PROMISING GROWTH OUTLOOK SPURS MAJOR SPENDING PLANS

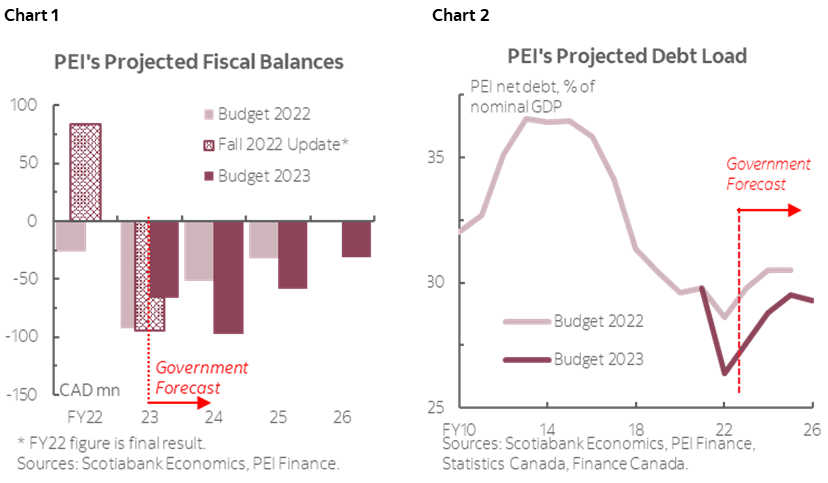

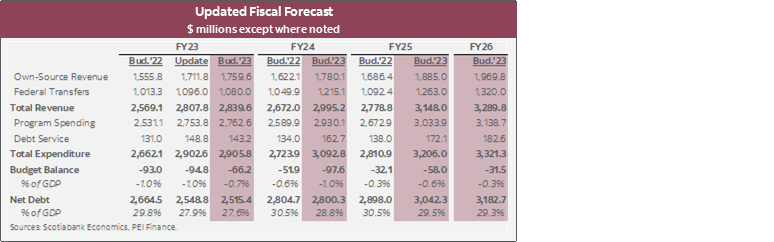

- Budget balance forecasts: -$66.2 mn (-0.7% of nominal GDP) in FY23, -$97.6mn (-1%) in FY24, -$58.0 mn (-0.6%) in FY25, -$31.5 mn (-0.3%) in FY26—a better-than-anticipated starting point followed by deeper deficits projected for the next two years relative to the last budget with no return to balance in sight (chart 1).

- New policy measures focus on health, housing and affordability.

- Net debt-to-GDP: expected to edge up from 27.6% in FY23 to 28.8% in FY24—1.7 ppts below forecast in last year’s budget—then stabilizes at levels above 29% in FY25 and FY26 (chart 2).

- Real GDP growth: +2.9% in 2022, 3.5% in 2023—well above private-sector forecast range of 0.8–2% in 2023; nominal GDP growth: +4.4% in 2022, +6.5% in 2023, +6.0% in 2024.

- Borrowing: $374 mn cash requirements forecast for FY24 of which $250 mn is long-term, up 27% from FY23.

- The budget features tax system changes and major new investments in housing and healthcare. Although more prudence is warranted in a highly uncertain economic environment, we acknowledge the imperative to increase spending to cater to the province’s fast-growing population.

OUR TAKE

The re-elected PEI Progressive Conservative government tabled a budget with a considerable increase in spending supported by an optimistic growth projection. Higher-than-anticipated own-source revenue puts PEI on a better starting point and the province is projecting a narrower deficit of -$66.2 mn (-0.7% of nominal GDP) in FY23—a $28.6 mn improvement from its mid-year fiscal update. The province expects the deficit to widen to -$97.6mn (-1.0%) in FY24 as growth slows and total spending rises by 6.4%. In outer years, the province sees the deficit fall to more modest levels of -$58.0 mn (-0.6%) in FY25 and -$31.5 mn (-0.3%) in FY26.

Revenues are forecast to rise by 5.5% in FY24, mostly attributable to a material boost in federal transfers. PEI anticipates $1.2 bn in major transfers in FY24—up 12.5% over FY23 and accounting for 87% of revenue increases. Own-source revenues are expected to rise modestly by 1.2% in FY24 even with the fiscal impact of new tax relief measures. Over the medium term, total revenue is set to grow at an average pace of 4.8% through FY26.

