- Mexico: Headline inflation slows to 3.94%, below expectations, producer prices rise to 2.98% y/y, formal employment falls by 29,922 jobs, and wholesale heavy vehicle sales jump 20.1%

- Peru: A country politically divided (almost) in half

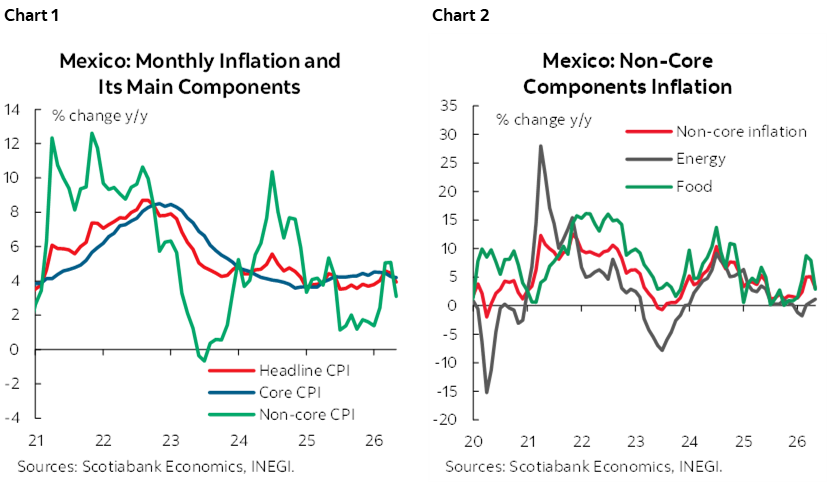

MEXICO: MAY HEADLINE INFLATION SLOWS TO 3.94%, BELOW EXPECTATIONS

In May, headline inflation surprised to the downside, falling from 4.45% to 3.94%, below the 4.03% consensus forecast (charts 1 and 2). Core inflation declined from 4.26% to 4.19%, slightly below the 4.21% consensus. Within it, goods inflation fell from 3.99% to 3.78%, while services remained under pressure and edged higher to 4.57% from the previous 4.52%. Meanwhile, non-core inflation slowed from 5.08% to 3.10% because, although fruit and vegetable prices remained elevated at 14.38%, livestock prices offset part of the pressure (-4.74%), bringing agricultural inflation to 2.90%.

Among the products with the strongest upward impact—ranked by incidence—were potatoes and other tubers, with a monthly increase of 12.8%, owner-occupied housing at 0.31%, low-cost restaurants and taquerias at 0.51%, and household gas at 2.04%. By contrast, electricity, green tomatoes, and eggs posted lower prices during the month. On a sequential monthly basis, headline inflation fell -0.21%, core inflation rose 0.22%, and non-core inflation dropped -1.65%.

MAY PRODUCER PRICES RISE TO 2.98% Y/Y

The National Producer Price Index accelerated in May, rising from an annual rate of 2.56% to 2.98%. By sector, the most notable development was a -9.33% drop in primary activities, while services increased 4.55%, up from the previous 3.98%. Within industrial activities, prices remained at 3.24%, with sharp increases in mining (32.04%) and construction (4.59%), while manufacturing (0.84%) and utilities (-0.03%) showed little change.

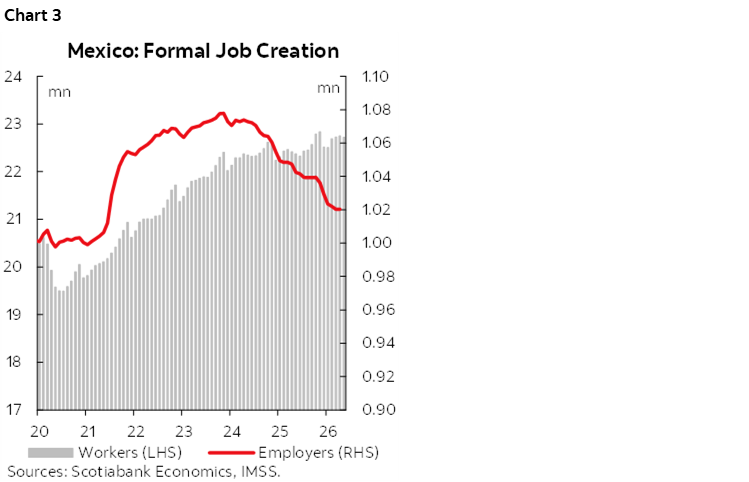

MAY FORMAL EMPLOYMENT FALLS BY 29.9KJOBS

In May, the total number of jobs registered with the IMSS recorded a monthly decline of 29,922 positions (chart 3), bringing the total to 22,718,681. According to the official release, this result was affected by a seasonal decline in temporary jobs in the agricultural sector, as well as the cancellation of a fraudulent employer registration that included individuals without a genuine employment relationship. As a result, over the past twelve months, formal employment accumulated 236,637 new jobs, equivalent to an annual growth rate of 1.5%, maintaining the same pace as the previous month and marking the strongest rate since September 2024. On the other hand, the total number of registered employers fell by 3,231, extending a streak of twenty-five consecutive months of decline and bringing the total to 1,015,999 employers, equivalent to a 2.5% decrease. Finally, the average base contribution wage stood at 671.3 pesos, equivalent to a nominal annual increase of 6.6%, maintaining the moderation trend observed since 2022.

