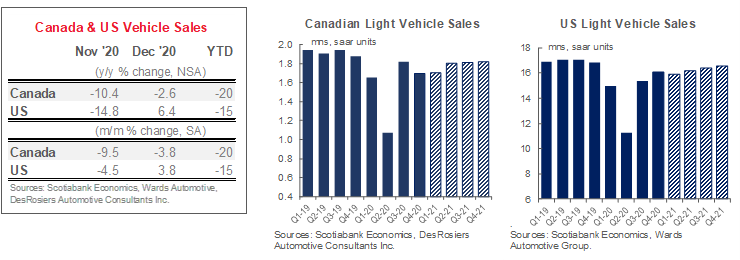

CANADA

Canadian auto sales largely held up against COVID-19 headwinds in December. Sales declined by a modest -2.6% y/y, according to DesRosiers Automotive Consultants Inc. The headline number masks the impacts of additional sales days this December relative to last year, as well as buoying base effects from depressed sales activity in December 2019. On a seasonally adjusted basis, sales were down by around -4% m/m (with caution around this indicator given only quarterly reporting by OEMs). Though mounting COVID-19 cases across most of the country necessitated more stringent lockdowns in December, dealerships stayed open (by appointment) while consumer sentiment remained resilient. In fact, the Conference Board reported a modest increase in major purchase intentions in December. Nevertheless, a broader dampening of economic activity is expected over the next quarter at least—as lockdowns are proving more stringent and enduring than originally anticipated—until vaccine distribution is ramped up substantially. Retail sales are estimated to have stalled in November following an exceptional early rebound, while consensus forecasts also expect job growth to have stalled in December. Annual auto sales finished the year at 1.54 mn units, down 20% y/y. We currently forecast a healthy rebound to 1.8 mn units in 2021, with improvements weighted towards the second half of the year once immunizations are broad-based and fleet comes back on line as travel resumes. There is some upside to this forecast, notably around stronger policy supports underpinning recoveries on both sides of the border, but also still considerable downsides related to the trajectory of the pandemic and the ability to effectively vaccinate sufficient populations in a timely manner.

UNITED STATES

US auto sales posted a stronger-than-expected month in December with a 3.8% m/m (sa) pickup in sales activity. On a year-over-year basis, a 6.4% y/y (nsa) improvement likely overstates the strength of sales activity as there was an additional weekend in December 2020 relative to last year. December’s performance is nevertheless impressive given more stringent lockdowns across many populous states as COVID-19 cases escalated to highest levels yet. The late-December USD900 bn stimulus approval likely bolstered consumer sentiment (offsetting a weakening signalled in mid-month polling by the Conference Board) with roughly half of December auto sales typically taking place after Christmas. Cox Automotive also reports a five-year record for incentive spending in December. The unemployment rate had edged downward again in November, while more timely weekly jobless claims increases in December were less pronounced than expected. December auto sales—at an annualised sales rate of 16.3 mn units—provide a solid hand-off to the new year, but sales are expected to dampen modestly early in the new year with monthly volatility to continue until vaccination efforts are well-underway. Inventory constraints are expected to hamper selection over this period with December inventory reported to be at a nine-year low, according to Wards Automotive. Annual sales for 2020 landed at 14.4 mn units, down 15% y/y. With this modestly stronger handoff to 2021, we have revised upward our 2021 sales outlook to 16.3 mn units. There is further upside to this outlook should immunizations proceed faster and if additional stimulus is provided, but also further downsides related to pandemic risks.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.