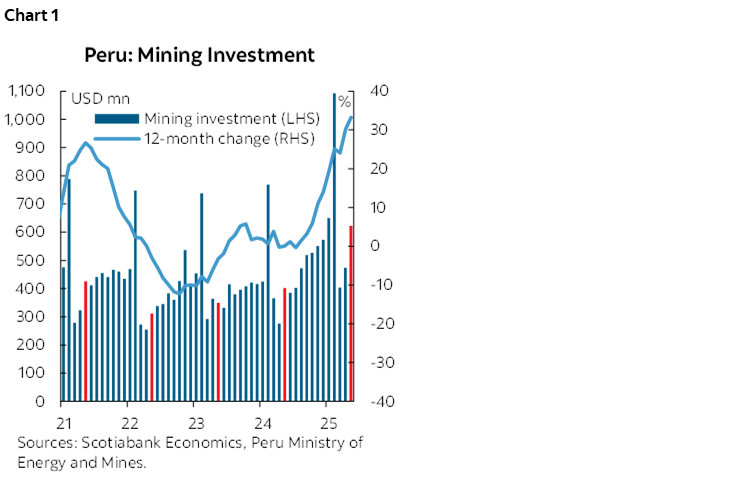

- Peru: Mining investment reached its highest first-quarter level since 2015

Mining investment totaled USD 1.5 billion in the first quarter of 2026 (chart 1), up 43.7% YoY (1Q25: USD 1.04 billion), marking the highest amount for a first quarter since 2015. The increase was mainly driven by companies with projects in the pipeline—both greenfield linked to new operations and brownfield tied to expansions, replacements and optimizations—as well as by higher sustaining and expansion capex aimed at existing operations.

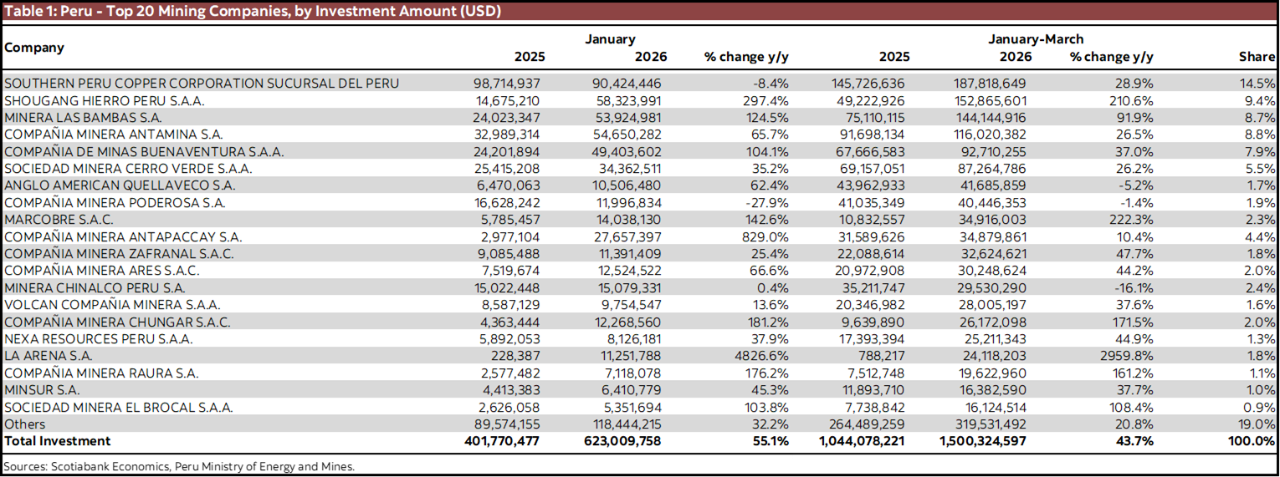

Among the leading contributors (table 1), Southern Peru (+29.9% YoY) stood out, currently advancing construction of the Tía María project, a greenfield copper development located in Arequipa, which reached 32.5% progress as of 1Q26, according to the company. Buenaventura (+37.0% YoY) also showed strong growth, supported by post-start-up capex at San Gabriel, its greenfield gold project in Moquegua. While commercial start-up had been scheduled for 1Q26, some delays occurred due to permitting.

Las Bambas (+91.9% YoY) and Cerro Verde (+26.2% YoY) also increased investment, associated with brownfield initiatives such as the Ferrobamba Replacement and Cerro Verde Optimization projects, respectively.

Shougang ranked as the second-largest investor during the period, driven by brownfield investments aimed at expanding and sustaining operations in Marcona. These include plant upgrades, infrastructure improvements and operational development. In 2025, Senace approved modifications worth around USD 327 million related to its mining unit. The company has also announced plans to extend the life of Marcona by 24 years, with an estimated investment of USD 1.82 billion covering construction, operation and closure.

Although the Ministry of Energy and Mines’ pipeline includes large greenfield projects, mining investment is currently being driven mainly by brownfield projects and sustaining capex. Tía María stands out as the main new project under execution, but most of the momentum comes from replacements, expansions, optimizations and operational improvements at existing assets, in a context of strong metal prices.

Mining production also posted a positive performance in 1Q26 (table 2), growing 1.2% YoY. At the metal level, results were mixed. Copper production increased 3.3% YoY in 1Q26, supported by higher output at Antamina (+41.7% YoY), driven by better ore grades and improved operational performance, according to the company, and at Las Bambas (+5.5% YoY), explained by improved recovery rates and higher grades from Ferrobamba. This performance partly offset declines at other operations such as Cerro Verde (−2.3% YoY), Southern Peru (−9.8% YoY) and Quellaveco (−8.2% YoY), which were affected by lower ore grades.

Zinc production also grew (+2.0% YoY), as lower output at Antamina (−19.9% YoY)—which prioritized copper and silver production over zinc zones—and at Volcan (−12.8% YoY) was offset by higher production at other operations, including Nexa Peru, Shouxin, Los Quenuales and Chinalco. Iron ore production rose as well (+1.9% YoY). In contrast, tin (−0.8% YoY), lead (−4.0% YoY) and molybdenum (−9.2% YoY) recorded declines.

Gold production fell 3.4% YoY in the first quarter. Yanacocha increased output (+37.1% YoY), supported by higher recovery through reprocessing methods in a mature stage of the mine. According to Newmont sources in May, this recovery accounts for about 44% of Yanacocha’s total gold production and 65% of its silver output, and has helped extend the mine’s life by four to five years. This contribution helped offset lower production at mines in La Libertad, such as Poderosa (−11.2% YoY), Retamas (−10.9% YoY) and Boroo (−18.5% YoY), which were affected by lower grades and the expansion of illegal mining. Silver production increased (+2.3% YoY), mainly supported by Antamina.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.