FINANCIALLY DODGING THE COVID BULLET, READY TO MOVE ON

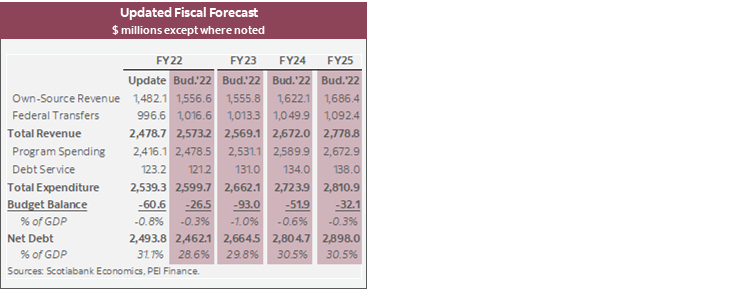

- Budget balance forecasts: -$26.5 mn (-0.3% of nominal GDP) in FY22, -$93 mn (-1.0%) in FY23, -$51.9 mn (-0.6%) in FY24, -$32.1 mn (-0.3%) in FY25—narrower as a share of GDP than expected in many other provinces even at its peak (chart 1).

- New policy measures focus on health, child care, and economic recovery.

- Net debt: expected to edge up from 28.6% in FY22 to 29.8% in FY23, then stabilize at 30.5% in FY24 and FY25—well below forecast in last year’s budget (chart 2).

- Real GDP growth: +3.5% in 2021, +2.9% in 2022 anticipated by the average private-sector forecast—following the mildest contraction among provinces in 2020 at -1.7% of GDP.

- Borrowing: $213 mn in FY22 of which $200 mn is long-term; $332 mn cash requirements forecast for FY23 of which $250 mn is long-term, slightly up from FY22.

- The budget confirmed PEI’s outstanding track record in pandemic management and prudent fiscal planning. We believe the budget outlined a credible three-year framework that maintains PEI’s financial advantage.

OUR TAKE

Effective pandemic management and prudent fiscal planning has enabled PEI to minimize fiscal shocks, running only modest and declining deficits over the horizon, while still supporting targeted additional investments. Recall that the province settled at a meagre of $5.6 mn deficit in FY21 (less than 0.1% of nominal GDP), before slashing its forecast FY22 deficit by three-quarters from the previous Budget to $26.5 mn (-0.3% of GDP) in the latest estimate. With that track record, PEI plans to increase expenditures by 2.4% in FY23, and with revenues relatively flat, the shortfall is expected to widen to $93 mn (1.0% of GDP). The plan anticipates a gradual reduction of deficits over the three-year horizon—driven by strong revenue growth in FY24 and FY25 and stabilizing expenditures—to -$32.1 mn (-0.3% of GDP) in FY25.

Despite a temporary slow-down in FY23, robust growth in the province’s own-source revenues and federal funding should continue to support future spending initiatives and debt servicing costs. Revenues are projected to decrease slightly from both provincial and federal sources in FY23, before picking up again by an annual rate of 4% from both sources in FY24 and 25. Meanwhile, the three-year plan suggests expenditures will grow across the planned horizon, yet at a slower rate of 2–3%. Debt service cost is expected to increase slightly as a share of revenue from 4.7% in FY22 to 5.1% in FY23, and edge down to 5% in FY25.

Policy measures have a focus on health and economic recovery. Extra funding was allocated to recruit specialized physicians, support the medical homes and neighbourhoods project—an Island-based electronic platform that connects patients and health care practitioners at the local level—and expand the dental care program. In partnership with the federal government, PEI plans to improve the availability of child care and early education. The budget also outlined efforts to improve clean and affordable energy and public transit in the province. More relevant to the recent discussions on rising inflation, there will also be an increase in the Basic Personal Taxable Amount tied to the Consumer Price Index.

Federal transfer projections were lifted again and will remain an important source of income across the three-year fiscal framework. PEI now expects to receive $1,017 mn (40% of revenues) from the federal government in FY22, $43 mn higher versus the last Budget. The plan then assumes the FY23 transfers to remain on the same level even with the removal of some pandemic support, then grow at an average annual rate of 3.9% during FY24–25 to hold steady near 40% of provincial government receipts.

Prudent fiscal planning continues to account for potential downside risks. The nominal GDP assumptions underpinning the deficits sat at very modest levels of 3.9 % for 2022, 3.0% for 2023, and 3.2% in 2024. While caution is warranted considering the volatilities of the province’s main industries, most private-sector forecasters project higher nominal growth for the island. The budget also included two contingencies worth $15 mn (0.6% of total expenditures) each in FY23 to absorb potential costs/losses associated with two areas of uncertainty—COVID-19 and the US potato export ban.

The province expects immigration to remain the anchor of its population expansion plans, and again contribute significantly to economic growth in the coming year. Before the pandemic, immigration contributed more to population gains in PEI than in any other province. PEI anticipates that 2,500 newcomers will arrive on the Island in 2022—the second-highest ever recorded total—as travel linkages improve, system backlogs are processed, and pandemic restrictions ease. That surge should support labour force growth this year, though omicron wave impacts will likely delay the recovery and exacerbate job vacancy rates early in 2022.

Despite the 2 ppts projected increase as a share of output from FY22 to FY25, the province’s net debt trajectory remains well below the historical average, as well as levels expected in many other provinces. With more deficits on the horizon, PEI is expected to increase its cash requirements from $213 mn in FY22 (94% is long-term) to $332 mn in FY23 (75% is long-term).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.