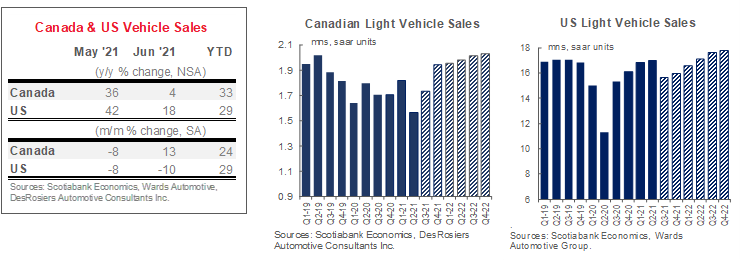

CANADA

Canadian auto sales posted only a weak rebound in June with the reopening of provincial economies as low inventory curbed purchases. DesRosiers Automotive Consultants Inc. estimates 163 k vehicles were sold—a 4% improvement relative to last year but still 12% down relative to June 2019. On a seasonally adjusted basis, sales posted an approximate 13% m/m improvement relative to May when most of the country was under lockdown, but the selling rate stood at a modest 1.65 mn saar units. This brought second quarter sales down sharply by 14% q/q (sa) following first quarter growth of 5% q/q (sa) at a solid sales rate of 1.82 mn saar units. Weak Canadian sales activity in April and May can largely be attributed to lockdowns as south-of-the-border purchases were relatively robust in early Spring despite ongoing inventory shortages. However, notwithstanding strong demand—evidenced by high price appreciation in both new and used vehicle markets—empty dealer lots likely curbed any substantial rebound in June. Inventory levels remain at historic lows as the global semiconductor chip shortage has seriously impacted North American vehicle production. While vehicle production has stabilized in June, it is only expected to start accelerating in August, according to Wards Automotive Group. But this may already be dated with Ford recently announcing further production cuts in July in a rapidly evolving environment. Otherwise, consumer health remains robust: a temporary dip in jobs under the lockdown likely saw a turn-around in June; already-elevated household savings ticked up modestly again in the first quarter (to 13%); and major purchase intentions have largely stabilized, apart from slight deteriorations under each lockdown. Rapid progress on vaccine roll-out should accelerate both confidence and consumption going forward…provided there is product to purchase. In our baseline forecast, we expect auto production to accelerate over the third and fourth quarters. Pent-up demand for new vehicles should unwind progressively to finish the year at 1.75 mn units. There is substantial downside to this outlook given the uncertainty around supply constraints, as well as competition for limited vehicles against robust American demand.

UNITED STATES

US auto sales felt the pinch of the semiconductor chip shortage with a sharp retrenchment of 10% m/m (sa) in June. Year-over-year sales were up by 18%, but, more informatively, the selling rate stood at just 15.4 mn saar units. Prior to this, April and May sales were running hotter than our annual forecast as stimulus checks spurred demand that kept second quarter sales in positive territory with a 1% q/q (sa) improvement, following the 5% q/q uptick in the first quarter. Over the second quarter, households drew down savings that had spiked to nearly 30% of disposable income in March and remained elevated at 12% by June, while a stronger-than-expected economic recovery and vaccine rollouts fueled an improvement in auto purchase intentions in June as reported by the Conference Board. Weekly jobless claims also continued to decline during June to the lowest point since the onset of the pandemic. However, limited supply clearly dampened June sales despite solid demand as inventory remains at record-lows (with an inventory-to-sales ratio hovering around 1). This will impact sales in the near term with our baseline forecasting a third quarter decline of 8% q/q before rebounding by 2% m/m (sa) in the fourth quarter to finish the year at 16.4 mn units. There is a material risk that sales will be lower if the resolution of supply constraints takes longer.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.