The effects of the vicious third wave of the pandemic on the economy are being overtaken by continued resilience and positive surprises to indicators.

Risks remain tilted to the upside, owing largely to President Biden’s attempts to raise government spending even further.

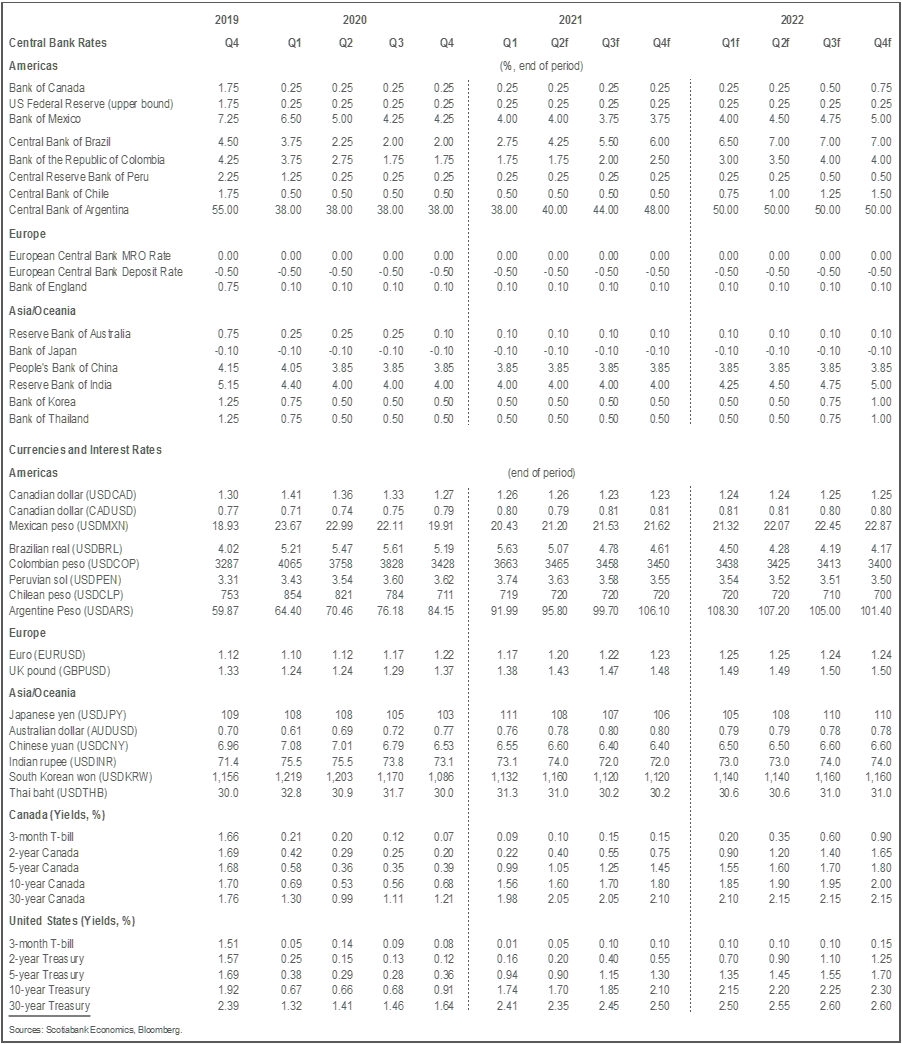

The Bank of Canada is likely to raise interest rates in 2022-Q3, well ahead of the Fed owing to higher inflation and markedly better labour market outcomes in Canada. The Fed is expected to move in 2023-Q1. Both central banks will raise interest rates by 25 bps a quarter once they start hiking.

