- Inflation rates may be distorted…

- …because of the way that revised weights are incorporated…

- …which leaves us with poor ability to track true inflation

- How this could have been avoided

- The BoC has added reason to be more circumspect toward what is happening with inflation

Canadian CPI, m/m / y/y %, June:

Actual: 0.3 / 3.1

Scotia: 0.6 / 3.5

Consensus: 0.4 / 3.2

Prior: 0.5 / 3.6

Canadian core CPI, y/y % change, June:

Average: 2.2 (prior 2.3%)

Weighted median: 2.4 (prior 2.4%)

Common component: 1.7 (prior 1.8%)

Trimmed mean: 2.6 (prior 2.7%)

While headline and core inflation appeared to land softer than expected, there is strong cause to counsel treating the results with caution. The year-over-year and month-over-month rates of inflation may have unfortunately lost their usefulness at an important transition point for monetary policy given the way Statistics Canada (and other global agencies) incorporate basket weight changes into CPI, given the chosen timing of that transition and given the absence of other simultaneous attempts the agency could have provided in an effort to offer a fuller picture of true inflation.

This frankly means that for policy purposes we’re left flying blind on true underlying inflation and that markets may have over-reacted somewhat to the perceived miss relative to expectations. Note that the Canadian dollar initially depreciated by about a quarter cent to the USD and shorter-term yields rallied before these effects stabilized.

THEY LOST THE PLOT TO THE INFLATION STORY

At issue is Statistics Canada’s choice of the chain-link reference month for incorporating new basket weights. Up to May 2021 the basket weights are still set at 2017 levels and nothing gets revised for changed pandemic-era spending patterns. Starting in June 2021 onward those weights are set at the revised 2020 basket weights that were updated last Wednesday.

That means that when we are looking at year-over-year headline and core inflation rates we are comparing amoebas to blue whales in that June 2020 price index levels are still set at 2017 weights. Ditto for every other month during the pandemic to date except for starting with June 2021. When StatsCan says that the year-over-year CPI inflation rate would have been 3.1% regardless of whether 2017 or 2020 weights are used they are arriving at this conclusion only because they are not adjusting June 2020 for the revised 2020 weights in addition to the June 2021 index levels at 2020 weights. They are only saying that June/June would be the same if they were still using 2017 basket weights, or if June 2021 used 2020 weights compared to June 2020 at 2017 weights which isn’t a useful comparison. What we needed was June 2021 at 2020 spending weights compared to June 2020 at 2020 spending weights and the same thing for each historical month during the pandemic in order to assess the evolution of inflationary pressures.

It’s standard practice for global statistical agencies to transition from one set of basket weights to a revised set at a particular month without revising history and this point is called the chain-link reference month. That part is understood and the agency is doing so competently in keeping with global and historical practices.

It’s just unfortunate that in the midst of the pandemic we’ve lost the continuity of the spending basket’s influences upon inflation to reflect changes in spending behaviour that are only being incorporated from June 2021 onward. That makes the year-over-year rates an unreliable depiction of what is truly happening to inflation. It’s a case of doing the right thing in a data nerd sense by keeping with standard data practices over time and internationally while missing the whole plot of the story from a market and policy standpoint in terms of the need to provide reliable inflation estimates that reflect pandemic-era realities.

HOW THIS COULD HAVE BEEN AVOIDED

StatsCan could have addressed this in one of at least a couple of ways, or it could now be incumbent upon the BoC to do so. One way would have been to provide shadow CPI figures using a chain-link reference month set for the beginning of the pandemic or, say, the end of 2019. That would have allowed us to track a constant basket of spending behaviour and the price implications throughout 2020–21.

Alternatively they could have simultaneously published an updated version of their adjusted CPI measure (last one here) that dynamically adjusts spending weights each month throughout the pandemic and which was tracking about 0.4% higher than official CPI on a year-over-year basis the last time they published it. Instead, the agency will publish a revised methodology and estimates for the adjusted CPI measure ‘later in the Fall’ and hasn’t reported on the measure with estimates fresher than January 2021 when it was tracking about 0.4% higher than the official headline y/y CPI rate. They teased us with inflation estimates that were tracking higher than the official CPI estimates but then subsequently lost the whole point of the efforts.

