- Colombia: imports stood at lowest level since May 2021 in February

- Peru: Fewer working days affect cement sales in March

Markets are reopening to ‘steady’ Israel-Iran tensions to trade with a risk-on feel into a quiet Monday following no major escalation in the conflict over the weekend. Asia trading kicked off with a rates-negative mood that is holding through a more rates-neutral Europe session ahead of a quiet G10 day. Risk-positive trading is driving a decent 0.5% rise in SPX futures is undoing about half of Friday’s steep tech-led losses, and an outperformance of high-beta FX (MXN up 0.3%) in contrast to small ranges elsewhere. Crude oil prices opened lower to sit 0.8% weaker at writing while copper and iron ore post small gains and small losses, respectively.

Mexican economic activity figures for February out at 8ET are today’s Latam data highlight. The median economist projects a 0.5% m/m expansion to correct the surprising 0.6% m/m contraction in January. The decline at the start of the year marked the fourth consecutive month of losses for the worst economic streak since summer 2021, as volatility in agricultural output combines with flatlining secondary and tertiary activity. We already know that industrial production contracted in February as extractive and construction industry activity declined against a rise in manufacturing. On the other hand, retail sales surprised with a 0.4% m/m expansion in data published Friday morning.

Data strength today would align with Dep Gov Heath’s opinion that Banxico will likely hold rates steady at the May decision (likely unanimously, according to him) as officials monitor a few more data prints. In the interview published on Saturday, Heath also said that as far as he can tell “no one is thinking of drops bigger than 25bps”. This week’s H1-Apr inflation data may shift expectations slightly for Banxico policy over the balance of 2024, though it is highly unlikely to tilt markets into expecting a May cut; as of Friday, there were only 5/6bps priced-in.

Today, Colombia’s Senate is expected to vote through Petro’s pension reform proposal to now head to a two debate rounds process in the lower house. On Friday, senators approved the inclusion of a clause allowing private fund managers to charge an up to 0.7% fee on AUMs. This may act as somewhat of a consolation prize for private managers, as an offset to expectations that, under the reform proposal, most of new pension savings would go to publicly-managed accounts.

—Juan Manuel Herrera

COLOMBIA: IMPORTS STOOD AT LOWEST LEVEL SINCE MAY 2021 IN FEBRUARY

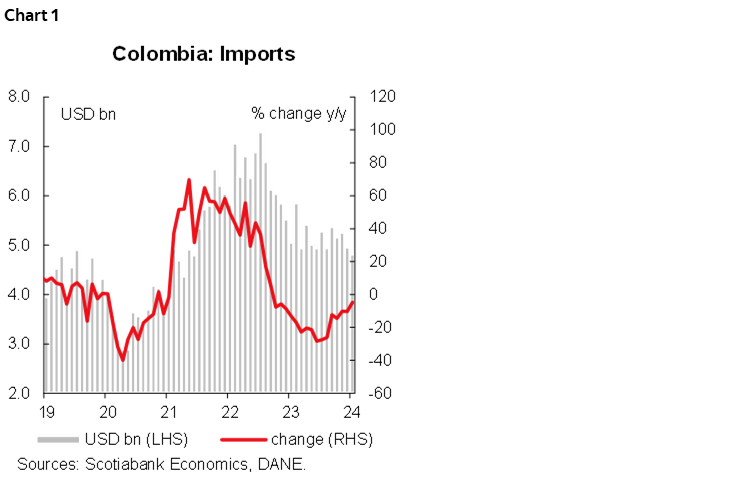

On Friday, April 19th, DANE published imports data for February 2024, which reached USD 4.82 billion CIF (chart 1), a decrease of 4.7% y/y. This is the sixteenth consecutive month of decline, however there are some signals of stabilization. Annual contraction was mainly due to a decrease in purchases from the manufacturing group of 3.7% y/y, -2.7 p.p. to the total variation. Within this group, the largest decrease was due to a fall of 9.8% and a contribution of -4.4 p.p. in the purchases of machinery and transport equipment. Fuels and products of the extractive industries decreased by 19.2% y/y, and a contribution of -2.1 p.p. to the total variation. In contrast, agriculture, food, and beverages recorded a modest growth of 0.5% y/y and a positive contribution of 0.1 p.p. to the total variation, mainly due to higher imports of oils, fats, and waxes of animal and vegetable origin (29.2% y/y), which contributed 1.8 p.p. to the variation of the group.

As for the YTD to February, Colombian imports were USD 9.78 billion CIF and recorded a contraction of 7.6% compared to the same period in 2023, and the lowest level since May 2021. By sector, imports of the manufacturing group were USD 7.38 billion CIF and decreased by 1.6%, compared to the same period in 2023, followed by the group of fuels and production of extractive industries with a decrease of -37.7%, which together contributed -6.4 p.p. to the variation. Finally, the agro-food and beverages sector contracted by 8.7% YTD to February, contributing negatively with 1.3 p.p. to the variation in this period. Nevertheless, we do not expect BanRep to accelerate the easing cycle, as our baseline scenario is for the central bank to maintain the 50bps rate cut at its next meeting on April 30th.