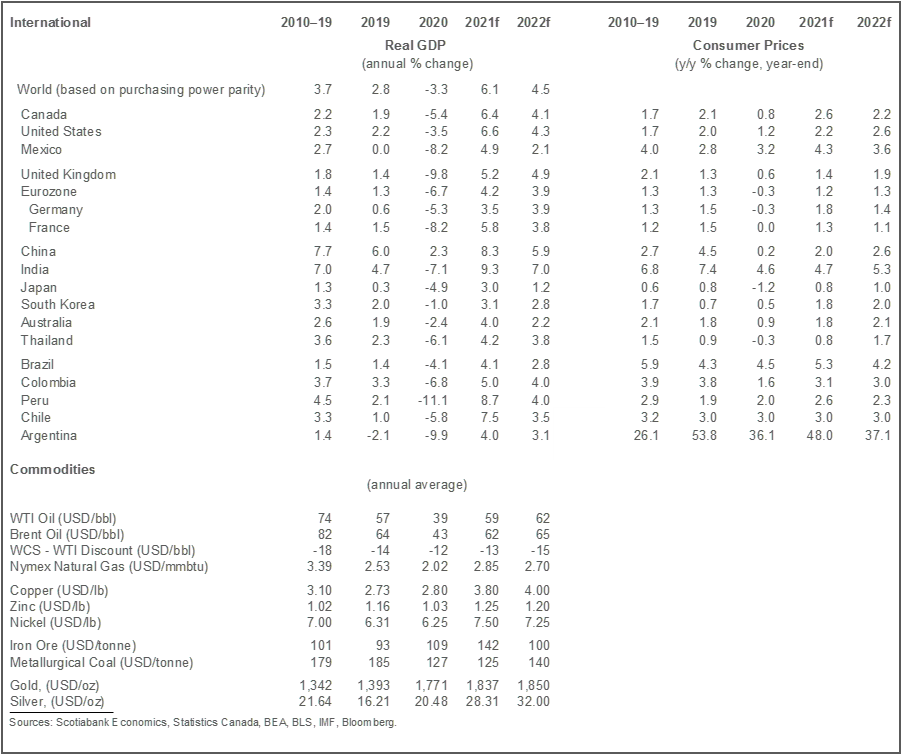

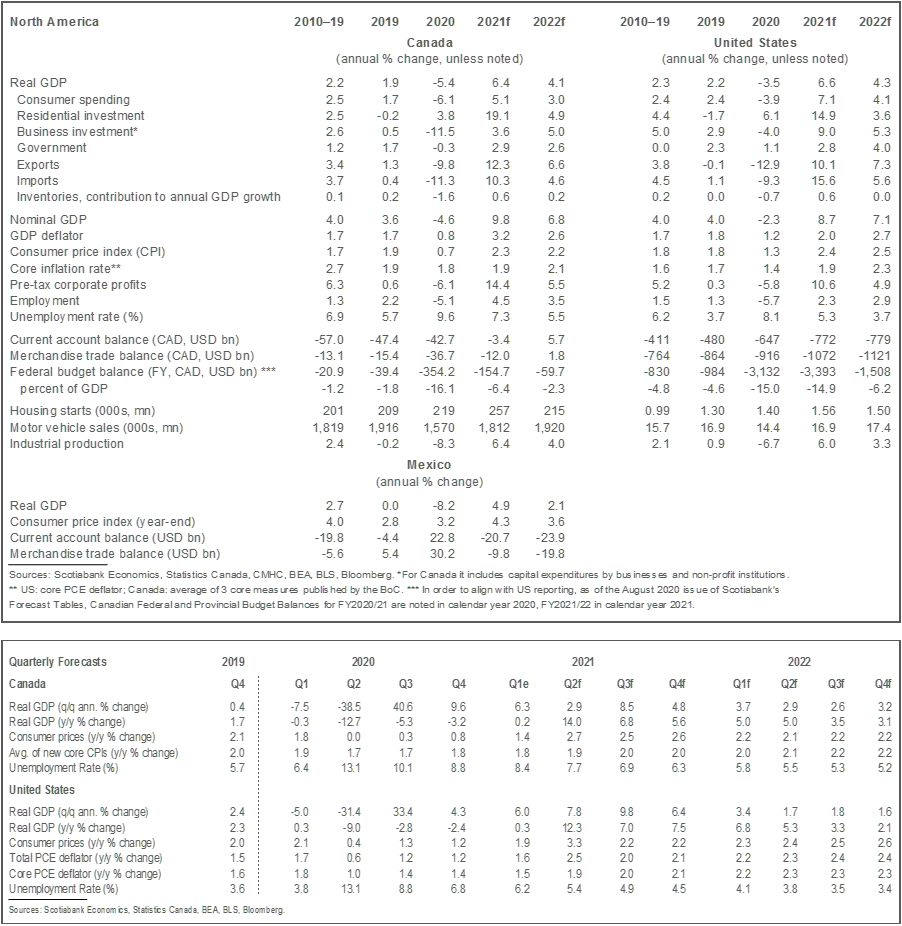

Despite very worrisome developments on the pandemic front in recent weeks in many countries, incoming economic data continue to suggest outcomes are surpassing expectations. This is particularly true in the United States and Canada. In the former for example, March retail sales were exceptionally strong on account of stimulus cheques. In Canada, the March labour market readings were very robust with employment now only 1.5% off pre-pandemic levels, and housing construction particularly strong. There is no doubt, however, that tightened mobility restrictions will have an impact on countries that have imposed them.

