation and perhaps more importantly the surge in housing market activity and still robust employment markets suggest that risks around the Bank of Canada’s inflation outlook are tilted to the upside, as we have long argued. With inflation on a gradual downward path so far this year, the risks to the inflation outlook were manageable at current policy rate settings.

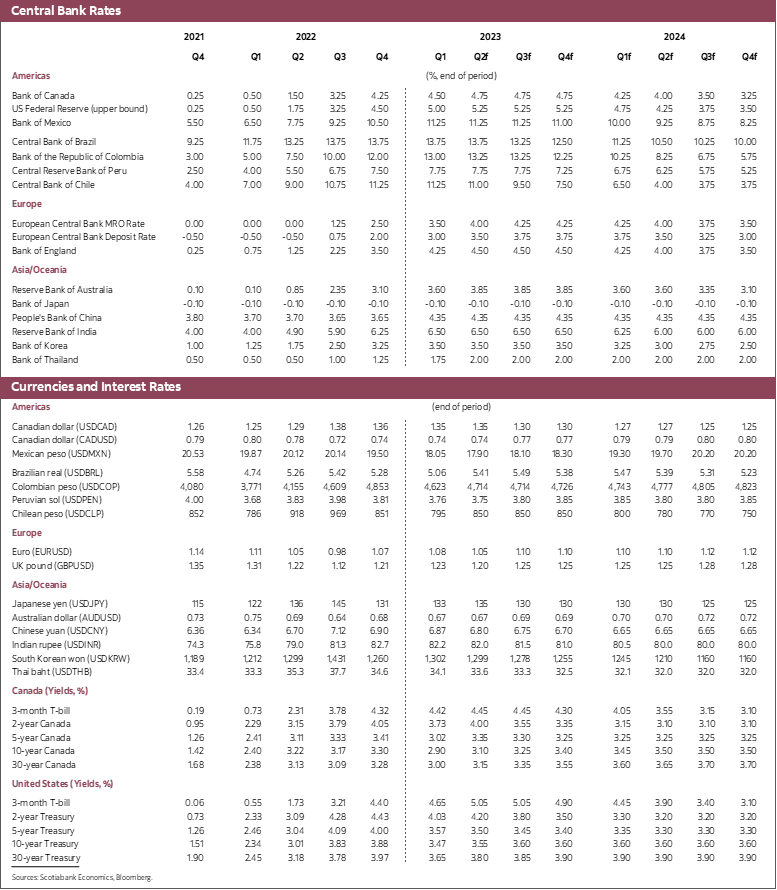

- With core inflation rising (admittedly for one month only), we believe the Bank of Canada no longer has the luxury to wait to see how the balance of inflation risks evolves in coming months. As a result, we now think a 25 basis points move is required at the June meeting. Governor Macklem should leave the door clearly open to additional moves should those be required. We continue to expect the policy rate will be cut early next year and see little chance of a cut this year.

- That being said, this move is best seen as insurance against inflation. Our model does not indicate a need for higher rates despite the April inflation shock and other developments.

We remain of the view that the country will experience a mild recession in the second and third quarters though that slowdown, if it occurs, is best characterized as a stall in economic activity. There are some indications that economic activity is moderating though the evidence remains scant. Statistics Canada notes that it estimates real economic activity fell in March, potentially setting the quarter up for a decline. Associated with that are indications that real-time local business conditions moderated in April providing additional evidence of a softening in demand. Moreover, oil prices are significantly lower than expected, with consequent impacts on the economy and inflation. The wildfires in Alberta will be another drag in the second quarter but that is likely to be temporary and reversed once the situation returns to normal. These developments contrast with a sharp improvement in home sales in April despite very low listings, and a still strong job market which saw reasonably robust hours growth. Moreover, population growth is at a 50-year high based on the population estimates in the Labour Force Survey, building on the historic population growth observed last year. On balance, this suggests that economic activity is likely to fall only moderately in the second quarter, following the strong start to the year.