BoC IMPLICATIONS

Former Governor Dodge was on the mark yesterday when he indicated that the BoC should be more circumspect toward inflation risk. He’s even more correct today in that if we don’t have a good handle on true inflation at a vulnerable transition point then the BoC has even less reason to sound so strident with its exaggerated conviction that everything is all just transitory and driven solely by base effects that now can’t even really be judged. There is also the residual issues stemming from the earlier flap over seasonality adjustments to components of the basket and wherever that now stands.

DETAILS, FWIW!!

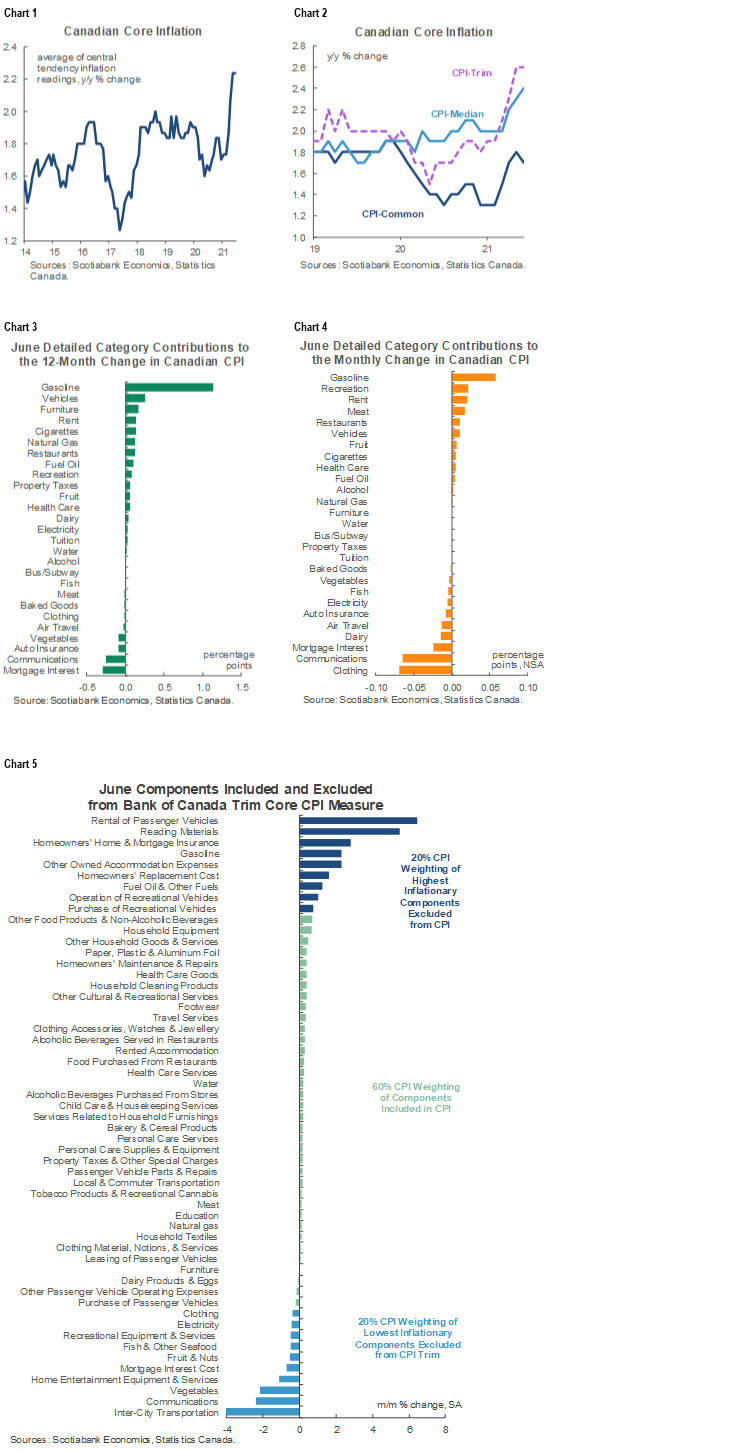

Because of the comparability issue at a transition point for the spending basket it’s largely pointless to delve too deeply into the composition of changes to inflation tracking. That will therefore be kept brief by referring the reader to charts 1–5. They show unchanged average core inflation at 2.2% y/y, the breakdown of the core measures, the breakdown of the weighted contributions to the year-over-year headline inflation rate, the same thing for the month-ago inflation rate and a breakdown of the trimmed mean CPI basket on the next page.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.