- Chile: Economic activity falls 1.2% y/y in April—another negative surprise; Labour market deterioration persists

- Peru: Headline inflation declines, but core inflation shows no signs of moderation

CHILE: ECONOMIC ACTIVITY FALLS 1.2% Y/Y IN APRIL—ANOTHER NEGATIVE SURPRISE

- Growing above 1% this year becomes challenging; Central Bank likely to revise GDP growth range down to 1.25–2.0% in the June IPoM.

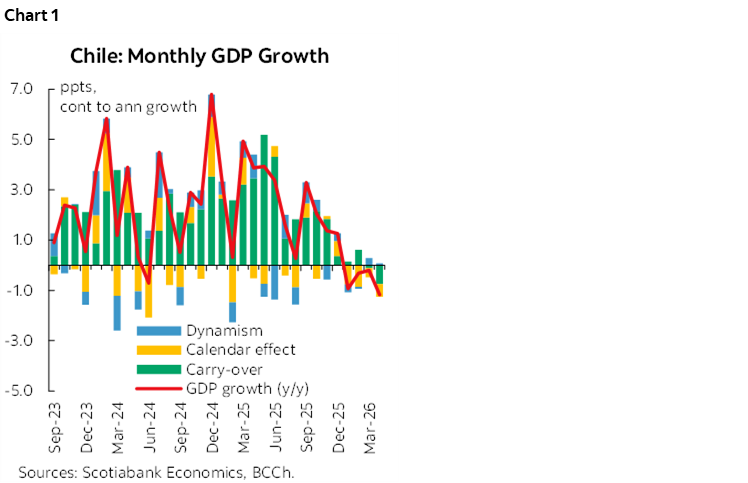

Economic activity (Imacec) contracted 1.2% y/y in April, below both survey expectations (EES: 0.1% y/y) and market consensus (Bloomberg: -0.1% y/y). By sector, a significant share of the decline was explained by mining, which fell 12% y/y and subtracted 1.5pp from overall Imacec growth. This was partially offset by still-favourable comparisons in services and commerce, despite ongoing weakness at the margin. From a statistical standpoint, seasonal factors accounted for nearly half of the annual contraction—despite no differences in working days compared to last year—while carry-over effects explained the remaining half (chart 1). This suggests that economic activity has been unable to surpass its comparison base during Q1. Indeed, excluding calendar/seasonal effects, Imacec fell 0.9% y/y, marking the largest decline in three years (since March 2023).

The statistical boost fades, with carry-over at 0% for 2026. If activity were to remain flat for the rest of the year—i.e., zero monthly growth—GDP growth would be zero in 2026. Achieving 2% growth would require a significant acceleration in coming months (around 0.7% on average in non-mining sectors), not only from mining. A downward revision in growth expectations appears unavoidable, as reaching 2% (the Central Bank’s midpoint) looks increasingly unlikely. In this context, we expect the Central Bank to revise its growth range in the upcoming MPR from 1.5–2.5% to 1.25–2.0%.

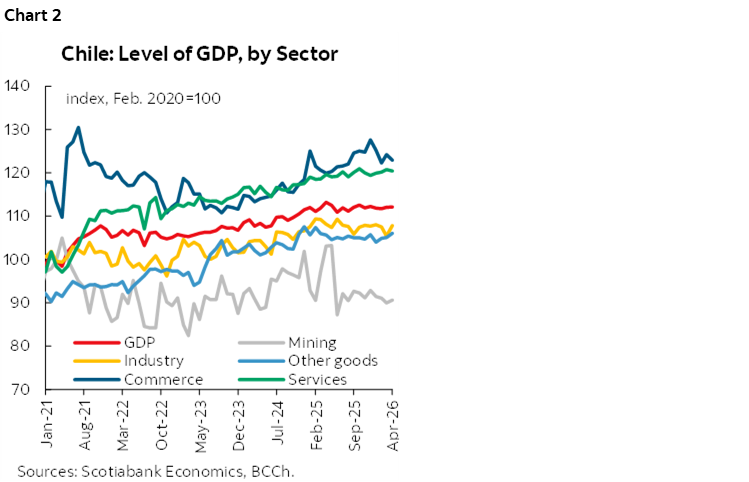

Activity remains stagnant since early 2025. So far this year, Imacec has declined by 0.1% relative to end-2025 levels, reflecting mining activity that has yet to recover production levels, alongside non-mining sectors affected by shocks in fishing and agriculture, which have also weighed on industry and commerce (chart 2). While fishing has shown early signs of recovery in some regions (mainly in the far north), El Niño poses relevant risks for activity across several sectors—including mining, industry, and agriculture—which could weigh on growth during the winter–spring period. Against a backdrop of a weak start to the year, global geopolitical uncertainty, domestic fiscal tightening, and potential adverse weather conditions, achieving growth above 1% this year has become increasingly challenging.

