- Chile: BCCh cuts 100bps, as expected; we anticipate a cut of at least 100bps at the next meeting absent inflationary surprises

- Colombia: 2023: a positive balance for the labour market, but with some deterioration in Q4

February has started with a continuation of Fed-related losses in FX, a negative mood in rates markets, a modest rebound in wounded US equity futures, and stronger commodities. Overnight, US commercial property losses risks were highlighted by a Japanese bank after a US bank suffered steep losses yesterday on its own warnings. Eurozone inflation data came in slightly above expectations, as had been teed up by country-level data released ahead of it. The BoE’s decision at 7ET—where we expect a more neutral hold—and the 8.30ET US data run of ULC, productivity, and jobless claims figures, followed by US ISM manufacturing at 10ET are the G10 highlights today.

US equity futures are up 0.3% in SPX, and European equities are mixed. All major currencies but the JPY and KRW are registering losses vs the USD, though the MXN’s 0.2% drop represents a middle-of-the-pack performance for the peso to have it trading around ~17.25. Oil and iron ore are up about 1%, copper is flat. Yesterday’s rates market rollercoaster on US data misses, commercial property fears, and then the Fed/Powell tone swings (see our take) was followed by range-bound trading in Asia hours before a bit of a bid in the front-end in early-Europe trading... that then turned into European rates now trading well weaker cross the curve; USTs are bear steepening.

After yesterday’s BCB, BCCh (see below), and BanRep (see here) decisions, we have a couple of key releases in Latam, starting with Chilean Dec economic activity at 6.30ET, followed by Peru CPI at 10ET. Briefly, the BCB cut 50bps as expected and left guidance unchanged (meaning 50bps are coming in March and May), the BCCh cut 100bps with one member voting for a larger reduction, and BanRep opted for a smaller cut of 25bps against the 50bps cut seen by about half of economists, including us.

Our team projects that Chilean GDP grew by 0.9% y/y in December but with practically no growth on a monthly basis. Yesterday’s data were mixed, with manufacturing production surprisingly contracting year-on-year but retail sales posting a smaller-than-expected decline; commercial activity also contracted 3% y/y. Overall, Wednesday’s figures point to GDP likely undershooting our forecast.

Peru’s official journal already released headline CPI figures this morning, showing a 0.02% m/m increase in Lima prices that translates into a 3.02% y/y print. Although just shy of falling inside the 1–3% target range, this is a minor issue and the national print at 2.95% y/y already sat in the BCRP’s band (let’s see what the details deliver). While this result is slightly above our forecast of 2.9% for Lima, it is below the median’s projection of 3.16% (0.13% m/m). Continued progress into the target range with anchored inflation expectations and El Niño price risks finally fading could prompt a larger cut by the BCRP soon—though perhaps not next Thursday.

Peruvian rates markets should be supported by the print. However, they will also be weighed by the broader global rates weakness and to some degree by Fitch’s three-level rating downgrade of Petroperu yesterday, to B+ (below IG), due to the government’s lack of clear support. Next week, FinMin Contreras will announce support measures for the state-owned company.

—Juan Manuel Herrera

CHILE: BCCH CUTS 100BPS, AS EXPECTED; WE ANTICIPATE A CUT OF AT LEAST 100BPS AT THE NEXT MEETING ABSENT INFLATIONARY SURPRISES

Yesterday, the Central Bank (BCCh) cut its benchmark rate by 100 basis points (bps), to 7.25%, as we anticipated a few weeks ago and in line with the most recent market expectations. With this, the Board leaves the reference rate at the lower part of the range of the rate corridor published in the December IPoM, recognizing a new downward surprise in core and total inflation, although it maintains the validity of the interest rate corridor until the next IPoM. This decision was not unanimous, since one member was in favor of a cut below what the corridor considers (-125 bps), anticipating that the IPoM scenario would already be obsolete both in terms of inflation and interest rate and revealing concerns about falling behind the curve, with inflation well below 3%.

The new scenario for the BCCh would be very similar to the one we proposed at Scotiabank several months ago, contrary to what was expected by market consensus. Although the statement recognizes that the GDP growth scenario has been in line with what was anticipated, it is explicitly noted that total and core inflation were “below what was expected in the last IPoM”, bringing forward the convergence of inflation to the target and reducing the benchmark rate to its neutral level earlier than expected, also validating what was pointed out by one of the members a few weeks ago. This should be ratified in the April IPoM, which leads one to think that the magnitude of the cut in that month could be at least 100 bps. Certainly one of the concerns raised by the Board is the likelihood of falling behind the curve and ending up with inflation well below 3%. At Scotiabank we continue to project that inflation will reach 3% in March and we do not rule out that the benchmark rate will be at its neutral level by the middle of this year.

How do we see the next meetings? The Central Bank has meetings ahead in April, May and June, so it cannot be ruled out that the Board will quickly bring the interest rate to its neutral level. At the beginning of this process of rate cuts, at Scotiabank we proposed that, once the BCCh was convinced that inflation was decisively converging to the target, the benchmark rate would be cut quickly. After the decision, the rate is about 325 basis points above its neutral level. We estimate that, if there are no inflationary surprises in the January and February records, we could see cuts of at least 100 bps in the next meetings, which could bring the benchmark rate to its neutral level by mid-year.

