- Chile: A challenging start to the year—achieving growth above 2.5% in 2026 will require stronger private investment, full execution of public investment, and a recovery in confidence indicators

- Peru: Inflation exceeds the midpoint of the Central Bank’s target range

CHILE: A CHALLENGING START TO THE YEAR

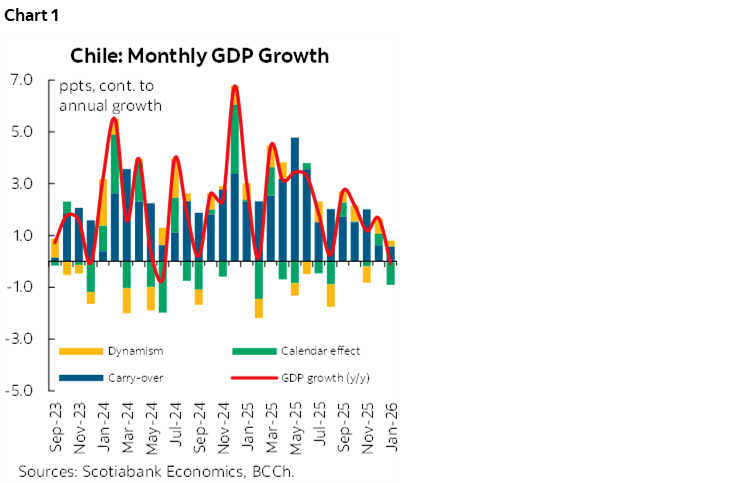

GDP contracted 0.1% y/y in January, falling short of market expectations (consensus: +1.0% y/y). This print should be analyzed jointly with December’s GDP, which had surprised to the upside due to temporary factors that appear to have reversed in January. As such, the figure does not change our baseline annual growth outlook, though it reduces the probability of scenarios with growth above 2.5% in 2026.

Excluding calendar effects, underlying activity is recovering only gradually (chart 1). January had fewer working days than a year ago, subtracting around 0.9ppts from annual growth. At the same time, weaker momentum in commerce and manufacturing, together with reversals in the “rest of goods” category, explain the flat annual growth of non-mining GDP (0.1% m/m SA).

A sharp decline in fruit exports negatively affected wholesale commerce. Reversing the strong performance seen in December, the sector made a negative contribution to total commerce, posting drops both in annual terms and on a seasonally adjusted monthly basis, led by the food industry. Similarly, agricultural and forestry activity fully unwound December’s gains, driving a m/m SA contraction in the “rest of goods” component of January GDP.

Commerce may benefit from greater liquidity beginning in February. The payment of benefits related to years of contributions and adjustments for life-expectancy differences injected more than USD 130 million per month into the economy starting in February (chart 2). Combined with the increase in the Universal Guaranteed Pension (PGU), this likely provided an additional boost to retail trade. On the investment side, machinery and equipment imports continue to grow at a solid pace, improving short‑term prospects for wholesale sales and broader economic activity.

Carry‑over for the year remains at 0.6%, meaning statistical factors make it more difficult to achieve growth above 2.5% in 2026. Moreover, weaker momentum at the margin implies the economy must grow at above‑average monthly SA rates just to reach 2.5% for the year. At Scotia we maintain our 2.5% growth forecast for 2026, supported by strong investment dynamics and a recovery in private consumption in the coming months, though we remain conservative regarding upside scenarios.

Monetary policy decision: Recent developments in the Middle East warrant particular attention from the Central Bank ahead of this month’s meeting. However, if the impacts remain concentrated in higher oil prices without spillovers to other products (food, transportation costs, or significant CLP depreciation) domestic conditions would still support a 25 bps cut, given weak employment creation, inflation below 3%, and subdued internal demand.

—Aníbal Alarcón

PERU: INFLATION EXCEEDS THE MIDPOINT OF THE CENTRAL BANK’S TARGET RANGE

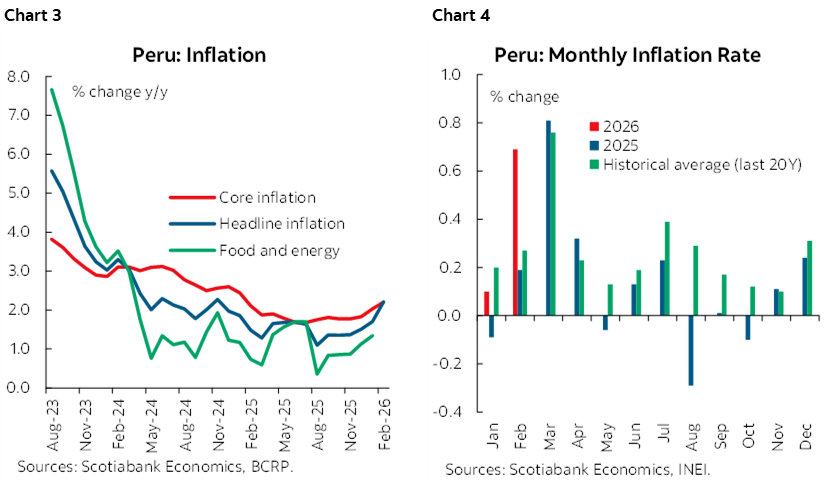

Both headline and core inflation rose in February, surpassing the midpoint of the Central Reserve Bank of Peru’s (BCRP) target range—that is, exceeding 2.0%.

Headline inflation accelerated from 1.7% in January to 2.2% in February, marking the highest annual rate since November 2024. On a monthly basis, consumer prices increased by 0.7%, above the Bloomberg market consensus of 0.3% and closer to our expectation of 0.5%. Core inflation also increased, with the annual rate rising from 2.0% in January to 2.2% in February—the highest level since January 2025.

The main driver of the inflation uptick was the category of food and non-alcoholic beverages. Within this group, there were notable price increases in chicken (+9%) and chicken eggs (+18%), both of which carry significant weight in the basic consumption basket. These price pressures have been evident since the first weeks of January and are linked to high temperatures that have reduced productivity in the poultry sector. Another product experiencing a sharp increase was peas, whose price has nearly doubled due to intense rainfall in the highlands.

These shocks are expected to be temporary and should reverse once weather conditions normalize, typically within two to three months. For March—an inflationary month due to education-related expenses—headline inflation could rise further if El Niño–related effects persist. By year-end, however, we maintain our forecast for headline inflation at 2.2%.

—Ricardo Avila

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.