LABOUR MARKET DETERIORATION PERSISTS

- Seasonally adjusted unemployment rate rises to 8.9%, wage bill slows, and monetary policy trade-offs intensify

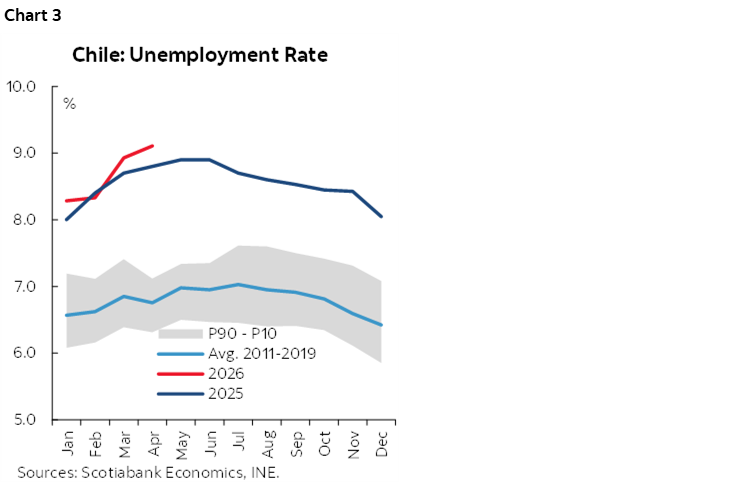

The unemployment rate reached 9.1% in the rolling quarter ending in April, above both market and our expectations (9.0%) (chart 3). Compared to the previous quarter, it increased by 0.2pp, driven by a rise in the labour force (+13k people) alongside a loss of 7k total jobs. In seasonally adjusted terms, the unemployment rate increased from 8.7% to 8.9%, with only 1.2k jobs created and a rise in the labour force of nearly 21k people. As a result, the unemployment rate remains above the Central Bank’s estimated NAIRU range (8.0–8.5%), confirming that the labour market continues to deteriorate rather than recover.

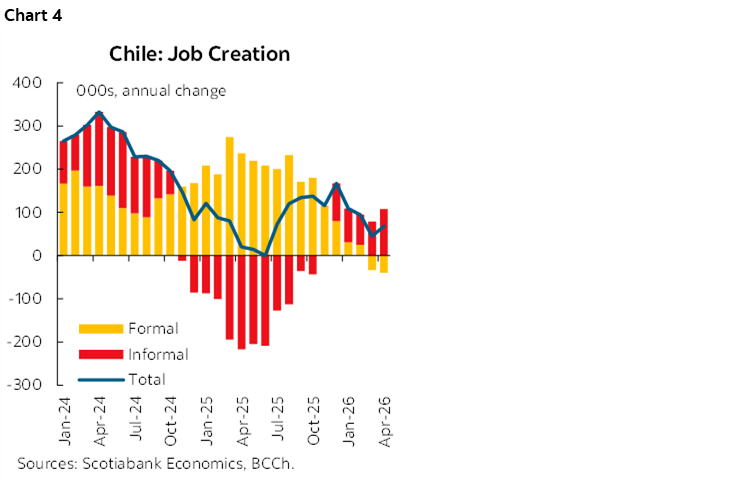

Formal job destruction persists for a second consecutive quarter (chart 4). In y/y terms, 40k formal jobs were lost, extending the negative record from the previous quarter. Notably, the labour market had not destroyed formal employment since 2021, when the pandemic was still ongoing. The weakness observed in formal employment is now spilling over into salaried employment, which fell by 10k jobs y/y—the first contraction in five years. On a monthly basis, most of the decline in private salaried jobs was concentrated in Accommodation & Food Services (-34k), while 18k public-sector salaried jobs were lost in Education.

Wage income likely posted its first contraction since the pandemic. In y/y terms, and even assuming nominal wage growth above last year’s rate for April (to be released on June 5th), the total wage bill would have grown only 0.7% y/y, showing a persistent deceleration since mid-last year.

