- Explosive job growth continues

- Wage growth eased, but the trend remains strong

- Hot pre-holiday core CPI and strong jobs add to BoC hike prospects…

- ...pending another upcoming CPI report and BoC surveys

- Strong employment, moribund productivity and uncertainty over why

- Why is trend job growth accelerating despite 12–24 months of higher bond yields?

- Canadian Jobs, m/m 000s // UR %, December, SA:

- Actual: 104 / 5.0

- Scotia: 15.0 / 5.0

- Consensus: 5.0 / 5.2

- Prior: 10.1 / 5.1

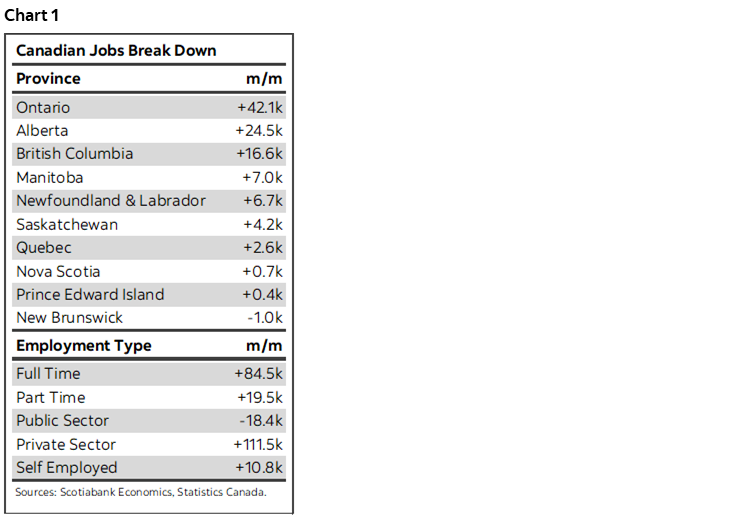

You go, Canada! The only thing better than seeing Canada’s junior men’s hockey team win gold for the 20th time last night is to follow it up with a ripping jobs report. Some details are provided in chart 1 and the table above. Clearly the gain blows the bands and is highly statistically significant given that the 95% confidence interval around what this survey pegs for job growth is about +/-57k. 100k more than consensus and a slightly smaller beat compared to my own guess can’t be dismissed as noise.

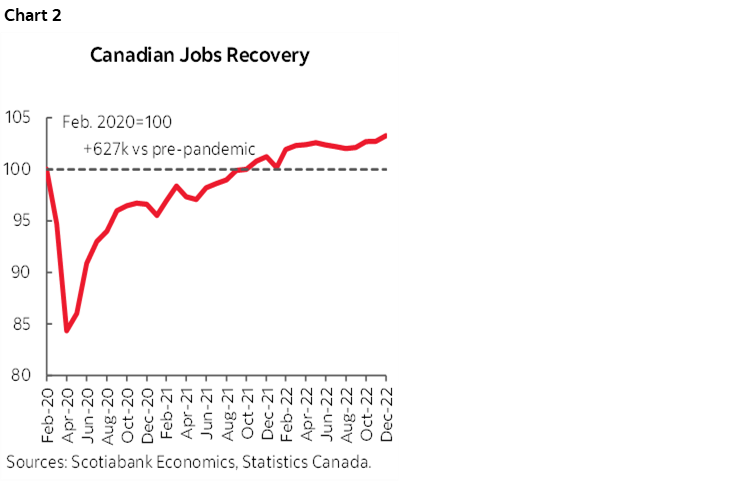

The trend is even more impressive. Canada now has 627k more jobs than it did before the pandemic struck (chart 2). 222k of those jobs came in the fourth quarter of 2022. The body count masks moribund performance on labour productivity as the cost to this explosive growth which I’ll come back to along with why this may be happening.

BANK OF CANADA IMPLICATIONS

The trade-off is that this makes it even more likely that the Bank of Canada hikes again on January 25th in keeping with the bias I’ve had since the BoC’s December communications including on statement day (here) and subsequent communications plus following the December 21st inflation report (here). Governor Macklem and Deputy Governor Kozicki made it abundantly clear in their round of communications in December that they were open to either a hold or a hike this month and it would depend upon the data leading up to the meeting.

