FISCAL OUTLOOK DETERIORATES IN AFFORDABILITY BUDGET

- Bottom line: Weaker revenue and higher spending have led PEI to anticipate larger deficits and a faster increase in debt than previously projected, despite some efforts to find fiscal savings and target new affordability measures. The decline in the deficit in future years will depend in large part on the achievement of the planned $200 mn annual savings through a spending review as well as the planned slowdown in health spending growth.

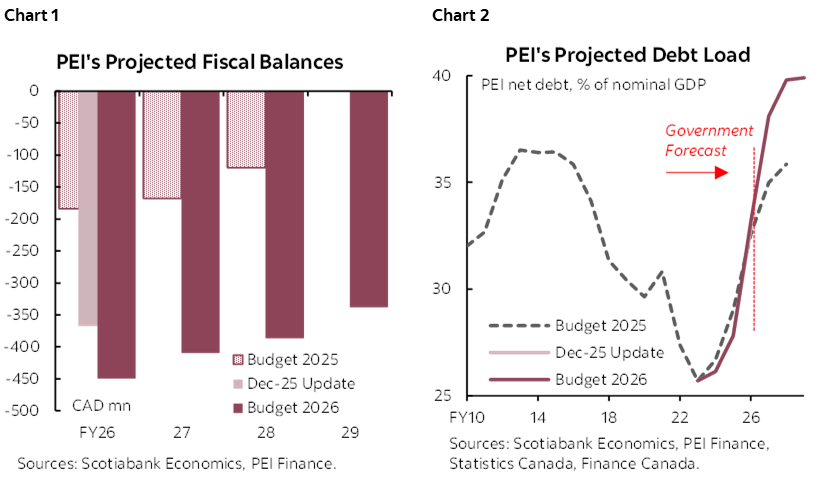

- Budget balance: the FY26 deficit is estimated to be $450 mn (4% of nominal GDP), up from $367 mn (3.2%) in the mid-year update, and is projected to decline from $410 mn (3.5%) in FY27 to $338 mn (2.6%) by FY29 (chart 1).

- Economic assumptions: real GDP growth is assumed to grow 2% in 2026 and 2027, down from an estimated 2.4% in 2025.

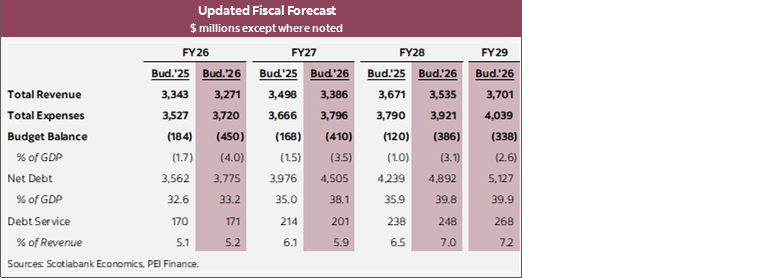

- Net debt: projected to rise from 33.2% in FY26 to 39.8% in FY28, higher than last year’s outlook of 35.9%, then holding at 39.9% in FY29 (chart 2).

- Borrowing requirements: set to be $918 mn in FY27, down from $1,053 mn in FY26.

OUT TAKE

PEI's Budget 2026 falls further into the red for longer with the deficit gradually declining over the outlook. PEI’s latest operating budget marks a clear deterioration in the near-term fiscal outlook versus both the December fiscal update and last year’s operating budget as the province now expects the budget balance for fiscal year 2025–26 (FY26) to be -$449.6 mn (-4.0% of nominal GDP), compared with -$367.4 mn (-3.2%) in the mid-year update and -$183.9 mn (-1.7%) in Budget 2025. The budget’s larger deficit reflects both a softer revenue track and a higher spending base relative to last year’s budget plan. The deficit is projected to gradually decline from $410 mn (3.5% of GDP) in FY27 to $338 mn (2.6%) in FY29. As such, the latest budget expects the province will be quickly approaching the ceilings of its fiscal anchors for net debt-to-GDP and the interest-to-revenue ratio, formally targeted in December 2025, by the end of the outlook.

