- Retail sales fell sharply in December with more weakness likely in January

- There were multiple drivers, but consumer fundamentals remain very strong

US retail sales, m/m % change headline/ex-autos, SA, December:

Actual: -1.9 / -2.3

Scotia: -0.1 / +0.1

Consensus: -0.1 / 0.1

Prior: 0.2 / 0.1 (revised from 0.3 / 0.3)

Well, that hurt. Retail sales were a big disappointment and there will probably be further weakness into at least the early part of 2022Q1 such that the soft patch is not over yet. There are nevertheless several reasons for the weakness that caution against a bearish consumer narrative set against what are otherwise solid consumer fundamentals.

WHAT HAPPENED IN DECEMBER?

First, the results. The value of retail sales in the advance estimates was down by 1.9% m/m with the ex-autos component down by -2.3% and with sales ex-autos and gas falling by 2.5% m/m.

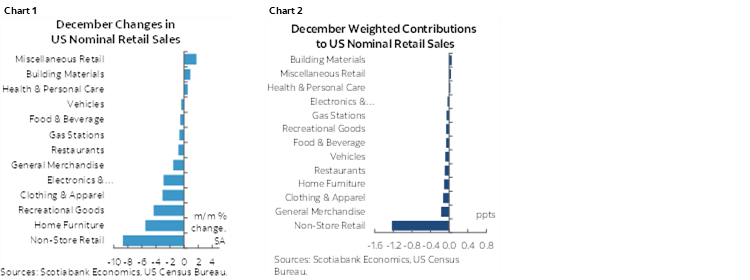

Breadth to the weakness was very high. Chart 1 shows the percentage changes by category and chart 2 does the same thing by weighting their contributions to the change in overall sales. E-sales were down 8.7% m/m and were the single biggest weighted drag on retail sales last month and so US consumers didn't even really shop from their devices. My gosh, maybe us phone addicts set the little corrupting devices aside for a moment! The softness did not stop there. Furniture/home furnishings were down 5.5%, clothing sales fell by 3.1%, sales at sporting goods and hobby stores were off by 4.3%, electronics/appliances sales fell by 2.9%, food/beverage sales were 0.5% lower and spending at restaurants and bars fell by 0.8%.

A NEVERTHELESS STRONG Q4

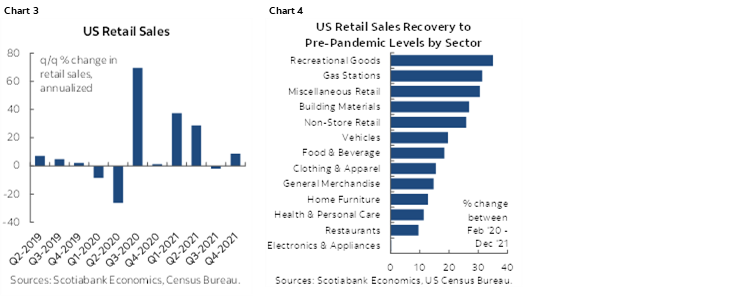

Still, for GDP purposes, the retail sales control group was up by almost 6% q/q annualized in Q4 after a 2.8% gain in Q3. sales ex-autos and gas were up 6.7% q/q SAAR in Q4 and total retail sales were up 8.7% q/q SAAR in Q4. Chart 3. Chart 4 shows that it’s still the case that retail sales have more than fully recovered from the pandemic across almost all categories.

So what gives? Sales gains appear to have been brought forward this season with October up 1.8% m/m, September up 0.7% and August up 1.2%. So, the way the monthly readings evolved around the turn of the quarter drove the Q4 gain to be solid overall even though the quarter ended poorly.

Why were sales brought forward? Possible reasons include the fact that the industry ate its own holiday lunch with sales promotions that started earlier than ever this year. Black Friday in October?? September for that matter??? Yeesh. There’s always a sale on and consumers have responded accordingly and against what may have been the industry’s wish to trick people into spending more early and throughout the peak holiday season.

WHY THE SUDDEN WEAKNESS?

But the possible reasons for softness run deeper than that.

One reason is the bare shelves argument. Inventories as a share of sales across the entire supply chain are at a record low especially in retail (chart 5).

A second reason relates to delivery bottlenecks and transportation delays. Perhaps there were enough shoppers who knew about the challenges that they'd face getting product in time into the holiday shopping season that they behaved by shopping earlier.

A third reason is the probable rotation toward spending on higher contact services as the delta variant subsided. Most of that activity is not captured in retail but will be captured in total consumption for December toward month-end. Airfare, haircuts, lodging, sporting/concert tickets etc etc are all not captured in retail.

WHERE TO FROM HERE?

I'm still of the belief that the consumer fundamentals are sound. Unfortunately, January's sales are likely to be rather poor and maybe February as well due to the omicron variant particularly on services. Online sales may pick-up in this period. My hope is that the way Q1 evolves will set up a bonanza into Q2 when winter weather and omicron both break.

1. Debt payments as a share of disposable income are at a record low back to data that began in 1980. Americans spending only 9% of their after-tax disposable income on debt payments?? They had already brought this figure lower before the pandemic and the ‘make households whole’ policies of the pandemic (as labelled by folks such as St. Louis Fed President Bullard) have pushed this figure even lower (chart 6).

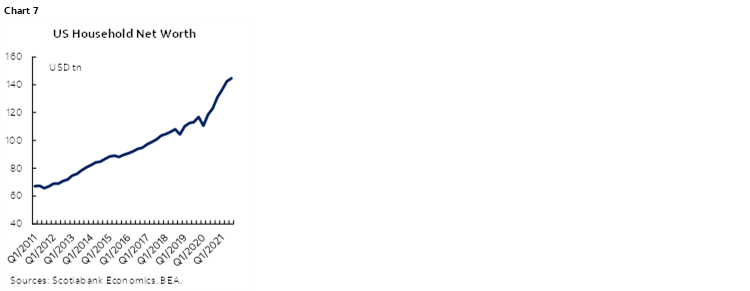

2. Net worth has been growing very strongly. No, it’s not just billionaires as Bernie, Warren and AOC would have us believe. It’s you. The homeowner. The mainstreet equity holder (chart 7).

3. Most of the stimulus cheques and accelerated child benefit payments have been stockpiled on household balance sheets. Cash and deposit holdings are up by trillions in the pandemic (chart 8).

4. We're likely at or very near (imo beyond) maximum employment. Wage gains have been picking up. Inflation is eating into wages now, but I'd expect positive real wage gains going forward plus add in benefits.

5. Overall, place the nasty data into the end of Q4 in the context of what I think is a mixed picture to read versus that still keeps alive prospects for a very positive consumer picture on a trend basis going forward.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.