Well, hot core CPI followed by hot jobs lean toward continued hiking. That said, before firming up a call, I would still like to see the CPI inflation figures two Tuesdays from now and the BoC’s surveys including measures of wage and inflation expectations the day before. Macklem’s panel appearance next week might be risk, but low risk.

MARKET REACTION

Markets responded in mixed fashion because of the dual influences of the US data whereby nonfarm’s 223k was priced post-ADP and yet US wage growth decelerated with downward revisions. ISM-services then disappointed at 10amET. The result is that the Canadian dollar has appreciated with USDCAD falling by about one-and-a-third pennies. Canada’s 2-year yield had risen a few basis points in the immediate aftermath of the Canadian jobs numbers but then fell by about 7bps post-ISM as it was dragged lower by the 17bps rally in US 2s on the day while still underperforming the US front-end. OIS is now pricing about 75% odds of a 25bps BoC hike on January 25th and a terminal rate of between 4.5–4.75% from a policy rate that is currently set at 4.25%.

DETAILS SHOWCASE STRENGTH

Payroll jobs were up by 93k and got an assist from an 11k rise in self-employment. Within payrolls, it was all private sector driven (+112k) as public sector jobs fell by about 18k.

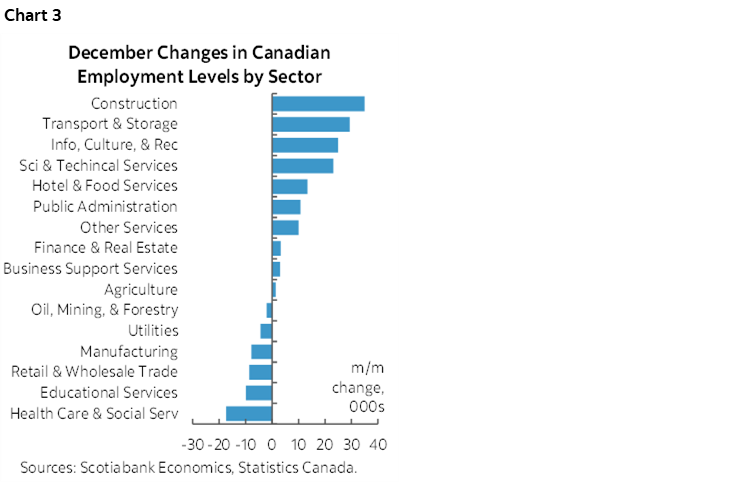

Sectoral breadth was high (chart 3). The goods sector added 22k and services added 82k jobs. Within goods, despite the fears, it was all about construction jobs (+35k). Construction employment stands at an all-time record high which probably highlights the supply pressures on the new build segment versus the correction on the resales side of the picture. Absent supply while jacking up immigration rates logically requires growing the housing stock which remains a point that the housing bears are totally ignoring. Immigration plus a positive terms of trade lift and robust job markets make it hard to go all-in on housing downsides offered by competitor narratives.

Within services, the leaders were transportation and warehousing (+29k), info/culture/recreation (+25k), and professional/scientific/technical which includes everything from accountants to engineers (+23k). There were milder gains in most other categories. In fact, out of 16 main subsectors, jobs were up in 10 of them. Within just services, jobs were up in 8 out of 11 sectors.