Monetary policy faces a complex environment with opposing forces, also shaped by fiscal developments:

- The recent Q1-26 Public Finance Report suggests fiscal adjustment will be smaller than assumed in the latest MPR, implying a stronger fiscal impulse than in the baseline scenario.

- Q1 activity was disappointing—largely due to supply factors—but demand-side dynamics also lack sufficient strength to confidently signal a closing output gap.

- Annual inflation is expected to approach 5% in June, potentially triggering stronger-than-anticipated indexation effects and even signs of de-anchoring in long-term expectations across surveys and asset prices.

- The latest labour report points to a renewed deceleration in the wage bill—one of the main drivers of private consumption—while the seasonally adjusted unemployment rate continues to rise above the NAIRU range, implying a widening labour market gap. Moreover, salaried income likely contracted in y/y terms for the first time since the pandemic.

- On the fiscal front, further developments are expected on June 9th, just ahead of the June 17th IPoM release. The government will outline its fiscal convergence plan for the next four years (including 2026). This could be accompanied by additional budget cuts for 2026, reducing the implied fiscal spending growth from the Q1-26 report (+2.8% real).

All of the above leaves the Central Bank facing a challenging policy trade-off. We believe the key factor determining the next policy move—particularly whether the Central Bank opts for a 25bp rate hike—will be evidence of inflation expectations becoming unanchored. Even if activity and labour market conditions deteriorate beyond expectations and do not support a hike, the Central Bank could still be compelled to tighten policy should clear signs of de-anchoring materialize.

—Aníbal Alarcón

PERU: HEADLINE INFLATION DECLINES, BUT CORE INFLATION SHOWS NO SIGNS OF MODERATION

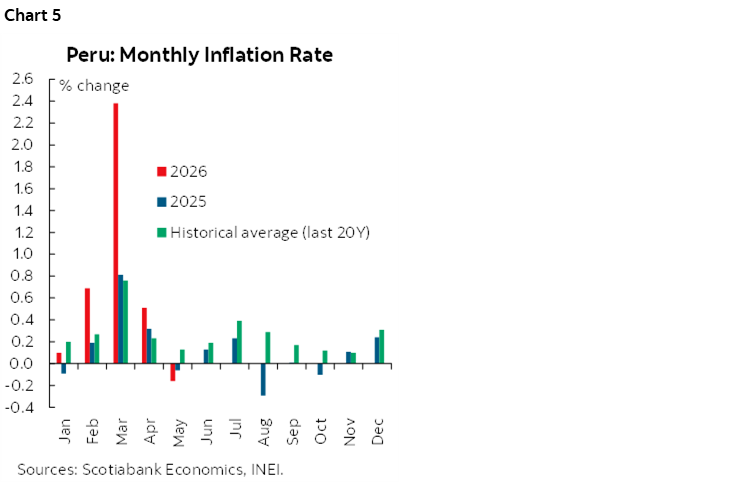

Headline inflation fell by 0.16% m/m in May (chart 5), in contrast with Bloomberg consensus expectations of a 0.06% increase. This marks the first negative monthly reading in seven months. As a result, annual inflation edged down from 4.0% in April to 3.9% in May, although it remains above the target range (1%–3%) for the third consecutive month.

In contrast, core inflation rose by 0.09% in May, pushing the annual rate up from 4.4% in April to 4.5% in May, indicating persistent pressures in non-volatile components.

At a disaggregated level, the main contributions to the headline inflation outcome came from three categories:

1. Food and non-alcoholic beverages: Prices declined by 1.7%, reflecting the easing of weather-related factors (high temperatures), which allowed for lower prices across most food items, particularly vegetables, legumes, tubers, and poultry.

2. Transportation: Prices decreased by 0.2%, driven by corrections in domestic airfares and interprovincial bus fares. However, gasoline prices recorded a marginal increase compared to previous months.

3. Housing, water, electricity, gas, and other fuels: Prices rose by 1.0%, mainly due to higher electricity tariffs (+4.2%). This increase reflects the depreciation of the local currency, as a weaker exchange rate feeds into tariff calculations and, consequently, exerts upward pressure on electricity prices.

Looking ahead, our baseline scenario assumes that international oil prices will begin to moderate during June. Under this assumption, we project inflation to decline to 3.2% by the end of 2026. Therefore, we do not expect inflation to return to the target range within this year. On the other hand, if oil prices remain elevated throughout the year, inflation would likely remain close to 4.0%.

—Ricardo Avila

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.