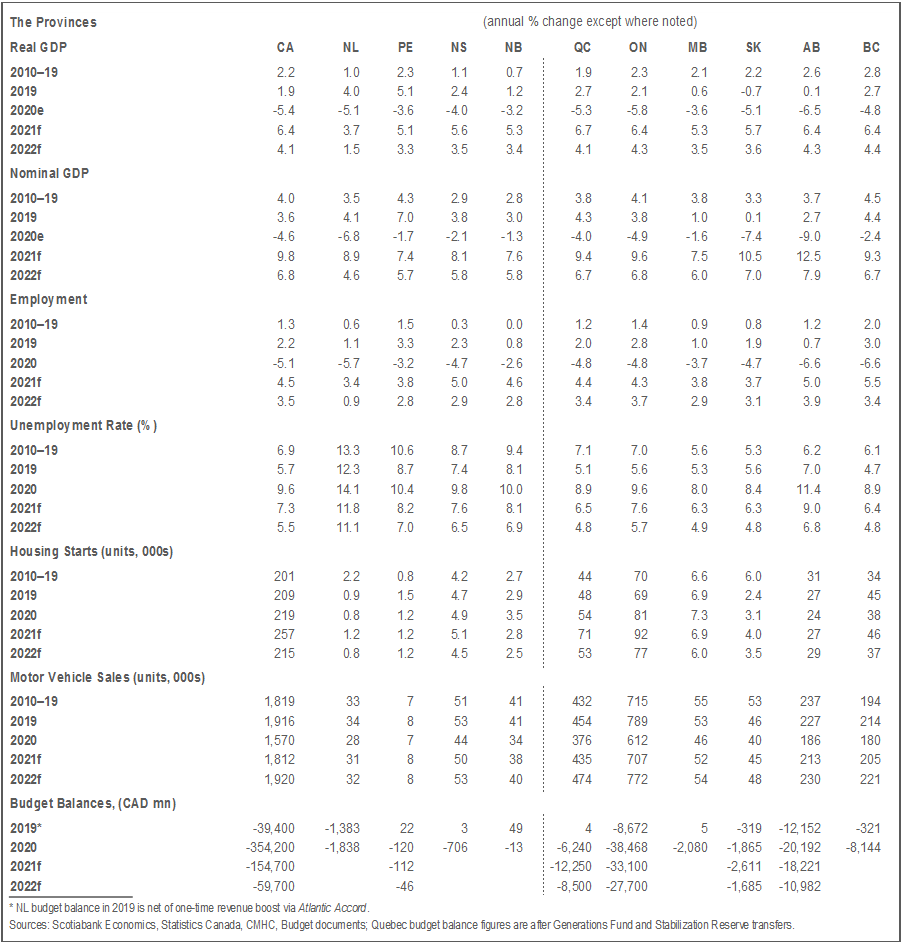

In Canada, the strength of incoming data, solid growth prospects in the US, and higher commodity prices are leading us to raise our forecast for 2021 to 6.4% (from 6.2%) and to 4.1% in 2022 (from 4.0%). This upward revision is tempered by the economic impacts of the third COVID wave, which we now believe will shave 3 percentage points from 2021-Q2 growth, leaving growth at 2.9% in that quarter. Canadian output is likely to return to pre-COVID levels during the summer. The speed of this recovery is nothing short of exceptional given that many forecasters (including us) had earlier called for an early- to mid-2022 return to pre-pandemic activity. The K-shaped recovery is still very much at play as the pandemic continues to weigh on COVID-affected sectors of the economy, while almost every other sector is doing substantially better.

As in Canada, the US economy continues to recover strongly. We have raised our forecast to 6.6% (from 6.3%) in 2021 but reduced it slightly to 4.3% (from 4.4%) in 2022. Our revision mostly reflects the strength of incoming data though we are also currently including about half of President Biden’s infrastructure plan. As a result, the risks to our forecast are tilted to the upside given the likelihood that significantly more fiscal spending occurs in the next few years (more infrastructure and other planned announcements).

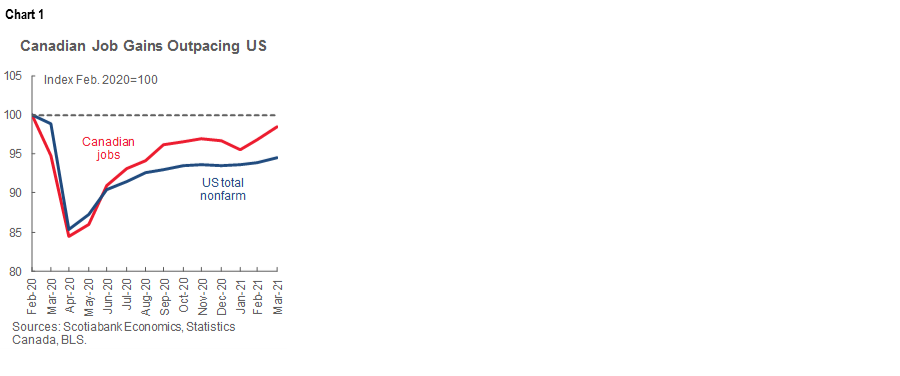