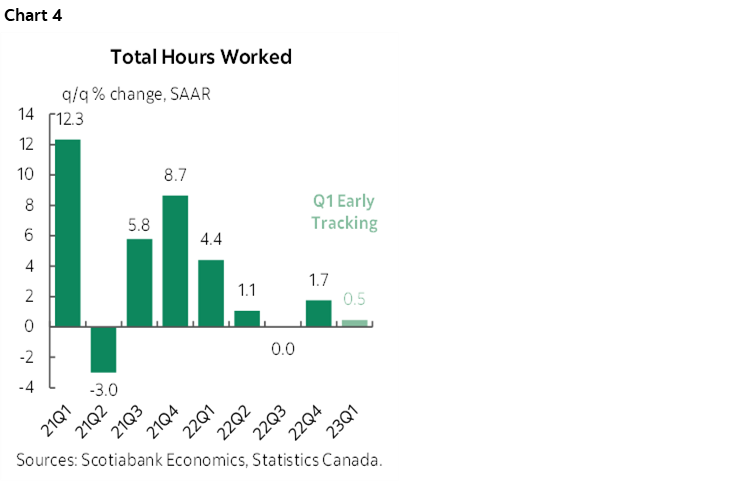

Hours worked were up by 0.1% m/m SA for the third straight gain. They increased by 1.7% q/q SAAR in Q4 and the way the quarter ended relative to the overall quarter bakes in ½% growth in hours worked in 2023Q1 before we start to get any Q1 data (chart 4). Overall, since GDP is an identity defined as hours worked times labour productivity (itself defined as real GDP per hour worked), these gains remain supportive of continued GDP growth roughly around estimates of potential growth. In other words, to date, and following torrid world-beating growth from 2021Q3 through 2022Q3, the Canadian economy is making no progress toward opening up disinflationary slack.

The unemployment rate fell to 5% from 5.1% and lower than the consensus estimate of 5.2% but on my estimate. Yeah yeah, ok, job growth was wayyy beyond what I had guessed. Meh, small victories people, small victories.

Ontario, Alberta and BC led the way. Ontario saw 42k more jobs created with every one of them being full-time. Alberta heaped on 25k more jobs, all full-time (41k). BC added 17k, but all part-time (+25k).

Younger and older workers were the main winners. Youth employment was up by 69k, mostly in full-time (54k). Men over 25 gained 23k jobs with women over 25 added 12k. Workers over 55 years of age gained 31k jobs.

Statcan noted that illness continued to weigh down workforce participation. 8.1% of workers were absent due to illness or injury and with all manner of viruses in circulation to blame. Even my household which miraculously avoided earlier waves was taken down in December. Statcan noted that the pre-pandemic norm for December is about 6.9%. That’s a meaningful shortage of workers and we need to be cautious toward the risks on this front well into 2023 as China’s decision to blow open the barn doors poses a potential ripple effect across global covid cases.

BE CAREFUL TOWARD COOLER WAGE GROWTH

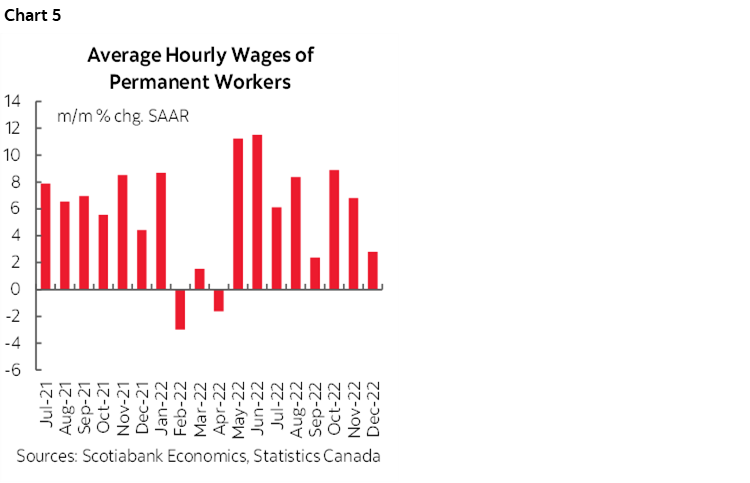

Wage growth eased to 2.8% m/m SAAR in December. This follows 6.8% growth the prior month. We’ve seen softer patches during the acceleration in wage growth like in September with a similar performance. Still, the trend is very strong as shown in chart 5. Average monthly seasonally adjusted and annualized growth in average hourly earnings of permanent workers has been 7.3% over the period from May through December.

