- Canada’s economy is far outpacing expectations…

- ...in terms of both Q4 GDP and what’s baked into Q1

- Spare capacity is on track to shut earlier than the BoC guides…

- ...which may contribute toward bringing inflation toward target…

- ...and expediting unwinding of bond purchase programs…

- ...on the path toward raising the policy rate as soon as 2022

CDN GDP, m/m % change, Nov, SA:

Actual: +0.7

Scotia: +0.4

Consensus: +0.4

Prior: +0.4

December guidance: +0.3

If Canada’s economy outperformed expectations without vaccines, then just imagine how it might perform as herd immunity approaches by Fall and what that may come to mean for monetary policy.

This morning’s GDP figures continue to indicate a much stronger economy than the Bank of Canada and many private forecasters anticipated. That carries potentially strong policy implications for the Bank of Canada that is increasingly looking as if it over-committed itself to keeping rates on hold until 2023 while the TransCanada highway gets plastered with government bonds bought by the BoC.

StatsCan has tentatively guided that the economy grew by 7.8% q/q at a seasonally adjusted and annualized rate in Q4. By way of comparison, the BoC’s January MPR anticipated strong growth, but at a 4.8% clip and so it is getting a highly material beat to its expectations. So are we, as our forecast anticipated 5.4% growth.

Furthermore, based upon the way Q4 ended, the first quarter of 2021 already has 1.7% annualized GDP growth baked in before we even get any Q1 data. Here too we’re tracking better than anticipated, but much more tentatively than the Q4 tracking. The BoC’s January MPR had forecast a 2.5% contraction in Q1 GDP and so the hand-off math is tracking more than four percentages stronger. January GDP will fix some of that I suspect on restrictions, school closings and nonessential business lockdowns, but if those restrictions get eased in February—which is plausible given falling case trends—then we could not only enter Q1 better than expected but also exit Q1 better than expected. Q1 GDP still faces high uncertainty, but the new information here is more positive.

The implication is that the output gap closed more rapidly in Q4 than estimated and this reinforces expectations for overall slack in the Canadian economy to be eliminated perhaps into 2022H1 or at least a full year ahead of BoC guidance and ahead of prior forecasts shown in chart 1. With average core inflation trending around the 1.6–1.7% range and just tenths beneath the 2% target, the BoC might wind up on its inflation target or above it and sooner than it thinks.

This carries at least four policy implications. The first one concerns the BoC’s Government of Canada bond buying program. Recall that Governor Macklem guides that the GoC bond buying program will continue until the recovery is “well underway” and stop before the output gap has been shut. Two quarters of strong growth over 2020H2 into Q1 uncertainties likely doesn’t tick the definition of ‘well underway’ just yet with ongoing slack, but debate around timing the end point should be brought forward. If the gap shuts by 2022H1 then the bond buying program may end toward year-end. If so, then the BoC needs to get on with having a taper discussion with markets. I would still pencil in another taper to $3B/week from $4B at present around the April MPR and then additional tapering toward shutting down the program at year-end. The Federal Reserve would likely have the BoC’s back through the early part of this until it transitions toward taper talk perhaps by ’21H2.

Would this be a policy mistake? I don’t see it that way. It’s only a policy mistake if the BoC gets out of the bond buying business because we don’t need to stop heaping on monetary policy stimulus. It would only be a policy mistake if the economy didn’t merit tighter financial conditions. I think we’re transitioning toward the point at which we should have less stimulus. That doesn’t mean speed skating toward neutral and halting the balance sheet tomorrow. Rather, it means that the conditions will be ripe for beginning the process of experimenting with withdrawing extreme emergency levels of monetary policy stimulus ahead of what the BoC presently guides. The graffiti is on the wall over at 234 Wellington Street and the conditions are fast approaching for a 2010-style experiment to gravitate off-bottom and away from extreme emergency policy conditions with still maintaining stimulus by holding back from neutral until we have greater clarity on durability.

The second policy risk that is consistent with this viewpoint is that the BoC should likely let the Provincial Bond Purchase Program end on schedule in May after it has already ceased the mortgage and corporate bond buying programs with the latter being trivial in any event. Why?

- One main motivation for the BoC’s QE programs involved adding stimulus through nonconventional programs given the limits to conventional policy with the policy rate at ¼% and the BoC loathe to go negative. If we don’t need to be applying as much nonconventional stimulus then the PBPP should go as part of that and the incremental shift toward less easy monetary policy should first focus on QE programs.

- A second motivation was to aid market repair. Critics of the BoC’s initial foray into buying provincial bonds never thought the market was in disrepair in the first place because markets were clearing and issuance was occurring. I can’t see how they could suddenly oppose ending the PBPP now with further evidence that markets are working just fine from a consistency standpoint. The problem with programs like the PBPP is that it may be easier to overcome some resistance to their introduction than to get markets off the fix as the rationale put forth by addicted markets proves to be malleable.

- Third, the QE programs were put in place because of an anticipated liquidity withdrawal caused by soaring government issuance that required an expansion of the central bank’s balance sheet in its role as provider of liquidity. Well, today, we have considerable evidence that liquidity is in excess supply and distorting market conditions particularly with the recent developments around short-term market rates that have challenged the BoC’s ability to enforce its 0.25% policy target rate.

