PANDEMIC RECOVERY BEGINS WITH BOOKS DEEPER IN THE RED

SUMMARY

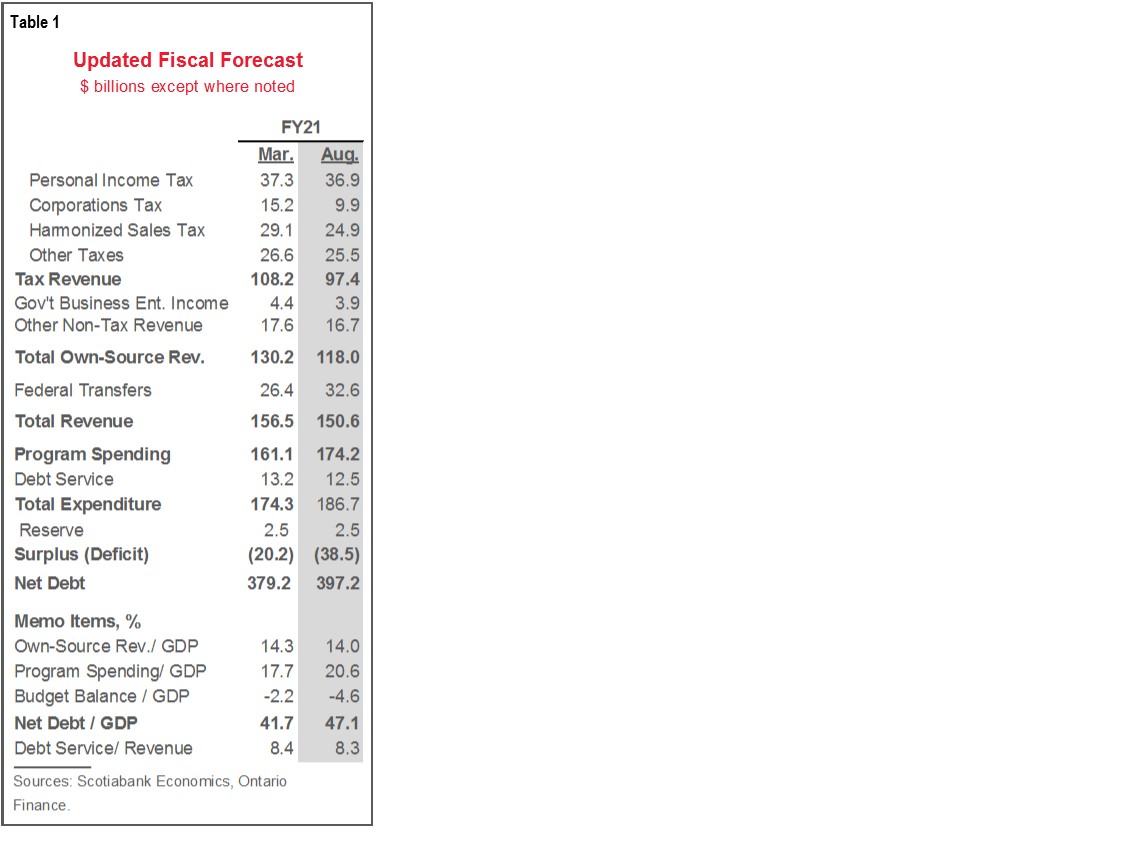

Like most of the world, the Province of Ontario’s finances will take a hit from the COVID-19 pandemic: a record $38.5 bn deficit (4.6% of nominal GDP) is now planned for fiscal year 2020–21 (FY21).

The fiscal shortfall is a natural consequence of the historic economic contraction expected this year; accordingly, net debt is forecast to hit a record 47.1% of GDP, with borrowing projections also shifting higher.

Despite risks and expectations of an extended post-lockdown period of convalescence, positively trending economic indicators, easing caseloads, and ongoing advantages bode well for a solid recovery.

OUR TAKE

As expected, and as seen across the globe, the COVID-19 pandemic has created a far more difficult economic and fiscal environment for Ontario. That is clearly reflected in the record economic contraction, deficit, and debt levels anticipated this year. The government will likely need to continue to provide targeted fiscal support throughout the forecast horizon, in the context of a medium term plan to consolidate its balance sheet. The large deficit and debt loads relative to other jurisdictions in Canada that Ontario carried into the pandemic will make striking that balance all the more challenging.