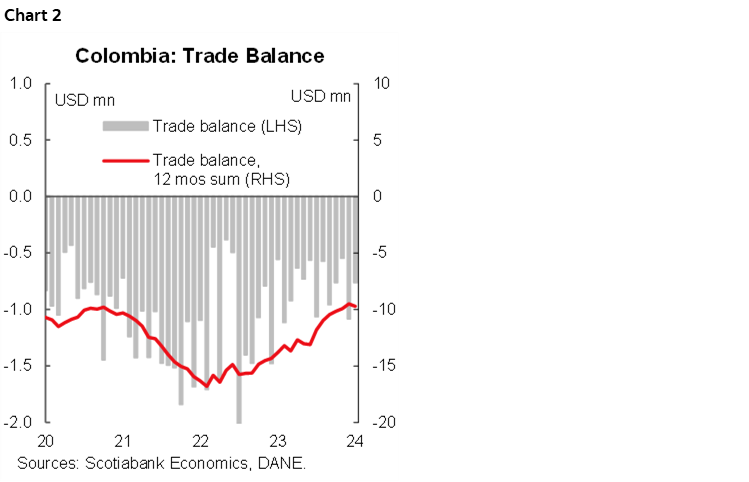

Colombia recorded an external FOB deficit of USD 762.5 million in February 2024 (chart 2), widening the gap between the end of February 2023 (USD -518.9 million), mainly due to a larger y/y decline in exports than imports. Nevertheless, the external deficit was lower in February compared to January, when it reached USD 1.08 billion FOB. In this sense, domestic demand continues to adjust to the high levels recorded after the pandemic, due to the decline in investments and consumption of durable and semi-durable goods. This pattern of weak domestic demand has manifested in a significant reduction in imports, which, together with exports, continues to justify a decrease in the real external deficit.

Recent data on economic activity and imports indicate that investment remains low, marking a discouraging start to the year, especially in sectors related to capital goods and those related to the construction sector. In addition, imports related to durable and semi-durable goods continue to be in the red due to lower household demand, reflecting the impact of high interest rates on the economy and inflation that is not anchored to its target.

Market consensus and our forecast are for a 50bps rate cut to 11.75% at BanRep’s April meeting, probably with a split vote. The board’s main concern remains the risk premiums that could be reflected in the exchange rate and delay the convergence of inflation to the target. However, economic activity and the external balance show worrying signs in some relevant sectors. We expect the central bank to accelerate the easing cycle towards the end of the year, ending at 8.25%.

Key Highlights:

- In February 2024, manufactured goods accounted for 75.3% of the total CIF value of imports, followed by agricultural products, food, and beverages at 15.2%, fuels and products of extractive industries at 9.4%, and other sectors at 0.1%.

- In February 2024, imports of manufactured goods amounted to USD 3.63 billion CIF, a decrease of 3.7% y/y and a contribution of -2.7 p.p. to the total variation. This was due to lower purchases of machinery and transport equipment (-9.8% y/y), which contributed -4.4 p.p. to the variation of the group.

- The second most important group of imports is that of agricultural products, food, and beverages, with a value of USD 732.1 million CIF, an increase of 0.5% y/y, and a contribution of 0.1 p.p. to the variation. This is explained by higher imports of animal and vegetable oils, fats, and waxes (29.2% y/y), which contributed 1.8 p.p. to the group’s variation.

- In third place are imports of fuels and products of the extractive industries, which amounted to USD 451.7 million CIF, a decrease of 19.2% y/y and contributing -2.1 p.p. to the total variation. Within this group, the product that contributed most to the decrease was petroleum and its derivatives (-31.7% y/y), which contributed -25.3 p.p. to the total variation of the group.

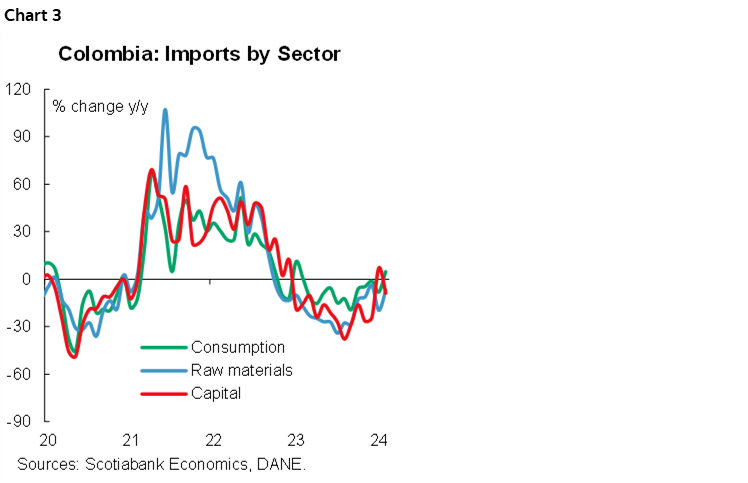

- When imports are classified by economic use or destination, two of the three main groups show negative trends (chart 3).

