- BoC holds, retains hike bias

- ‘Further and sustained’ inflation progress pushes back on H1 rate cuts

- Markets didn’t listen, 5-year yield at lowest since May

- The BoC and markets are combining to resurrect housing and fiscal imbalances...

- ...while lessening how monetary policy works to tighten through mortgage resets

- Easing now sounds great...

- ...but could well thwart prospects of more material easing later

- For real estate, it’s cash now, versus sustainability concerns

- Tomorrow’s BoC speech may be key

The Bank of Canada was hawkish mainly by using patient language toward timing rate cuts. It just wasn’t convincingly hawkish enough to markets that, left to their own devices, are on the path toward reigniting housing imbalances, tamping down how monetary policy works through mortgage resets, inflaming further government spending and driving concomitant inflationary pressures. The BoC needs to adopt a more assertive stance lest they repeat past mistakes by failing to stand in the way of a broadly based easing of financial conditions.

WHAT THEY DID

The BoC held the overnight rate at 5% as unanimously expected but mildly leaned against market pricing for early rate cuts in a statement that had a somewhat hawkish overall tone. They left QT and the balance sheet unwinding plan intact as expected. Communications are to be continued tomorrow when Deputy Governor Gravelle delivers a potentially important speech. Details will follow thoughts on how markets are managing the messaging and why the associated risks matter very much to the outlook.

HOW MARKETS RESPONDED

Markets responded by retaining unchanged cut pricing and driving a bull flattener move across the yield curve.

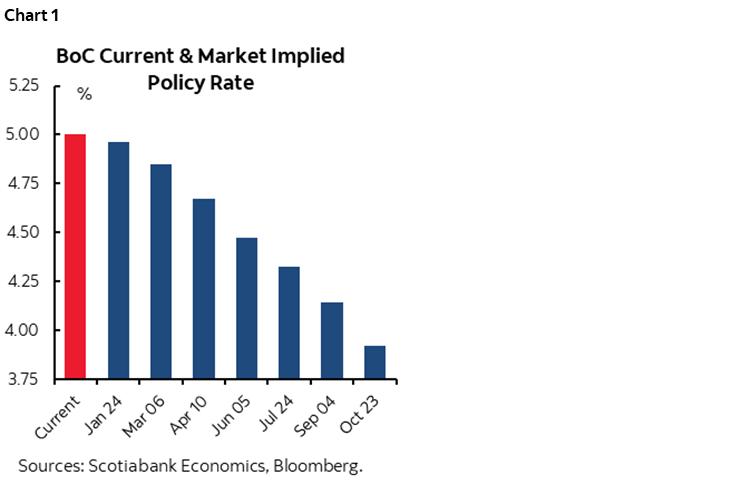

Market pricing for rate cuts was unaffected with a continued bias toward a strong probability of a cut as soon as the March meeting and more than a 25bps cut priced by the April meeting (chart 1).

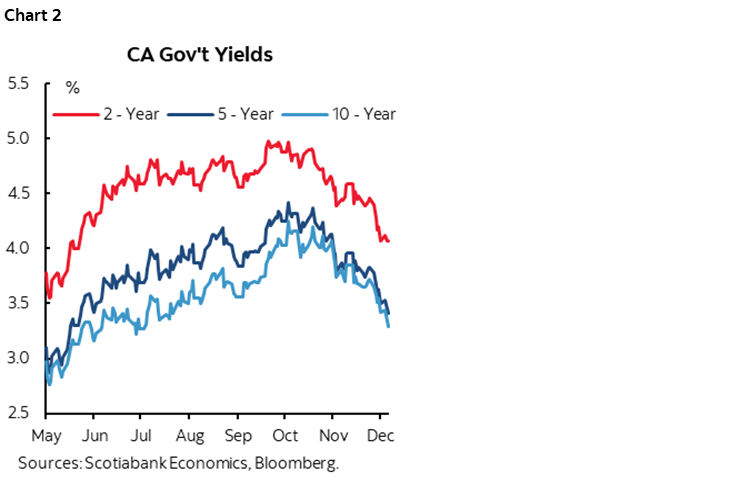

The two-year yield is flat to pre-statement levels and flat on the day. The 5-year GoC yield rallied a bit further and is now at its lowest since May 18th during the booming housing market. The Canada 10-year yield is at its lowest since late June. That matters to governments along with the rest of the curve. See chart 2.