Despite the risks, Ontario looks to be in a position to generate a solid recovery. Caseloads have thus far continued to diminish since the Province advanced into the latest phase of its reopening plan. Accordingly, several sectors of the economy are rebounding significantly, albeit off of a lower base. Fiscal supports detailed today acknowledge the severity of this historic downturn and should bolster the recovery. Amid an uncertain outlook, sizeable contingencies provide a cushion against further shocks and present some upside for budget balances to the extent that the recovery continues. And the provincial economy—when open—is one of the most vibrant in Canada. The road ahead will be a long one, but Ontario appears to be moving in the right direction.

ECONOMIC OUTLOOK

As seen elsewhere in the world, the COVID-19 pandemic has hit Ontario’s economy hard. Alongside plunging global activity, measures to contain the virus’ spread are forecast to drive a 6.7% real output drop this year—more than twice the previous record loss of 3.2% during the early 1980’s recession (chart 1, p.2). Recall that zero growth was built into the prior plan released in March, before COVID-19’s full impacts became clear. The Province foresees a smaller 5.3% dip in nominal GDP—in line with expectations of imported inflation in other net oil-consuming regions. The downturn’s widespread nature is reflected in pronounced declines in both nominal household spending and corporate profits. The virus’ spread among key trading partners—notably the US—remains a risk.

Yet economic activity has improved considerably as caseloads and containment measures have eased. Total employment, retail trade, housing starts, and home resales have all surged since the nadirs reached during peak lockdowns, with home purchases standing out for their particularly robust rebound. Despite border closures and travel restrictions, recent population gains in the order of 1.8% are expected to be maintained in 2020. Ontario’s diminishing infection rates (chart 2)—even amid continued relaxation of COVID-19 restrictions—also augur well for further gains. In part due to that momentum, the Province anticipates real economic growth of 5.5% in 2021, a healthy advance, but one that would still leave provincial output roughly 2% below its 2019 average next year.

FISCAL DETAILS

As provincial economic forecasts were revised lower, so too were provincial revenue projections. Total government receipts are expected to come in $5.7 bn lower than anticipated in March. Combined declines in corporate tax ($5.2 bn), sales tax ($4.2 bn), and miscellaneous other taxes ($1.5 bn) exceed the total downward revision, with a partial offset via a $6.2 bn increase in transfers from the Federal Government. The bulk of the jump in transfers stems from the Safe Restart Agreement. Still, the 3.9% decrease in total revenues penciled in for this year would represent the steepest decline since FY09.

Mirroring a range of new supports for the economic recovery, total expenditure plans were raised by $12.4 bn versus March. They are now on pace to climb by 12.6% in FY21, the largest gain since the 14.5% rise seen in FY10 at the height of the Global Financial Crisis (chart 3). As part of the Safe Restart Agreement, the Province allocated $2.2 bn to municipal and transit priorities. To bolster the recovery, the People and Jobs Fund—initially allotted almost $2 bn in funds in March—will receive a $3 bn top-up. The government will also apportion a further $4.3 bn to its Health Contingency Fund, and increase its standard contingency fund by $2.2 bn.

The $38.5 bn deficit (4.6% of nominal GDP) outlined for FY21—nearly twice the March projection—is a natural consequence of the hit to government revenues and increase in pandemic spending. In both nominal balance and output share terms, the fiscal shortfall would represent the Province’s largest since at least FY87. A $2.5 bn reserve is in place to cushion against unexpected revenue and spending shocks.

Mirroring the record deficit, Ontario expects to carry a net debt burden equal to 47.1% of nominal GDP this fiscal year. That is more than five ppts higher than anticipated in the prior fiscal blueprint and also represents a post-FY87 record high (chart 4, p.3). With interest rates on a lower trajectory in light of the softer economic outlook, debt servicing costs were revised $741 mn lower than anticipated in March. Servicing of debt is expected to account for 8.3% of total revenues—also lower than forecast in March.

Also largely reflecting the wider fiscal shortfall, total Provincial funding requirements are projected to climb $17 bn higher than outlined in March. Total long-term borrowing is expected to reach $52.1 bn in FY21. By August 12, Ontario had already completed $23.6 bn of that total. Roughly three-quarters was denominated in Canadian dollars, with the remainder issued in USD, Pounds sterling and Euros. The Province anticipates that the Bank of Canada’s Provincial Money Market Purchase (PMMP) program will allow it to raise $5 bn more in short term borrowing than outlined in March. Secondary market purchases of Ontario bonds under the Bank’s Provincial Bond Purchase Program (PBPP) are expected to far exceed the planned increase in long-term borrowing.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.