- Fourth, in the end, it isn’t the BoC’s job to remove price discovery in provincial government borrowing rates in absolute or relative terms. There needs to be a sound monetary policy reason for maintaining such bond buying over and above aiding investors.

Following on these comments, chart 2 shows my updated forecast for the Bank of Canada’s balance sheet through to the end of 2022. We’ve been forecasting the balance sheet throughout the QE era at the BoC and present assumptions indicate that the balance sheet will begin to materially and sustainably contract throughout 2022 after netting out all of the drivers. The level of the balance sheet is projected to remain materially larger than before the pandemic and so would excess deposits held at the BoC. This is important to understand because the outcome doesn’t point to monetary policy stimulus being withdrawn outright and back to pre-pandemic levels. The balance sheet will be a slow boat to turn but steps have to begin well in advance.

The third policy implication concerns the overnight lending rate itself. I think the prudent thing to advise heavily indebted Canadians is to plan their finances around rate hikes commencing considerably sooner than the BoC has guided even up to last week’s announcements. If slack is eliminated into next year and inflation returns closer to target, then there should be little compelling reason for why the BoC would still be sitting on such emergency levels of stimulus if the emergency has long passed. To go even further than that, as inflation risk continues to evolve away from deflation/disinflation concerns that initially motivated such massive stimulus, policy should being to acknowledge this by gradually lessening stimulus.

A fourth policy risk I’ll only allude to here merits cautioning against the ‘reset’ narrative, that this is a once in a billion year chance to ship it in and spend on curing all social and environmental challenges without any concerns about inflation. The balance of risks to that way of thinking has turned more cautious.

As for C$ concerns, today may be a good illustration of how the concerns are exaggerated. CAD only appreciated by about a quarter of a penny to the USD following the stronger than expected figures. One reason is that US data was also strong as core PCE inflation surpassed expectations. Another reason is that CAD appreciation reflects improving fundamentals and risk appetite that are contributing to expectations for tighter monetary policy sooner than previously understood. That’s likely sensible.

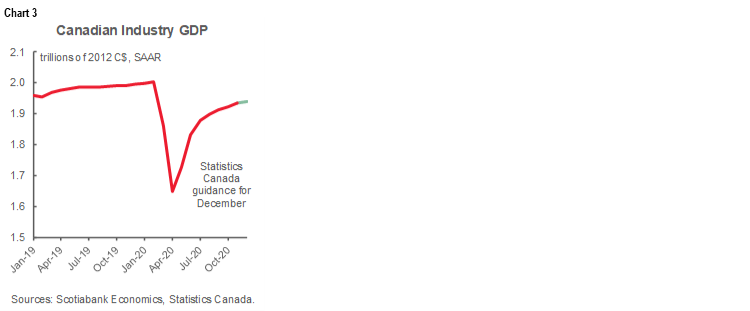

As for clean-up on the GDP numbers, I’ll let charts 3–6 do most of the talking. Chart 3 shows that of the initial 18% hit to the economy from February to April, all but 3% has been recouped in just eight months. That’s still a sizeable hit especially for any year other than a pandemic, but it is much more rapid progress.

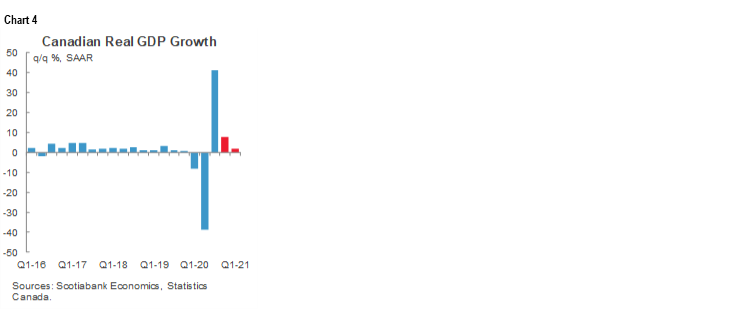

Chart 4 shows that against fears of what would happen after the initial super-charged Q3 GDP gain, the economy continues to track solid growth. It may be hard to see that on the chart because the Q2/Q3 swings swamp the scale, but Q4 at 7.8% and Q1 facing 1.7% baked in is reflective of high resilience.

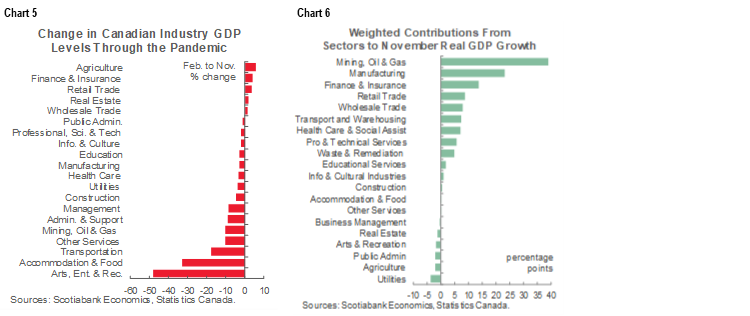

Chart 5 shows many sectors are inching closer to a full recovery up to November (we don’t have the breakdown for December). Chart 6 shows decent sector breadth in contributing to growth in November.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.