Though growth outcomes are expected to be roughly similar in both countries this year, labour market dynamics are significantly better in Canada (chart 1). US employment remains 5.5% below pre-pandemic levels while Canada is only 1.5% away. The participation rate is only 0.3 percentage points lower in Canada than it was in February 2020, while it is 1.8 percentage points lower in the US. The labour force is already above pre-pandemic levels in Canada but remains over two percentage points below in the US.

These differential labour market outcomes matter from a monetary policy perspective. While core inflation measures are close to the Bank of Canada’s target, core PCE inflation in the US is further away. For the Fed, the dual mandate means they need to incorporate labour market under-performance in their policy stance as well. As a result, we believe the BoC will raise rates well ahead of the Fed, as early as 2022-Q3. We expect the Fed will need to raise rates early in 2023, even though that timeline is quite accelerated relative to current communications from Fed officials. We do not believe that a later tightening by the Fed will pose a challenge for the BoC.

As noted above, risks to the forecast appear tilted to the upside given the likelihood of further fiscal measures in the US. This is despite a vicious phase of the pandemic and tighter-than-expected containment measures in many countries. From an economic perspective, it has been very reassuring to observe the economy’s resilience in the face of the virus’ evolution despite the very heavy human cost of the pandemic. We anticipate this divergence in economic and public health outcomes will last.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.