The present yield curve is offering little term premia over reasonable assumptions about a likely higher neutral rate than the BoC has previously published (2.5%) in light of Governor Macklem’s remarks that it is likely higher now. Entirely lost is the move earlier this Fall toward steeper curves.

WHY IT MATTERS...

Should the BoC care about what markets are doing? Absolutely.

In fact, the BoC and markets are combining efforts to ignite another booming housing market, renewed macroeconomic imbalances, lessened efficacy of monetary policy working through mortgage resets, emboldening governments to spend more, and triggering spillover effects upon broader inflation.

...TO HOUSING....

Why such concern about housing? Because there is too much bearishness in relation to the facts. The five-year GoC yield is a key driver of the mortgage market given that a majority of mortgages are fixed rate mortgages and mostly 5-year fixed with the 5-year GoC yield a key driver of that. The 5-year yield is dropping on the eve of the annual seasonality in mortgage pre-approvals that begins over Winter and grants borrowers rate pledges to go shopping into the Spring housing market that is key in Canada.

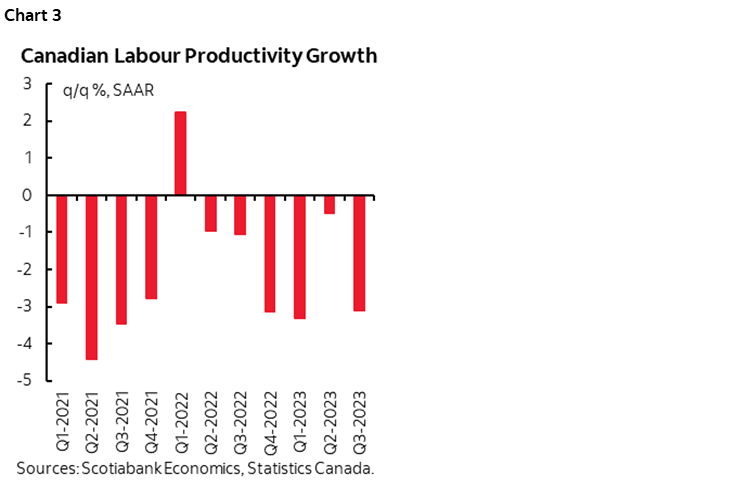

Canada has generated 430k jobs this year. Wage growth is soaring and collective bargaining agreements are cementing wage gains at rates well above the 2% inflation target for years to come. Productivity is in awful shape including this morning’s update for Q3 such that the combination of aggressive pay gains and tumbling labour productivity are adding to inflation risk (chart 3). Canadians, simply put, are getting paid more for producing less.

Canada now has two years of wildly excessive immigration relative to its ability to house them and relative to infrastructure shortfalls. The BoC’s line that immigration would contain wage pressures is a total, complete, bust.

Housing inventories are lean especially in the all-important new build segment given the need to expand the tight housing stock. First-time homebuyers have had extra time to save for a downpayment on mildly cheaper homes. Generational wealth transfers are helping with the financing.

Now we have a sustained easing of financial conditions including the key benchmark for the housing market. The BoC is at high risk of doing it again. That may please some with a bias toward maximizing near-term cash flow derived from housing and mortgage markets. I fear that much of my industry has a sky-high preference for near-term rewards; I suppose they have a high implicit discount rate on future earnings. Their incentive schemes are too skewed toward near-term outcomes. My concern remains that if we reignite pressures, then prospects for more meaningful and sustainable policy easing may be thwarted. All firms serving the housing and mortgage markets should be focused upon earnings sustainability and stability in a longer-run sense, not just the short-term which is a major reason why I lean back against people who suggest to me that a booming Spring housing market would be welcome news.

...TO MORTGAGE RESETS...