- Consumer goods imports reached USD 1.21 bn CIF in February 2024, down 4.8% y/y, contributing -1.1 p.p. to the total. Durable consumer goods fell by 3.4% y/y, contributing -0.4 p.p., due to the slowdown in household appliances and vehicles, which together contributed -1 p.p. to the group’s variation. However, this decline was partly offset by the positive contribution of household appliances, personal decoration, and furniture, which added 0.6 p.p.

- Non-durable consumer goods rose by 11.7% y/y in February, contributing 1.5 p.p. to the total import variation. This was mainly due to an increase in imports of food and medicine, which together added 1.7 p.p. to the group’s variation. On the other hand, beverages clothing, and textiles fell, together subtracting -0.2 p.p. from the group’s variation.

- In February 2024, imports of raw materials and intermediate goods amounted to USD 2.28 billion CIF, a decrease of 6.8% y/y and a negative contribution of -3.3 p.p. to the total variation. This decline was driven by a 22.5% annual decline in imports of fuels, lubricants, and related materials, with a negative contribution of -2.1 p.p. Imports of raw materials for industry (excluding construction) came second, with a decrease of 3.5% y/y and a negative contribution of -1.2 p.p. On the other hand, imports of raw materials for agriculture increased slightly by 0.4% y/y and contributed 0 p.p.

- In February 2024, imports of capital goods amounted to USD 1.33 bn, a decrease of 8.8% y/y and a contribution of -2.5 p.p. This decline was mainly due to the fall in imports of transport equipment (-212% y/y), building materials (-24.4% y/y), and capital goods for agriculture (-23.3% y/y), which together made a negative contribution of -2.4 p.p. to the variation in the group. Finally, imports of capital goods for industry fell by 0.6% y/y in February, contributing -0.1 p.p.

—Jackeline Piraján & Santiago Moreno

PERU: FEWER WORKING DAYS AFFECT CEMENT SALES IN MARCH

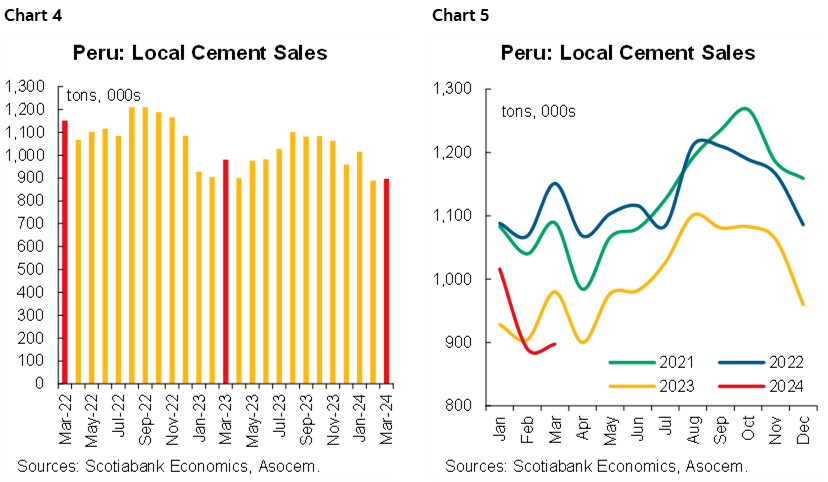

In March 2024, local sales of cement in Peru decreased by 8% YoY, as reported by the Cement Producers Association (Asocem). The sales volume, 897,400, was the second lowest since June 2020. This marks the second consecutive month of falling cement sales, following a previous drop of 2% in February.

Although the drop in sales was expected, the magnitude of the decline was higher than anticipated. Fewer working days due to the Easter holidays was the main factor causing the decline in sales of building materials at retail outlets. Excluding this effect, sales would have fallen by less than 2% YoY. Additionally, self-construction, which typically accounts for more than 50% of the cement sold in the local market, was affected by seasonal spending on education and Easter holiday travel expenses in March 2024, leading to a decrease in spending.

However, the increase in public investment of nearly 24% YoY, due to higher execution levels by the national and sub-national governments, will partially offset this decline. As a result, we estimated that the construction sector fell around 4% in March 2024. On the other hand, more working days in April 2024 than in April 2023 would have an impact on local cement sales, bringing the sector back into positive territory.

Furthermore, the gradual reduction of the central bank’s reference rate could boost the real estate market by reducing interest rates for real estate sales—especially in residential segment. This reduction in inflation expected for 2024 should improve household spending capacity, encouraging investment in the self-construction segment, considering that the price of construction materials has been progressively reducing since H2-23.

In conclusion, while the drop in sales of cement was higher than anticipated in March 2024, this decline was due to seasonal factors and the shift in the Easter holiday month. We anticipate a growth in the construction sector in the upcoming months, as its activity dropped throughout 2023. Additionally, the gradual reduction of the central bank’s reference rate could have a positive impact on the housing market.

—Carlos Asmat

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.