- Mexico: Gross fixed investment accelerated in August, with surging construction; Private consumption continues to be led by imported goods

Outside of APac markets reopening to catch up to Friday’s US moves—and in Japan to price action since Thursday—the week is starting out quietly with a small bias for paring the rates rally and lift oil prices. Equity futures are holding to the gains made while the USD is leaking lower in European trading, but the ranges are relatively small (the MXN is little changed in the mid-17s). The rest of the G-10 week is also mostly uneventful on the data front alongside the usual post-decision parade of central bank speakers (Powell on Friday).

USTs are bear flattening (2s10s down 1bp), in contrast to bear steepening EGBs (2s10s up 3bps) and gilts (2s10s up 4bps). The USD is down against all major currencies except those seeing firmer domestic rates, i.e. the JPY, AUD, and NZD, but even there the weakness is minor but notable in that the BBDXY is extending weakness below its 50-day MA (trading at lowest since Sep 20). Saudi Arabia and Russia confirmed that they would continue their supply/export cuts in December which, combined with Israel making inroads in Northern Gaza, has oil up ~1.5% in a broad commodities-positive day as iron ore rises 0.7% and copper adds about 1%. SPX futures are up 0.1/2%, partly buoyed by a Reuters report that Tesla will produce €25k cars at a Berlin factory.

The Latam day ahead, with Colombia closed today for holidays, only has the usual weekly BCB economists survey results and Brazilian S&P PMIs that generally get little attention from markets. Tomorrow may be a bit busier thanks to the release of Chilean international trade and nominal wages data, but traders should keep their powder dry on Monday and Tuesday for the release of Chilean and Colombian CPI on Wednesday, followed by Mexican inflation on Thursday ahead of Banxico (hawkish hold) and BCRP decision (neutral 25bps cut), to close the week with Brazilian prices figures and the BCCh’s economists survey. You can read more about our views for the week ahead in the Latam Weekly.

—Juan Manuel Herrera

MEXICO: GROSS FIXED INVESTMENT ACCELERATED IN AUGUST, WITH SURGING CONSTRUCTION; PRIVATE CONSUMPTION CONTINUES TO BE LED BY IMPORTED GOODS

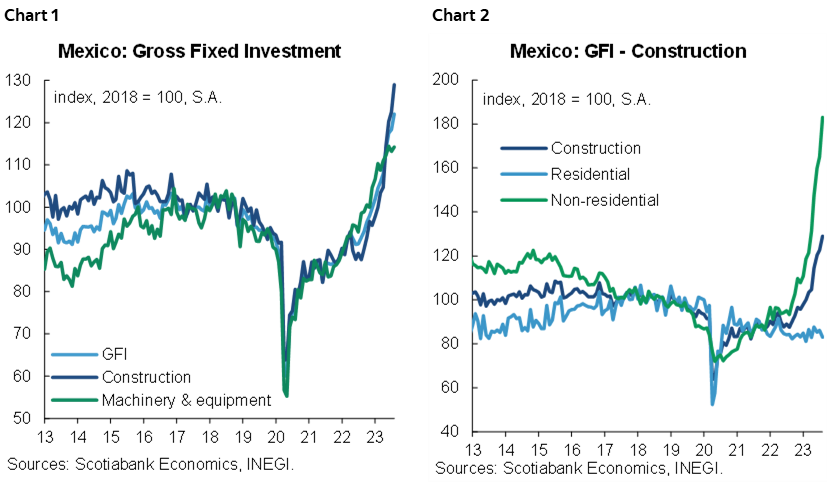

In August, gross fixed investment accelerated annually, going from 28.8% to 32.0% (chart 1). Machinery and equipment moderated 15.2% (19.8% previously), with the domestic subcomponent slowing down to 11.3% (17.5% previously) and the imported one to 17.8% (21.3% previously). Construction increased its pace to 48.1% (37.4% previously), non-residential construction increased to 99.5% y/y (71.1% previous) and residential fell -2.7% (3.5% previously) (chart2). In the seasonally adjusted monthly comparison, the GFI had a significant increase of 3.1% (0.7% previously), machinery and equipment rose 0.9% (-1.1% previously), and construction rose 5.2% (1.9% previously). Despite the annual advances, these strong increases have been supported by the change in the base year to 2018. Additionally, we highlight that the indicator has already exceeded the levels observed before the pandemic.

It should be noted that although the increase in non-residential construction is the main factor for the recent increases, the best has come from private construction (+50.0 y/y) and to a lesser extent public construction (+38.4%). On the machinery and equipment side, the pace is much lower, both in public (+15.9% y/y) and private (+0.8%).

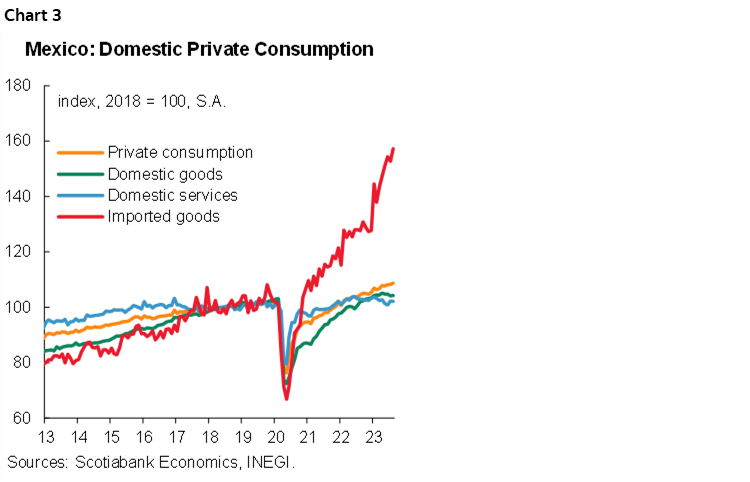

In August, private consumption slightly increased its pace in real annual terms, from 4.0% to 4.1%. Domestic goods fell -0.6% (-1.0% previously), imported goods (chart 3) increased 23.3% (19.4% previously), and domestic services moderated to 2.1% (3.0% previously). In its seasonally adjusted monthly comparison, private consumption rose 0.5% (0.1% previously), derived from the fact that services stagnated (0.0%) and imported goods increased 3.0%. The index has 30 months of consecutive increases, and what is most striking is the strength of imported goods, which could affect the trade deficit, and that domestic goods and services have not shown significant changes (chart 3 again).

We expect that both indices will continue to rise, and that the behaviour will remain the same for almost all their components, derived from the strong economic activity in 2023, which, although it slowed down in Q3, exceeded analysts’ expectations, which can be seen modified in the following surveys. In addition, consumption is not slowed down despite high rates, which could cause inflation problems.

—Brian Pérez

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.