- Mexico: The Governing Board could pause in response to second-round effects from increasing tariffs and tax adjustments; Industrial production shows mixed signals, light vehicle production and exports end the year in negative territory, and formal employment reached 278,697 new jobs in 2025, up 1.3% year-on-year

THE GOVERNING BOARD COULD PAUSE IN RESPONSE TO SECOND-ORDER EFFECTS FROM INCREASING TARIFFS AND TAX ADJUSTMENTS

- Comments from most members in the minutes to the December 18th monetary policy meeting indicated that future monetary policy moves will depend on inflation expectations not being distorted by tax and tariff adjustments

- In the international environment, the Board highlighted that global economic activity continues to decelerate, with inflation slightly above targets and a prevailing context of high uncertainty

- Domestically, the Board noted weakness in economic activity, emphasizing the fragility of manufacturing and the automotive sector, as well as low investment, with signs of reduced dynamism in the labour market

- Regarding inflation, the Board underscored the broad-based increase across inflation components, although long-term expectations remain stable. The risks to the balance remain tilted to the upside and could delay convergence to the 3% target

- Despite a highly uncertain environment, we maintain our forecast for a year-end 2026 rate of 6.50%. Although several members’ comments suggest greater gradualism in rate cuts, we do not rule out an additional adjustment in February, contingent on continued peso appreciation, headline inflation for early January remaining within expectations, and relative monetary conditions between the U.S. and Mexico being maintained

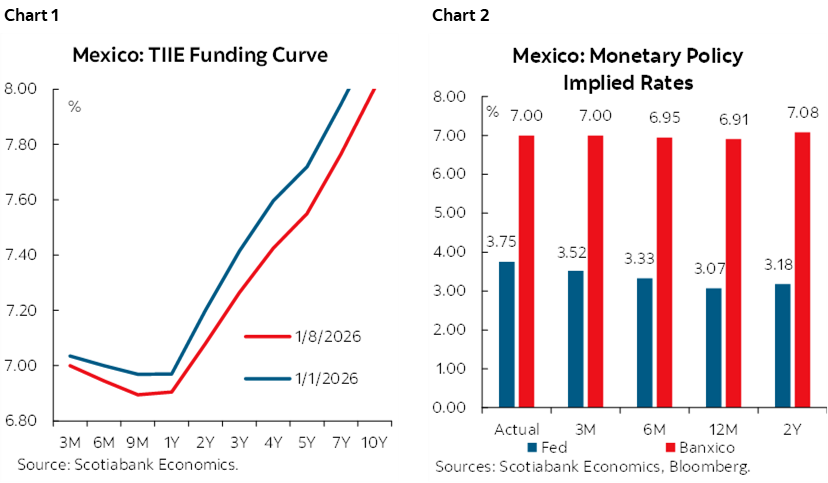

Banco de México published the minutes of the December 17th meeting, providing details on the discussion around inflation and monetary policy, with a majority decision to cut the reference rate by 25 basis points to 7.00%. Overall, we note that the Governing Board’s arguments remain focused on inflation levels, emphasizing the impact of economic weakness on prices. In this regard, despite upside risks, several members suggest continuing with a cycle of cuts, albeit with a more gradual and cautious approach throughout the year. Conversely, Deputy Governor Heath’s dissenting opinion stood out, as he considered it necessary to adjust inflation forecasts to a more credible trajectory. He also suggested keeping the rate unchanged and assessing whether the current stance is sufficient to achieve convergence to the 3.0% target, as well as evaluating the possibility of raising the policy rate if convergence cannot be achieved under the current stance.

For the international economy, they noted that in Q4 2025, the pace of economic expansion continued to moderate, pointing to a prevailing environment of elevated uncertainty due to U.S. trade policy. Inflation has remained near or slightly above central banks’ targets. They observed that the Federal Reserve cut its reference rate by 25 basis points for the third consecutive decision, while maintaining its expected rate path unchanged. Most indicated that international financial markets showed limited fluctuations, and that in most economies, interest rates along government bond yield curves increased. Finally, they highlighted that the U.S. dollar depreciated.

Regarding Mexico’s economy, they mentioned that available data suggest economic activity remained weak toward the end of 2025, with recurring stagnation reflected in the quarterly GDP decline in Q3 2025, virtually flat IGAE growth, and a clear structural slowdown compared to historical averages, with estimated annual expansion of just 0.3% for 2025. They also noted that the output gap continues to widen in negative territory, signaling growing slack, while on the supply side, persistent weakness in industrial production—particularly manufacturing and the automotive sector—was only partially offset by a limited rebound in construction and stronger performance in primary activities. On aggregate demand, investment remains on a downtrend in both public and private components, especially construction, while private consumption shows signs of losing momentum, with a greater share of imported goods and slower service consumption, without generating demand-side pressures. Manufacturing exports have been supported by computer equipment, linked to the U.S. tech sector and USMCA, offsetting the decline in automotive exports. In this sense, they point out that the balance of risks for growth remains skewed to the downside, dominated by external factors, and the labour market shows clear signs of cooling, with weak job creation, higher informality, and wage moderation, in a context where minimum wage increases could pressure labour costs in coming years.