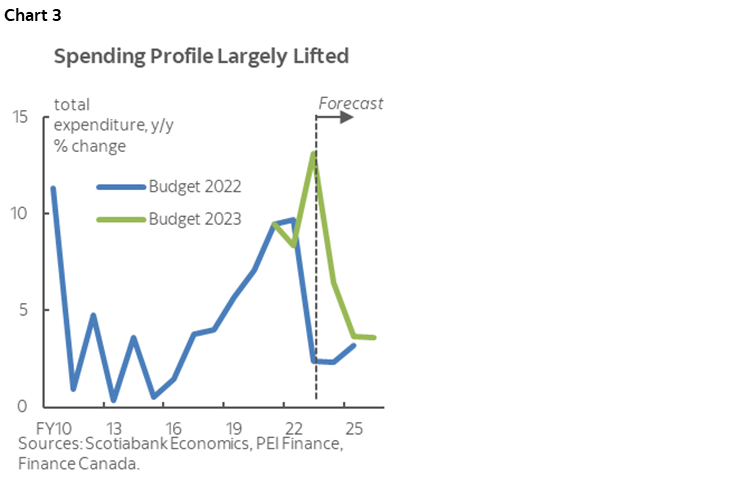

Following a surge of 13.1% last year, the province’s total expenditures saw another substantial boost in the near term (chart 3), partly offset by additional funding support from the federal government. Total expenditures are slated to grow by $187 mn (6.4%), including a $136.5 mn (15.0%) bump to health and wellness. Over the medium term, total spending will continue to grow at an average pace of 3.6% per year, within the bound of projected revenue growth. Debt service costs are expected to be $19.5 mn (13.6%) higher in FY24, accounting for 5.5% of total revenue in FY24, up from 5.0% in FY23.

Policy measures fall into three categories: health, housing and affordability. Extra funding was allocated to medical homes ($8.9 mn), prescription drugs and the Pharmacy Plus program ($13 mn), and enhancing mental health supports ($3.2 mn). Other major healthcare investments include $21.9 mn combined capital and operational spending designated to establishing the UPEI Medical School. Investments in housing include $6 mn to offset property tax increases and $1 mn to launch a new rent-to-own program. The budget contains tax relief measures helping with rising cost of living, tallying up over $14 mn in FY24. These include an increase in the Basic Personal Amount to reach $13,500 by 2024, a $750 increase in the income threshold eligible for the low-income tax reduction and a five-bracket income tax system.

The growth projections underpinning the outlook hinge on strong population growth assumptions and are significantly more optimistic than the private-sector forecast range. PEI enjoyed the highest population growth (3.6%) in the province’s history and among its peers last year, and projects another 3.5% growth this year. The province expects rising international immigration and positive inter-provincial migration to continue anchoring its population expansion plan with its headcount reaching 200k by the early 2030s. With an optimistic growth trajectory, extra caution is warranted in a highly uncertain environment, especially given volatilities of the province’s main sectors and the shaky economic outlooks of its main trading partners. The budget included contingencies totaling $43 mn (1.4% of total expenditures) in FY24 to absorb potential costs/losses associated with salary negotiations and other extraordinary events.

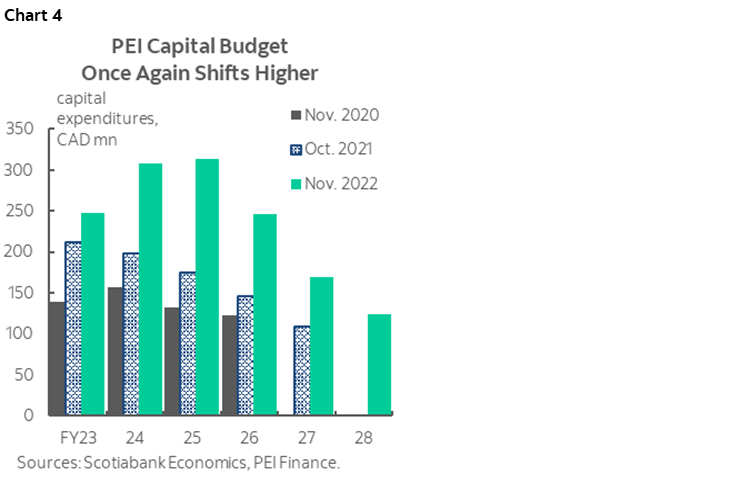

The island continues to boost infrastructure spending to bolster its economic potential. The province’s ambitious FY23 capital plan was unveiled in November last year and targets spending above $1 bn for the next five years—$321 mn (38.1%) higher than its last 5-year plan (chart 4). The enhanced plan aims to improve the province’s climate resiliency ($24.5 mn), healthcare ($92 mn), housing affordability ($100 mn) and education ($30 mn).

With strong projected nominal growth in the next three years, the province’s net debt trajectory remains well below the historical average as a share of output. Revised down slightly relative to the last budget as a share of nominal output, the net debt-to-GDP ratio is now expected to increase steadily from 27.6% in FY23 to above 29% by FY26. Although PEI still enjoys the second lowest debt burden among provinces east of Saskatchewan, it is on an upward trajectory and an unforeseen slowdown in growth could put the province’s net debt-to-GDP ratio on a higher path. With more deficits on the horizon, PEI is expected to increase its cash requirements from $295 mn in FY23 (68% is long-term) to $374 mn in FY24 (67% is long-term).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.