- Chile: May CPI (0.2% m/m; 3.9% y/y) supports the monetary policy outlook

- Mexico: Automotive industry performance in May shows mixed signals

CHILE: MAY CPI (0.2% M/M; 3.9% Y/Y) SUPPORTS THE MONETARY POLICY OUTLOOK

- Limited second-round effect, with food playing a key role in the downside surprise

Chile’s CPI rose 0.2% m/m (3.9% y/y) in May, coming in well below both market expectations (Bloomberg median: 4.2%) and our forecast, driven by historically large declines in food prices. Monthly inflation was mainly explained by increases in the housing division, reflecting part of the direct pass-through from higher international fuel prices through network gas and LPG tariffs, with a combined incidence of +0.06pp. In contrast, the food division fell 0.8% m/m, subtracting 0.18pp from headline CPI. Nearly half of this negative contribution was explained by a decline in bread prices (-0.08pp), while the remainder was driven by lower prices in fruits and meats. For a May month, this drop in food prices is the most pronounced in at least the past 16 years.

Monetary Policy: weaker activity mix supports easing bias, but no near-term policy signal. From a monetary policy perspective, the activity and labour market backdrop points to a widening output gap, suggesting the need for additional monetary stimulus. The latest inflation print does not provide arguments for near-term changes in the policy rate, nor does it signal any risk of inflation de-anchoring.

However, the international backdrop continues to introduce significant volatility, which we expect to remain the main rationale for a prolonged hold. This is consistent with a scenario in which the Central Bank revises GDP growth downward in the June MPR, while keeping inflation around 4% over the policy horizon.

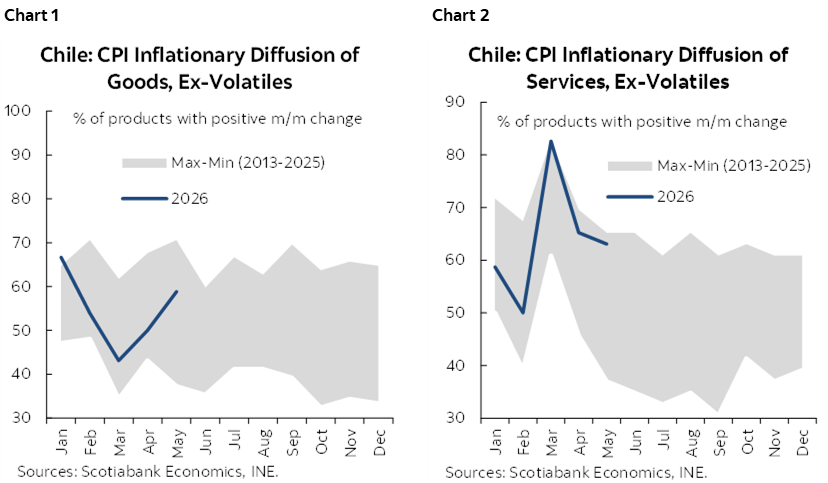

Inflation diffusion: in line with pre-Cyber Day patterns in goods, limited second-round effects in services are observed (charts 1 and 2). Inflation diffusion returned to average levels, with increases in core CPI (excluding volatile items) offset by declines in volatile components, particularly food. Goods diffusion remained elevated but within expected levels for a pre-Cyber month, consistent with patterns observed over the past two years. Services diffusion also remains in the upper range of its historical distribution, but in line with May readings in 2024 and 2025, suggesting no additional inflationary pressure. The main surprise comes from volatile items, whose diffusion has reached a two-month low. This has been driven by volatile food items, which—after three consecutive months below average—posted a historical minimum in May (lowest for any month of the year). This signals that a growing share of volatile food items is now experiencing price declines.

Food prices: historically sharp decline, led by an unprecedented drop in bread prices. Despite a significant increase in transportation costs since March, alongside higher international food prices, domestic food prices continue to decelerate, posting a historically large decline for a May print. Nearly half of the negative contribution from the Food division (-0.18pp) was explained by an unprecedented decline in bread prices (-4% m/m). This is difficult to reconcile with the current global backdrop, where international wheat prices have increased, albeit less sharply than in 2022, and remain above levels observed last year. Fuel costs—an important input in bread production—rose in April, reinforcing a cost-push environment. However, in May, despite the absence of significant fuel price declines, bread prices fell sharply, reaching their lowest level since late 2024. One possible explanation is that price-freeze announcements by major supermarket chains on selected staple goods may be playing a significant role. That said, this raises reversal risks, as the international cost environment continues to exert upward pressure on key inputs for bread production.

—Anibal Alarcón

MEXICO: AUTOMOTIVE INDUSTRY PERFORMANCE IN MAY SHOWS MIXED SIGNALS

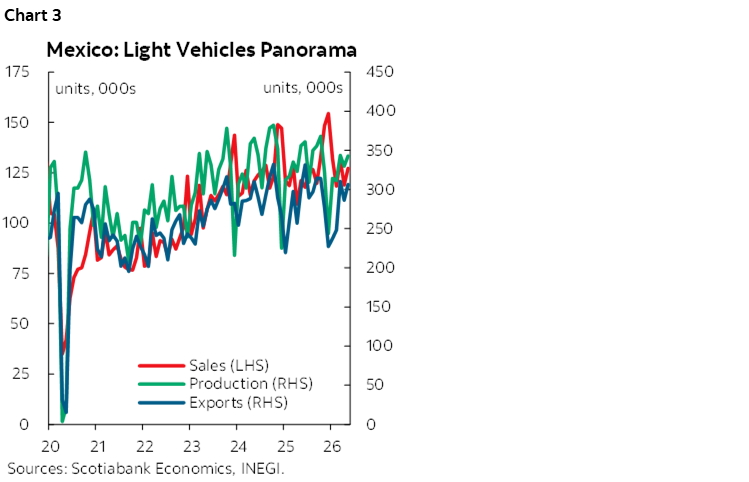

In May, the automotive sector showed mixed signals (chart 3). A total of 342,926 vehicles were produced, representing an annual decline of -3.70% (down from 2.1% previously). Meanwhile, 306,288 vehicles were exported, and 127,107 light vehicles were sold, posting annual changes of 1.74% (down from 11.4%) and 4.95% (down from 8.6%), respectively. In cumulative terms for January–March, production reached 1,642,083 vehicles, an annual variation of -0.09%; sales totaled 627,616 units, with a variation of 4.86%; and exports stood at 1,388,236 units, with an annual increase of 4.01%.

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.