Weaker revenues are weighing on the budget’s bottom line over the near-term. Total revenue was revised down by nearly $250 mn over FY27 and FY28 relative to last year’s budget. The previously announced increase in the basic personal exemption from $14,650 to $15,000 is expected to save residents $3.2 mn in income annually. Additionally, the province is proposing a new 20% tax bracket on income over $200 k, up from 19% currently. Total revenue is projected to increase 3.5% y/y to $3.39 bn in FY27, before increasing 4.4% y/y to $3.54 bn in FY28 and 4.7% y/y to $3.7 bn in FY29.

PEI’s expenditure plans point to a larger spending envelope over the medium term. Total expenditure is expected to increase to $3.8 bn in FY27, up from $3.72 bn in FY26, as the latest outlook adds more than $260 mn in spending across FY27 and FY28 compared to last year’s budget. Higher health spending is adding to overall expenditure over the outlook and is projected to rise from $1.16 bn in FY26 to $1.41 bn in FY27, $1.47 bn in FY28, and $1.53 bn in FY29. Other major program expenditures include Public Schools Branch which is planned to be $344 mn in FY27, up from $329.8 mn in FY26, and Social Development and Seniors spending at $246.9 mn in FY27, up from $241.8 mn in FY26. This is partially offset by lower program spending by other departments, including Transportation, Infrastructure, and Energy with planned expenditures of $279.1 mn in FY27, down from $317.4 mn in FY26. Most notably, the province is introducing $26 mn in funding for a new PEI Essentials Benefit, which is targeted to low- and middle-income residents, and complements an increase to the PEI child benefit. Helping fund these new affordability measures is the elimination of the PEI Energy Rebate Program. Looking beyond FY27, the government’s three‑year plan expects total expenditure will increase 3.3% y/y to $3.92 bn in FY28 and 3.0% y/y to $4.04 bn in FY29. As a measure to limit spending pressures, the province will be undertaking a multi-year comprehensive expenditure review that is estimated to save $195 mn in FY28 and $200 mn in FY29.

The higher deficits for longer will further driver up the province’s net debt over the outlook. Net debt is projected to rise from $3.77 bn (33.2% of GDP) in FY26 to $4.50 bn (38.1%) in FY27 and $4.89 bn (39.8%) in FY28, before reaching $5.13 bn (39.9%) in FY29. This is a steeper trajectory than last year’s budget, which anticipated a materially lower debt burden of 35.9% by FY28, and will be bumping up against the 40% net debt-to-GDP ceiling. The budget assumes that nominal GDP will grow 4% in 2026 and 2027, before increasing 4.5% per year thereafter. Meanwhile, real GDP growth is assumed to grow 2% in 2026 and 2027, down from an estimated 2.4% in 2025 amid trade uncertainty and slowing population growth. Higher debt also keeps interest costs elevated, as spending on debt services rises from $170.8 mn in FY26 to $247.8 mn in FY28 and $268.1 mn in FY29, pushing debt service to roughly 7.0%–7.2% of revenue in the outer years, up from 5.2% in FY26, and close to the province’s fiscal anchor of keeping the interest-to-revenue ratio below 7.5%.

The province’s cash requirements remain elevated amid the large deficits and capital program. For FY27, total cash needs are estimated at $918.4 mn, down from $1,052.7 mn in FY26, driven by the consolidated deficit ($410 mn), $486.5 mn in capital asset acquisitions, and $105.1 mn in net borrowing on behalf of Crown corporations, which is partially offset by $166.2 mn in amortization. These borrowing requirements are planned to be met through $900 mn in long‑term borrowing and $18.4 mn in short‑term borrowing and working capital.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.