Despite the recent depreciation of the CLP, the exchange rate pass-through remains limited due to the weakness of domestic demand and the adequate level of inventories. One of the conditions of this meeting was undoubtedly the depreciation of the CLP. The Board does not seem to give it much importance and only mentions the magnitude of the depreciation in its statement (6%). Our reading is that the Board would be indicating that the policy decision is not conditioned by the recent evolution of the exchange rate, contrary to what had been communicated in the October meeting when the evolution of the exchange rate affected the magnitude of the cut. Given that this depreciation has been bilateral with respect to the US dollar, that domestic demand continues to show weakness and that the level of inventories remains adequate, we consider that the exchange rate pass-through has been limited. Along these lines, we also do not expect that a maintenance of the Fed rate will have a significant impact on the next policy decisions of the BCCh, since this is incorporated into the IPoM's scenario.

—Aníbal Alarcón

COLOMBIA: 2023: A POSITIVE BALANCE FOR THE LABOUR MARKET, BUT WITH SOME DETERIORATION IN Q4

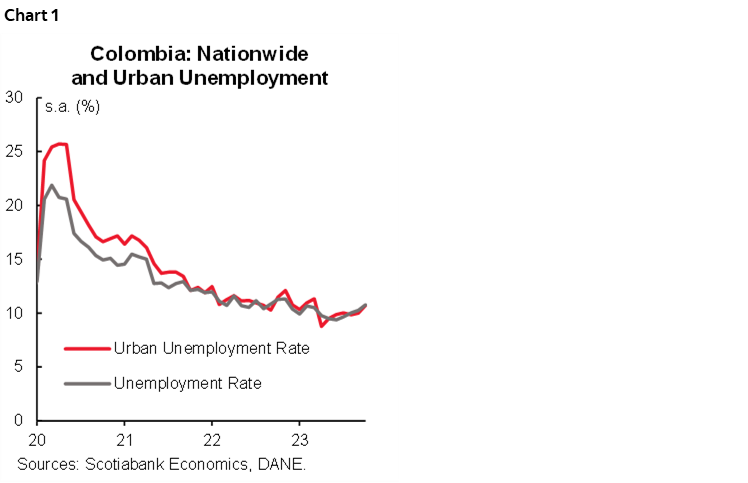

Employment data released on Wednesday, January 31st showed that the national unemployment rate in December stood at 10%, while the urban unemployment rate was 10.2%. Both figures improved compared to the December 2022 record of 10.3% and 10.8%, respectively. Thus, the average unemployment rate in 2023 stood at 10.2%, which is significantly better than the 11.2% in 2022.

In December, +396 thousand new jobs were created compared to December 2022, which were mainly concentrated in the trade and vehicle repair sector which added +319 thousand jobs, followed by professional activities which added +138 thousand new jobs. Job creation in the trade sector is classified as relevant considering that in the same month of previous years, job creation in this sector was negative with the exception of December 2019, which could suggest better dynamics in retail given lower inflation in durable and semi-durable goods, coupled with year-end festivities and related discounts.

Despite the good news for the whole year, the labour market has been deteriorating at the margin in the second half of the year. In fact, on a seasonally adjusted (SA) basis, the national unemployment rate in December stood at 10.8%, deteriorating from 10.3% in November, while the urban unemployment rate stood at 10.7%, up from 10% in November. In August, September and October, the trend showed a decrease in the number of employed people, even so, in November a change of trend was evidenced with the monthly creation of +112 thousand jobs. Despite this, December showed a reversal registering a monthly decrease of 212 thousand jobs.

The results for 2023 leave a positive balance for employment. Since July 2023, the behaviour of the unemployment rate has been in line with 2018 levels, closing with a very similar average, as in 2018 the average unemployment rate was 10%. Among other things, job creation remained positive throughout the year, with an average creation of +756 thousand jobs, with the accommodation and food services, and transportation and warehousing sectors adding the most labour to their payrolls, with an average job creation of +156 thousand and +111 thousand, respectively.

Yesterday’s employment data will provide important input for BanRep in order to fine tune the speed of the easing cycle. December figures support the idea that key sectors such as construction and manufacturing industries are not in a good shape at the moment. In December, these sectors subtracted a total of 223 mil jobs, associated with a lower dynamism in these activities. At Scotiabank Colpatria we estimate that BanRep will cut its rate to 7% by the end of 2023 (chart 1).

Key information on employment data:

- In December, the female population maintained an important participation in job creation, adding up to +222 thousand jobs, concentrated in professional activities (+135 thousand) and agricultural activities (+103 thousand). During 2023, job creation averaged +440 thousand jobs, while the average unemployment rate stood at 12.8%. As for the male population, in December they added +174 thousand jobs, with an annual average of +316 thousand jobs and an average unemployment rate of 7.9% over 2023. The unemployment gap stood at 3.8 p.p. in December, being the lowest against the same month of previous years (chart 2).

- In annual terms, +396 thousand jobs were created. The trade and vehicle repair sector added +319 thousand jobs, contributing 1.4 p.p. to the total, followed by the professional activities sector which added +138 thousand jobs adding 0.6 p.p. The manufacturing sector was the main counterpart, reducing 135 thousand jobs followed by the construction sector which added 88 thousand jobs.

- In terms of labour quality, 55% of the new jobs were in formal employment, while 26.5% were self-employed. By gender, the male population was mostly in formal employment (+171 thousand), while the female population had a higher share in the category of unpaid family workers (+94 thousand).

- The informality rate in December was 56.3%, which represents a drop of 1.1 p.p. compared to December 2022 (57.4%). In annual terms, +430 thousand jobs were added to formal employment and 33 thousand informal jobs were subtracted. In 2023, the informality rate stood at 56.4%, up from 58.0% in 2022.

—Sergio Olarte & Daniela Silva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.