Inflation remains too high, and the April inflation results show that core measures of inflation are accelerating from what were still uncomfortably elevated levels. One month definitely does not make a trend and it is too early to be definitive that this represents a worrisome shift in inflation dynamics. Our model still points to a gradual decline in inflation over the remainder of the year, though the April surprise is leading us to raise our inflation forecast for core inflation to 3.9% for 2023 and 2.3% next year. The April reading further reinforces asymmetric risks around the Bank of Canada’s inflation profile, however. The consequence of inflation overshoots relative to forecasts or Bank of Canada expectations are much more important than negative surprises to inflation (which would be very welcome). In this sense, the April results are worrisome given that the BoC forecast for inflation has been meaningfully below our own for a few quarters now suggesting they may need to raise their own forecasts appreciably.

The April inflation print does not in and of itself warrant higher policy rates. Our model, which has done a great job of forecasting inflation and interest rates, suggests that rates should remain at their current level. If the economy evolves as we are forecasting, there is no need for additional rate hikes. That being said, the consequences of higher or lower inflation are asymmetric. The Bank of Canada cannot tolerate a widening divergence of inflation from its 2% target.

Recent data suggest an accumulation of risks to the BoC’s inflation outlook. These obviously include the April inflation readings, but they follow other impactful data:

- The April housing data is a problem for the Bank of Canada. The housing market was a drag on the economy for much of last year, as one would expect given the evolution of monetary policy. A reversal in the market now, triggered by policy rate stability, a decline in longer-term borrowing costs post-SVB and an evident pent-up demand for homes mean that home prices are once again on the rise and that housing is likely to boost growth going forward. We have reflected that in our current forecast, but the BoC could dampen that activity with marginally higher rates.

- The job market remains remarkably robust. There are well documented lags between economic activity and labour market outcomes, but the strength of employment this year is astounding. Canadian employers have already hired nearly 250k workers so far this year and the most recent CFIB Business Barometer continues to show that small and medium-sized business believe labour shortages are the most critical barriers to higher sales or production. Nearly a quarter of firms expected to increase hiring in April, with only 14% expecting to shed labour—the lowest level since May 2022.

- And as Derek Holt has noted, there are a number of other potential upside risks to the inflation outlook that merit consideration by the BoC.

There are of course downside material risks to inflation. The most important are views surrounding potential output. Record population growth could suggest that potential output is currently underestimated, even though productivity is actually declining. Lower oil prices could also feed into non-core measures of inflation in a more meaningful way as the year progresses. And while employment growth has surpassed expectations thus far there is a possibility for a larger-than-expected adjustment to the downside as the economy slows. Our forecast assumes a historically modest increase in the unemployment rate this year, rising from its current level of 5.0% to 5.7% by year-end. In addition, it is still too early to be confident that the banking issues in the US will remain as benign as they have been thus far. Some retrenchment in credit is still likely.

We think the BoC needs to weigh potential upside risks to the inflation outlook more heavily than has been warranted since the pause was announced. This suggests to us that a more cautious approach to inflation management is required, and that an additional 25 basis points move is required at the June meeting. Again, we reiterate that our current forecast for the economy and inflation does not in and of itself suggest another increase is necessary. But mounting upside risks to the inflation outlook, many of which are already integrated into our upwardly revised inflation forecasts, suggest a further shot across the economic bow is required by the BoC. The BoC no longer has the luxury to wait to see whether or not these risks materialize given the outsized costs of a further deviation from target. The question for Governor Macklem and his colleagues is not whether or not they will raise their inflation forecasts, but rather by how much they will do so. We continue to believe that the BoC will not cut its policy rate this year and that it will undertake a gradual series of cuts in early 2024.

We foresee no change to our US policy rate views at present. We remain of the opinion that the Federal Funds target rate is at its terminal rate, though risks to that are evidently tilted to the upside. We continue to anticipate a modest US recession this year but have pushed that out to Q3 and Q4 relative to our previous view of a Q2/Q3 retrenchment. Economic data do not seem to suggest a fall in GDP is in order for Q2 at the moment, though there is evidence of a slowdown in consumer spending in recent weeks. The delayed recession, combined with a better start to the year than expected implies a slightly stronger 2023 than previously forecast and a weaker 2024. We assume that the US debt ceiling issue will be resolved and do not incorporate any impacts of a breakdown in talks into our forecast. A US default resulting from an inability to come to an agreement would have dramatic consequences and present a severe downside risk to the US and global outlook. As elsewhere, we expect US inflation to decline gradually through the year but have revised the profile upwards owing to its recent stickiness. While we do not believe another rate hike is necessary, we can not see the Fed cutting rates this year. This is a sharp contrast to current market pricing.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.