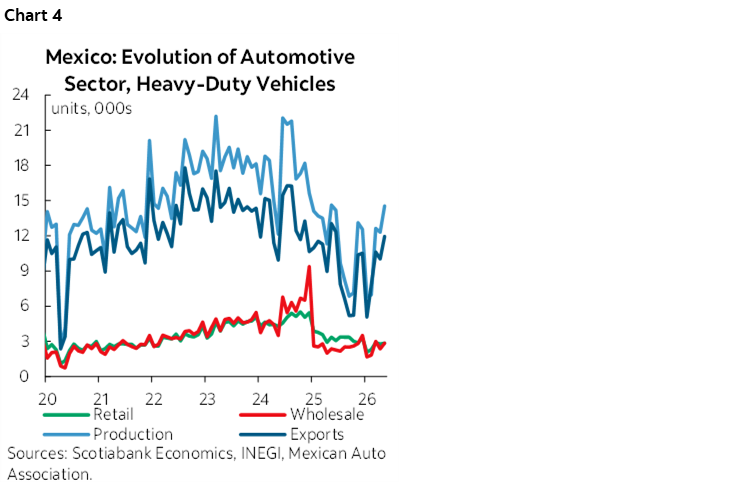

MAY WHOLESALE HEAVY VEHICLE SALES JUMP 20.1%

In May, wholesale heavy vehicle sales rebounded after fourteen negative months (chart 4), although retail sales, production, and exports remained in decline. Wholesale sales rose 20.1% year over year, while retail sales fell 15.6%. Meanwhile, production eased its contraction, declining 0.6% and extending a streak of consecutive declines since September 2024, while exports still showed a negative picture, with an 8.5% drop. On a cumulative basis, despite this month’s increase, wholesale sales averaged a 4.7% decline at 11,701 units, while retail sales averaged a 26.3% decline at 12,878 units. Likewise, production and exports posted double-digit average declines of 17.3% and 18.4%, with 55,614 and 45,530 units, respectively.

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

PERU: A COUNTRY POLITICALLY DIVIDED (ALMOST) IN HALF

Political uncertainty in Peru remains elevated following the second round of presidential elections held on June 7th, as the outcome continues to be too close to call.

According to quick counts conducted by leading polling firms, the difference between the two candidates falls within the margin of error, effectively resulting in a statistical tie. Ipsos estimates place Roberto Sánchez at 50.3% of valid votes and Keiko Fujimori at 49.7%, with a margin of error of ±1.9 percentage points, precluding a definitive result at this stage.

Preliminary official results from the National Office of Electoral Processes (ONPE), with 95.8% of ballots processed, show Sánchez with 50.07% of valid votes (8.908 million votes) and Fujimori with 49.91% (8.884 million votes). The difference—approximately 24,000 votes—is exceptionally narrow, representing less than 0.2% of total votes cast.

The remaining uncounted votes are expected to play a decisive role. Ballots from Peruvians residing abroad—historically more favourable to Fujimori—and votes from remote rural areas—typically supportive of Sánchez—have not yet been fully incorporated.

In addition, approximately 1,500 tally sheets, representing an estimated 300,000 votes, have been challenged or flagged for review. These will be assessed by electoral authorities, including Special Electoral Juries in the first instance and the National Elections Board (JNE) as the final arbiter. As a result, the official determination of the election outcome could extend until mid-July, depending on the resolution timeline of these contested ballots.

Given the extremely narrow margin and the volume of disputed votes, the final result may depend not only on the completion of vote counting but also on the JNE’s decisions. This significantly prolongs the period of political uncertainty.

Market reaction has reflected this uncertainty, albeit within relatively contained ranges. During the trading session, the Peruvian sol initially depreciated, with the exchange rate reaching S/3.52 before reversing and closing at S/3.44, below the previous session’s close. The equity market followed a similar pattern, opening with declines of up to 1.8% before recovering toward the end of the session. Sovereign bond yields also exhibited volatility, briefly incorporating a higher risk premium before retracing.

Overall, market movements suggest that investors are adjusting expectations as the probability of each candidate’s victory evolves, rather than pricing in a clear directional outcome.

In summary, Peru faces a highly polarized electoral environment, with a deeply divided electorate and an outcome that remains uncertain. The combination of a statistically tied result, unresolved votes, and a potentially prolonged adjudication process suggests that political clarity may take several weeks to materialize, maintaining short-term volatility in local financial markets.

—Pablo Nano

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.