- North American growth is strongly outperforming expectations so far this year. The resilience theme carries on.

- We now expect the US Federal Reserve will only cut rates by 50 basis points this year, beginning in September given the momentum seen in the US economy and worrisome inflation developments.

- We continue to believe the Bank of Canada should wait until the third quarter, at least, before it begins to lower its policy rates. While inflation is lower than expected, growth is much stronger than forecast, in part because of government fiscal plans, but also because household spending continues to be more resilient than expected.

- We see no benefit to rush into a rate cut at the next meeting in Canada and believe patience will lead to a better outcome for Canadians, even if it means the interest rate pain lasts a bit longer.

Central banks are approaching the policy crossroads. At some point this year, it seems likely that most advanced economies will shift from the tightening path they had been on and maintaining to an easing path. With inflation slowing in many parts of the world, this is a relatively straightforward process for central banks. Not so in North America. Substantial growth surprises have led to large upward revisions to growth in Canada over the last several months. In the US, this has also come with a series of positive surprises to inflation, while the opposite has been seen in Canada. This has led to a marked shift in tone by central bankers and pricing of policy actions by markets. Chairman Powell has made it very clear that the Federal Reserve is in no rush to cut interest rates given the strength of the economy and inflation. Governor Macklem, on the other hand, has emphasized the slowdown in Canadian inflation and has been unusually candid about a June cut being in the “realm of possibility”. As we’ll explain below, we remain comfortable with our view that the Bank of Canada will cut interest rates later in the year rather than June, though Governor Macklem has clearly opened the door pretty wide to a June cut. In the United States, it appears unlikely that the Fed will be in a position to cut rates until at least September.

Key to central banks’ decisions are inflation prospects. In Canada, there is no doubt that recent inflation prints have been supportive of an earlier rather than later withdrawal of monetary stimulus. Headline inflation is hovering around 3% as are measures of underlying inflation. Even more constructively, the month-over-month evolution of trimmed means and median inflation, measures that are keenly watched by the Bank of Canada, are well below 2%. Taken in isolation, this is great news and is driving much of the Governor’s guarded optimism in relation to rate cuts.

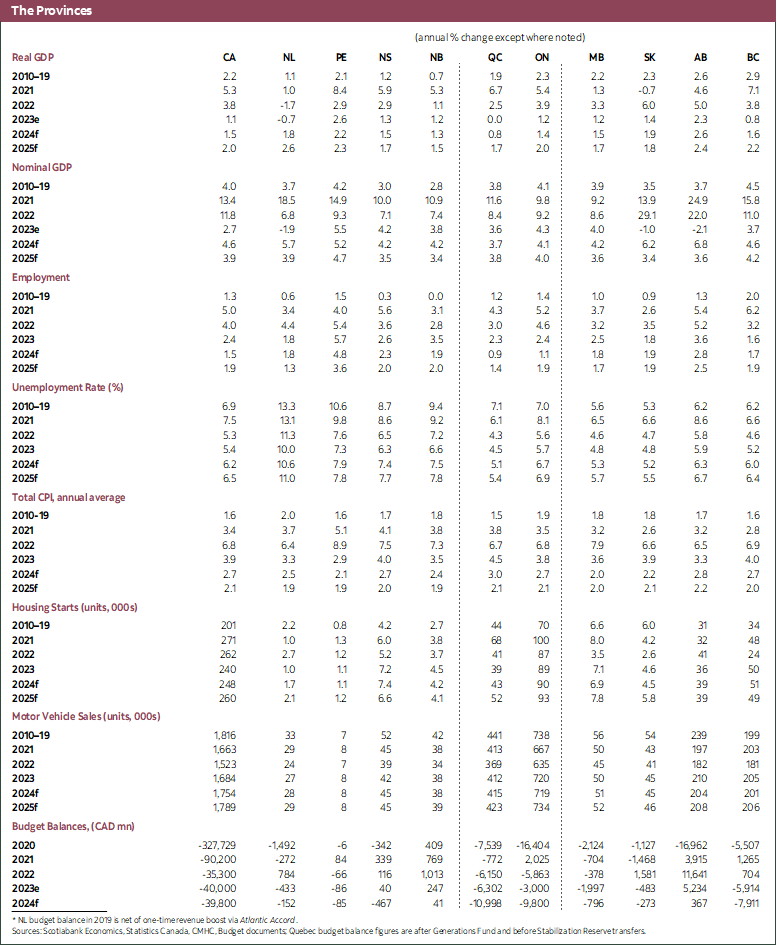

We believe the improvement in the inflation outlook needs to be set against a broad range of factors that suggest that more progress must be seen on the inflation front for the Bank of Canada to cut. Topping the list is the economic outlook. We now expect growth of about 1.5% in Canada this year. That is a large revision from our earlier forecast and reflects a number of compounding factors:

- Growth surprises at end-2023 that carried through in early 2024, notably on the consumer spending side. Retail sales have been much stronger than anticipated, as have auto sales and housing sales more generally. It is true that some interest-sensitive components of spending such as furniture and home goods remain soft, but those spending categories are tightly linked (with a lag) to home sales, which we know have increased and expect to rise further.

