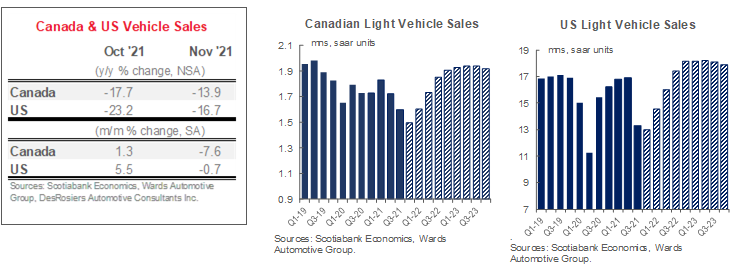

CANADA

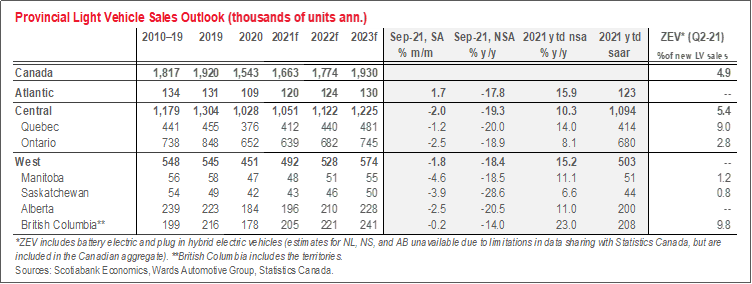

Canadian auto sales dipped in November in what has been a volatile recovery for auto sales amidst inventory challenges. DesRosiers Automotive Consultants Inc. estimated 110 k vehicles were sold at a seasonally adjusted annualised rate of just 1.45 mn units (-13.9% y/y). This works out to a -7.6% m/m (sa) decline, following October’s modest gain (1.3% m/m, sa). Recall, some monthly variability can be discounted as the shift to quarterly reporting in Canada has introduced wider margins of error. The recovery in North American auto production in November (+9% m/m, sa) offers measured hope that output will continue to improve into next year, but a host of headwinds will likely slow the pace. As Canada competes for limited inventory, days supply continues to edge lower across Canada, clearly constraining sales in an otherwise robust demand environment. Job growth may have stalled in November when numbers are published as rebound effects wane (and government programs were wound down), but the hand-off from October was strong with jobs exceeding pre-pandemic levels and robust wage gains over the past four months. Retail sales (and guidance) have surprised on the upside so far this Fall, despite supply-side constraints. Elevated household savings and still-hesitant consumer confidence suggest there is still more spending to be unwound as the economic recovery advances—and importantly when supply is available. The acute supply-demand imbalance continues to drive new vehicle price inflation: 6.1% y/y in September CPI (0.3% m/m, nsa). Our sales forecast sits at 1.67 mn, 1.77 mn, and 1.93 mn units in 2021, 2022, and 2023, respectively. While fundamental economic drivers suggest auto demand should be approaching pre-pandemic levels, auto production capacity likely limits the pace at which supply can meet this pent-up demand; consequently our projections close that gap only by 2023. There is still high uncertainty on this outlook including around the pace of auto production recovery. The emergence of the Omicron variant poses another material risk through further global supply chain disruptions while, domestically, recent weather events in British Columbia could temporarily impact the Canadian auto sector through port and rail turmoil.

UNITED STATES

US auto sales faced a setback in November as purchases pulled back by -0.7% m/m (sa), providing a reminder that the recovery will be volatile as risks still loom. Annualised sales stood at 12.9 mn units, increasing the likelihood that fourth quarter purchases will struggle to meet the 13 mn saar mark. This follows the 5.5% m/m (sa) improvement in October that sparked hopes that a rebound was finally underway. It likely still is—improving auto production in North America in November is a positive sign—but it will be bumpy. The high pricing environment and limited inventory likely took a toll on consumer confidence in November, as well as escalating COVID-19 concerns towards the end of the month. Auto purchase intentions dropped to an all-time low in November (and sharply by 2.5 ppts), according to The Conference Board, as new vehicle price appreciation reached new heights in October (9.8% y/y, nsa) for a 1.4% m/m (sa) increase. Otherwise, demand-side factors have been robust. Latest retail sales posted a healthy gain of 1.7% m/m as job growth accelerated in October, while more recent weekly jobless claims continued to trend lower through November. We have nudged down this year’s outlook to 15.0 mn units owing to this month’s weak performance and less optimism for the final month of the year. Demand is likely to continue to exceed supply through 2022. We expect sales will increase to 16.1 mn and 18.0 mn in 2022 and 2023, respectively. Further disruptions to auto production through pandemic-related supply chain factors remain a material downside risk to this outlook.

Trends in Canadian Provincial Vehicle Sales

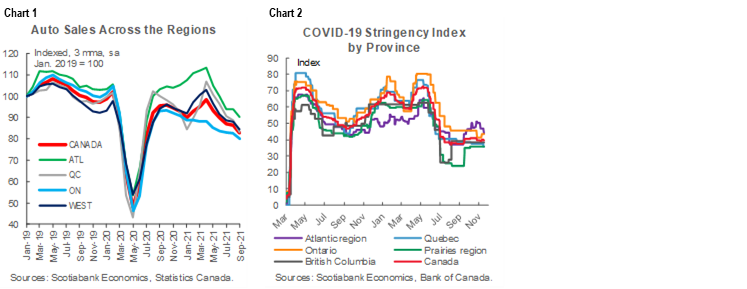

- Lagging provincial auto sales data confirm that inventory shortages curbed sales across most of the country in September. It also provides a reminder that caution is warranted (for economists at least) in relying on single-source monthly data points for auto sales in Canada given a wide range of estimates across sources (admittedly, each with a different methodology). DesRosiers Automotive Consultants Inc. had reported a -4.3% m/m (sa) decline in national auto sales for September; Wards Automotive tabulated a +1.2% m/m (sa) improvement, while recent Statistics Canada data falls somewhere in between with a -2.1% m/m (sa) dip for the month of September.

- Nevertheless, the trend decline across regions has been notable since early Spring (chart 1). Towards the end of 2020 and early 2021, there had been some notable differentiation across markets: Atlantic Canada’s auto sales recovery was less impacted by pandemic constraints via third and fourth waves (chart 2); Quebec’s shorter and less stringent lockdowns, along with robust economic fundamentals drove a surge in auto sales; Ontario’s weaker economic path—in a large part owing to larger pandemic effects—weighed more heavily on its auto sales; while Western Canadian sales were fueled by rebounding commodity prices and stronger economic fundamentals in British Columbia. However, inventory shortages have universally pulled down sales across the regions since then.

- All regions and provinces saw declines in September auto sales on a month-over-month basis except Atlantic Canada. Inventory challenges were the driving factor with Atlantic Canadian provinces posting improvements owing to double-digit declines the month-prior. On a year-to-date basis, Atlantic Canada, Quebec and British Columbia continue to perform above the national average.

- Although auto production appears to be stabilizing—if not improving—it will likely be several months before we start to see differentiation across markets based on more traditional economic drivers as limited inventory continues to put a cap on auto sales in an environment of pent-up demand.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.