Furthermore, watch the contract-based wage settlement figures (chart 6). This data is from a separate lagging (October) Statcan source but the average wage gain being booked in the first of an average three year contract has rising to 4.3% with a three-year average gain of 3.9%. So, 4% wage growth per year is the highest in a very long time and continuing to accelerate. It may continue to face upward pressure given motions from labour unions and developments in the public sector. On the latter count, watch Ontario’s court appeal of the ruling that struck down its imposed 1% per year wage contract with further possible implications for retroactive payments.

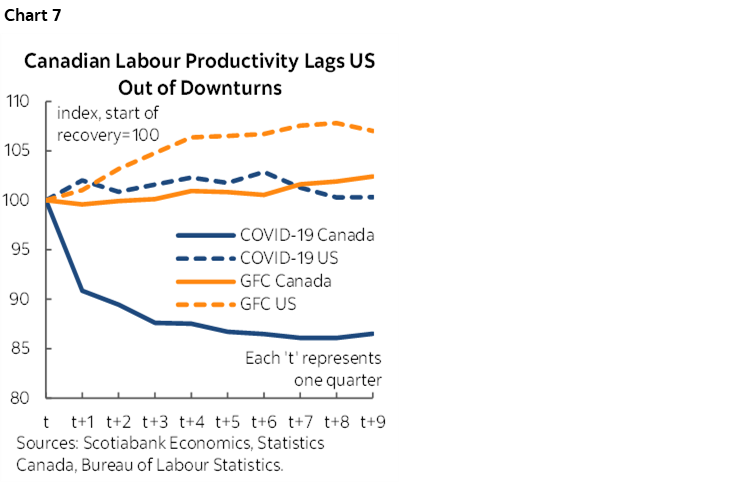

The added consideration I keep emphasizing is also the fact that Canadian labour productivity blows. Absolutely stinks. Except for you the reader and I of course, but someone’s shirking out there! See chart 7. Real GDP per hour worked has collapsed in far worse ways during the pandemic than in the aftermath of the GFC and in far worse ways than in the US.

The combination of any wage growth alongside poor productivity is unflattering to the average Canadian worker. It says they are getting paid more for producing less which is hardly the path to prosperity. That’s inflationary on both counts and should concern the country’s policymakers, private sector employers, those interested in the country’s competitiveness and ultimately workers themselves.

Why this is happening isn’t clear, at least to me. Canada’s productivity drivers and challenges have been debated ad nauseam for many years and this has long sparked uncertainty and disagreement. One possibility is that job supports were too generous earlier on, but that’s getting to be a rather old argument now. Another is labour hording by employers in a slower growing labour force and if they have to hire more workers to make up for the fact that job supports earlier on didn’t let the market adjust to changed circumstances. Another is that as population growth picks up, the surge of immigration is being soaked up faster than output can initially rise and maybe productivity will catch up, but this doesn’t explain much of the full pandemic experience given the recency of the pick up in immigration. Another could be underinvestment by businesses for various reasons not least of which being due to high uncertainty plus the long-lived historical performance on the cap-ex stock relative to GDP in Canada versus the US and other measures like R&D spending and technology adoption rates. Still another could be that as supply chains recover and businesses are reticent to heap on fixed costs in this environment they may have a preference toward labour over capital which—because of the supply-side drivers—could continue to make this a very different environment for the labour market compared to past tightening cycles.

THE OTHER SHOE HAS ALREADY DROPPED

Whatever the drivers, Canada’s job market is on fire. There will be those who counsel caution that the other shoe is waiting to drop because of lagging effects of tighter monetary policy. To a degree they are probably right, since rate hikes only began in March.

That said, we’ve had 15–24 months of higher 2- and 5-year Government of Canada bond yields that didn’t sit around waiting for the BoC to finally start hiking as they priced this risk in advance of when slow footed central banks began to wake up. Why isn’t the job market already cooling? For that matter, it’s even more puzzling to see job growth accelerate with a whopping 222k jobs created in the final quarter of 2022. At least so far, that doesn’t exactly smell like a pending recession. Indeed, perhaps the other shoe has indeed dropped in favour of different labour market drivers now versus the past versus the conventional notion that higher rates will crush everything.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.