- Some of the strength in consumption is linked to population growth, as the Governor has noted numerous times. It is true that per capita consumption has been falling. That is likely the result of higher interest rates and a sign that monetary policy is working, but the surge in population growth continues. The rise in population growth so far this year exceeds the record pace we saw last year. As a result, there are many more spenders in the economy. And on balance, consumption spending is rising, which we believe should be of concern to the Bank of Canada.

- Adding to the underlying resilience in the economy are actions taken by the provincial and federal governments in recent budgets. There is not a shadow of a doubt that the jump in spending in recent budgets will boost growth this year and next. This is of course a repeat of policies of the last few years whereby our governments have been actively working to frustrate the Bank of Canada’s efforts to reign in inflation. To a significant degree, interest rates are at current levels because of policies put in place by all levels of government in recent years. Based on current budgets, we conservatively estimate that government spending will account for about half the growth expected this year in Canada. There is a chance that the governments contribute even more to growth than that.

- Oil prices have risen significantly in the last several weeks. This represents a large terms of trade shock for Canada, which add to growth but also to inflation indirectly through the growth channel, and directly through higher energy prices. This is likely to put modest upward pressure on inflation in coming months.

- Perhaps just as important as the factors above is the remarkable strength of the US economy. Analysts keep raising the US growth forecasts only for data to consistently come in stronger than expected. This is particularly notable along the household spending and industrial production dimensions. We expect US growth of around 2.4% in 2024, but the momentum in the economy is such that something closer to 3% is in the “realm of possibilities”. With nearly 80% of our exports going to the US, a strong US economy is unequivocally beneficial to Canada. And in the current environment this suggests added caution on the monetary policy side north of the border. This is all the more important given Chairman Powell’s recent remarks in which he signals the growth and inflation outcomes in the US reveal that it is too early to contemplate an easing in monetary policy.

- Finally, the Canadian dollar has been tumbling as markets reduce expected rate cuts in the US despite the substantial increase in oil prices. We do not believe current levels of the loonie are in line with fundamentals and expect a modest appreciation throughout the remainder of the year, but there is clear risk to this forecast. An early move by the Bank of Canada could put more downward pressure on the Canadian dollar and in so doing provide an additional boost to exports and some modest upward pressure on inflation. While the Governor has made it clear that our flexible exchange rate regime allows him to set the monetary policy that is right for Canada, we do think the risk of a further depreciation in the dollar should factor in their policy deliberations.

Moreover, the inflation data themselves require caution in interpreting. Given how much will ride on the next monetary policy decision, we believe the Governor will need almost absolute certainty that cutting rates is the right thing to do if he does move that way. The bar for a pivot on rates is much higher than the bar for an additional rate hike in a tightening cycle, or for an additional cut when rates are brought down. This high bar is all the more evident given the pause in January 2023 and the need to raise interest rates another 50 basis points later in 2023.

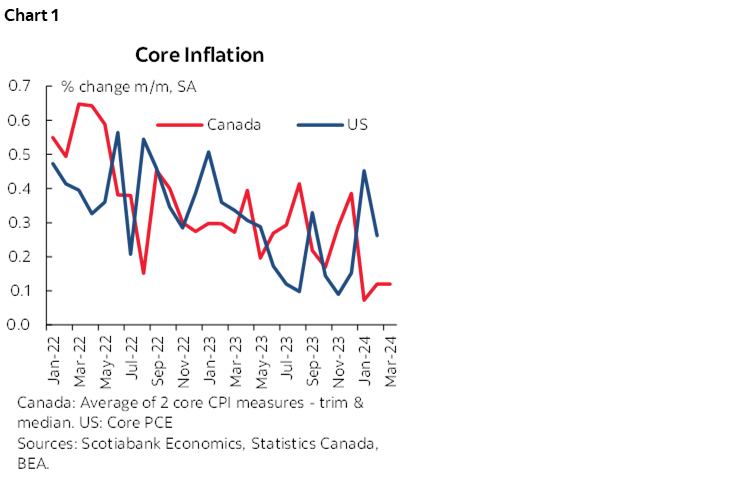

To that end, the experience with US inflation is instructive. The core PCE deflator decelerated sharply for much of last year on a month-over-month basis prompting many analysts to say that US inflation was vanquished. That led in part to rising bets that the Fed would cut rates sharply in 2024. We are now seeing the inverse of last year’s dynamics. US inflation has come in hotter than expected in the last three months (chart 1). Time will tell of course if this is the beginning of a new course of US inflation. In our view, that’s an important element for the Bank of Canada to consider: what if the same thing happens here after they have cut? That is not a risk worth taking in the short run in our view.

Finally, there are clear signs that the housing market is turning the corner as buyers look to lower interest rates as a signal to jump back into the market. The government’s decision to extend the maximum amortization length for first-time home buyers on insured mortgages for new construction as of August 1st should lead to more activity in the lead-up to that occurring given the intense supply-demand imbalances that exist in the market. Cutting rates well ahead of that change could add further upward momentum to what is arguably the most rate-sensitive part of the economy.

Taken together, we don’t think there will be enough evidence to meet the high bar for the monetary policy pivot in Canada as a result of all the reasons above. A move later in the year, in the third quarter, continues to be the more likely scenario. At the margin, weaker-than-expected inflation may suggest a move earlier in the quarter might be required. We realize that view diverges from others quite a bit. And we also realize that it goes somewhat against Governor Macklem’s implicit guidance that June was in the realm of possibilities. We nevertheless see no need to rush to cut given the many moving parts of the economy.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.