Why the concern about lessening pressures on mortgage refinancing? The five-year yield is welcome news to people who might contemplate early renewal of fixed rate mortgages and therefore push out mortgage resets to address another day. The 100bps easing in 5s from the peak, should it continue, is rapidly eroding what were often exaggerated concerns about the impact of mortgage resets in the first place and lessening one of the key ways in which monetary policy had been tightening conditions. If it continues, then the gravy trade for all those big mortgages taken out at low rates in the pandemic would be to lock and load.

...TO FISCAL POLICY...

Why such concern about government spending? The lower the cost of debt financing, the less concern about interest expense in their outlooks compared to the lagging assumptions they put in their Fall updates. If lower yields are sustained, then the Winter budget season could well inflame further increases in short-term spending. One obvious candidate is the Federal government given an election on or before October 2025 and the de facto coalition’s exceptionally poor polling. Think governments will prudently tuck away downward revisions to projected interest expense? Oh folks, folks, folks, there’s swampland out there with your name on it.

...AND TO HOPES FOR DEEPER AND SUSTAINABLE EASING

This combination of renewed potential imbalances in housing and fiscal policy plus spillover effects are being courted by a complicit BoC. Its higher for longer message and previous efforts to reach further up along the curve were not apparent in this statement. They may be tomorrow, but will markets listen to subtle, nuanced messages? Probably not; they’ve been deaf thus far. Or should the BoC take more assertive action? I lean toward the latter. The further this runs, the more credible the threat of renewed hiking becomes and while I’d rather not see that I think it’s a risk we cannot credibly dismiss. They could alternatively set the guideposts for an updated overall framework of thinking around combined balance sheet and policy rate tools which is what I’m hoping to hear tomorrow even if in nuanced fashion during the press conference or more explicitly so.

The longer the BoC distances itself from market actions, however, the more likely it is putting future easing at risk. It tends to be aloof to markets, but at the banks of the Rubicon it clearly cannot afford to be now.

STATEMENT DETAILS—HOW THEY SIGNALLED NEAR-TERM PATIENCE

Key is the concluding paragraph that sends a patient signal to markets even if it isn’t being listened to or isn’t patient enough.

Retained was the reference to a willingness to “raise the policy rate further if needed” versus some folks’ expectations that they might have struck that out. Forward guidance is therefore unchanged, and it probably cannot change at this point without triggering a further tsunami of cut bets.

The second key is in the final paragraph where they say they are “still concerned about risks to the outlook for inflation” which may be a tad softer than previously saying “progress towards price stability is slow and inflationary risks have increased.”

Third key is that they want to see “further and sustained easing in core inflation.” Further progress on core inflation says much more than just one month, and sustained says they won’t ease until they have confidence that the progress will be sustained. That’s a two-step process that requires a lot of data. This is how the BoC is trying to lean against near-term rate cuts in my view, but market participants are failing to grasp such subtleties.

It has caught the BoC’s attention that “financial conditions have also eased, with long-term interest rates unwinding some of the sharp increases seen earlier in the autumn.” Some? Have another look. Try all and then some as observed earlier in this note.

For a fuller statement comparison please see the appendix.

WHAT GRAVELLE MIGHT SAY

Today was a light, statement-only affair—and a short statement at that! The dialogue will continue tomorrow.

Deputy Governor Toni Gravelle is tasked with delivering the Economic Progress Report that customarily follows non-MPR meetings. His speech highlights will arrive at 12:35pmET tomorrow. He will host audience Q&A after reading the speech. He will then hold a press conference at about 2:10pmET.

The public guidance offered by Deputy Governors matters more under Governor Macklem than previous Governors, a point I made in this morning’s note.

Will he matter this time to markets? We’ll see, but I wrote about what may be top of mind matters for the head of the BoC’s markets and payments divisions to consider in my Global Week Ahead (here). I won’t repeat that here but stand by its contents.

If Gravelle doesn’t seize that brass ring, well, maybe today’s market actions around the BoC will be a lessen to the more powerful central banks that are on tap to make decisions next week.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.