Headline inflation rose from 3.63% to 3.80% between the first half of October and November, driven by broad-based increases in both core and non-core components. Core inflation rose from 4.24% in October to 4.43% in November, largely explained by a base effect given atypically low inflation levels in the same month last year. They also noted that the uptick in annual goods inflation was due to fewer discounts during “El Buen Fin” compared to the previous year and attributed the increase in services inflation to higher prices for services other than housing and education, particularly food services. Non-core inflation also rose, from 1.58% to 1.73%. Regarding long-term inflation expectations, they highlighted that these remained relatively stable. They mentioned that special taxes (IEPS) and tariff adjustments in 2026 are expected to have one-off, transitory effects on inflation. They also noted that the pass-through of tariff measures to prices will depend on the availability of substitutes, firms’ ability to adjust profit margins, and demand conditions. Some indicated that the balance of risks remains tilted upward and could delay convergence to the 3% target, citing factors such as public insecurity and lack of competition.

On financial markets, they mentioned that performance has been stable, influenced by both local and global factors, highlighting historically low volatility in the exchange rate. The Mexican peso appreciated significantly, reaching its strongest level of 2025, mainly due to U.S. dollar depreciation, but also supported by solid macroeconomic fundamentals, a favourable risk-adjusted rate differential, and Mexico’s relative position in trade negotiations with the U.S., which has encouraged carry trades. However, forward-looking risks persist, associated with a potential dollar correction or the USMCA renegotiation process. Government bond yields increased across most maturities in the recent period, in line with movements observed in other economies, although yields along the curve remain below mid-year levels, with stable risk premiums comparable to those of Q2 2024.

In the monetary policy discussion, most members agreed that recent inflation stability, the favourable performance of headline inflation in 2025, and the evolution of its determinants have allowed for an orderly normalization of the monetary stance, justifying an additional 25 basis point cut under a forward-looking and gradual approach. They stressed that, after overcoming the inflationary episode, current pressures mainly stem from transitory relative price shocks (associated with taxes, tariffs, and other one-off adjustments) that, in principle, do not compromise the anchoring of expectations or generate generalized pressures, in a context of economic weakness, ample slack, and currency appreciation. However, one member (presumably Deputy Governor Heath) noted the need for caution given the possibility of second-order effects, persistence in core inflation, and structural factors that could limit convergence, warning that further cuts would bring the monetary stance closer to the neutral rate without sufficient conditions to consolidate it.

In this framework, most members emphasized that the easing cycle is not over but should proceed with greater gradualism and data dependence, carefully assessing the impact of relative price adjustments and conditioning future decisions on a clearly convergent inflation trajectory toward the 3% target.

Looking ahead, based on members’ comments, we believe the likelihood of a pause has increased significantly, although we do not rule out an additional 25 basis point cut at the February meeting, contingent on continued peso appreciation, headline inflation for early January remaining within the 3% ± 1% target range, and relative monetary conditions between the U.S. and Mexico being preserved. Thus, we maintain our expectation for a terminal rate of 6.50% in 2026, although we do not rule out a year-end level above this forecast.

INDUSTRIAL PRODUCTION SHOWS MIXED SIGNALS, LIGHT VEHICLE PRODUCTION AND EXPORTS END THE YEAR IN NEGATIVE TERRITORY, AND FORMAL EMPLOYMENT REACHED 278,697 NEW JOBS IN 2025, UP 1.3% YEAR-ON-YEAR

In November, the Monthly Indicator of Industrial Activity (IMAI) showed slight upward movements in seasonally adjusted monthly terms at 0.6% and a deeper annual decline at -0.8% vs. -0.3% previously in non-seasonally adjusted figures. By component and in seasonally adjusted monthly terms, mining and the energy industry remained flat at 0.0%, while manufacturing industries posted slight increases of 0.5%. Construction rose 1.6%, continuing its positive trend for the second consecutive month. In annual terms, mining (-1.0%) and manufacturing (-2.2%) fell, while construction (3.7%) and energy (1.4%) posted gains. Year-to-date, industrial activity has accumulated an annual real variation of -1.6%, maintaining its downtrend since the beginning of the year.

Light vehicle production and exports ended the year in negative territory. In December, vehicle production moved from -8.4% to stagnation at 0.0% year-on-year, while exports eased their decline from -3.4% to -0.8%. For all of 2025, production closed with a drop of -1.3%, totaling 3.937 million units assembled, while exports fell -1.6% to 3.425 million units, both affected by an uncertain international environment and changes in U.S. trade policy.

In December, formal employment fell seasonally by 320,692 jobs, excluding platform workers, marking the smallest December decline since 2021. For all of 2025, formal job creation reached 278,697 positions registered with the IMSS, representing a 1.3% increase compared to the previous year (vs. 0.9% previously, 1.0% in December a year earlier), the strongest advance since October 2024. Meanwhile, the average base salary was 627.9 pesos per day, an annual nominal increase of 6.9%, its slowest pace since June 2021. Lastly, the total number of employers registered with social security also fell monthly by 6,839, equivalent to an annual contraction of -2.4%, in line with the economic weakness observed throughout the year.

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.