- Peru: El Niño looms large in 2024

PERU: EL NIÑO LOOMS LARGE IN 2024

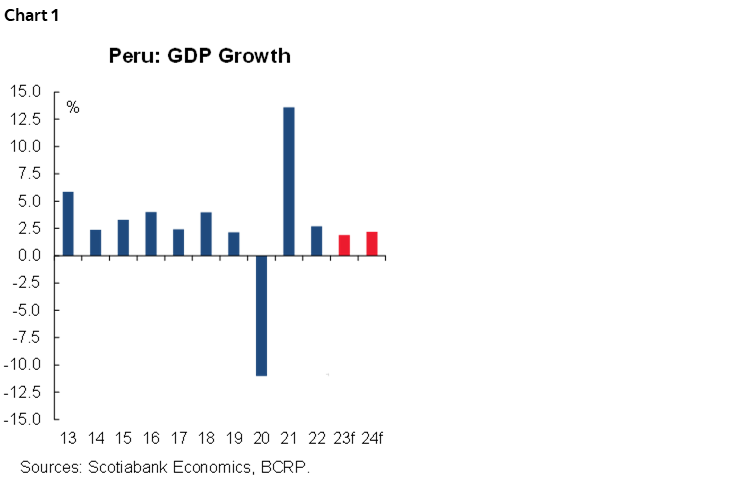

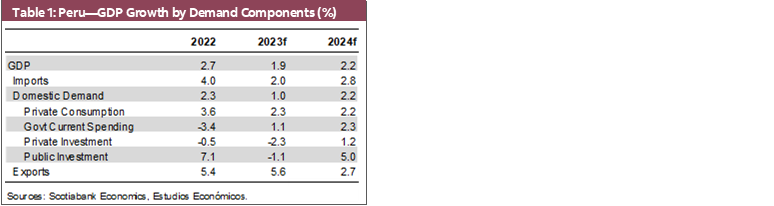

What nice Autumn weather we’re enjoying here in Lima! Therefore, beware! Offseason warmth and sunshine in Lima typically precede an El Niño event. Protests in 2023 and the likelihood of El Niño in 2024 have led us to revise our growth forecasts for both years. We are reducing our GDP growth forecasts for 2023 from 2.1% to 1.9%, and for 2024 from 2.4% to 2.2% (chart 1 and table 1).

Our forecast revision for 2019 reflects the impact of the protests on first quarter growth. GDP fell 1.2% y/y in January, which would not have happened if not for the protests. We expect a mildly less significant impact from protests in February. In March, meanwhile, rain and floods, rather than protests, will have an impact, albeit minor, on growth. Authorities at the BCRP and Ministry of Finance have suggested that Q1 2023 GDP growth will be in the vicinity of nil to 0.5%. We are inclined to agree with the BCRP’s forecast of nought growth in Q1. We had already contemplated the effect of protests when we lowered our forecast in December from 2.4% to 2.1%. However, the impact has proven to be greater than we had expected, so we are ratcheting down our forecast a bit more to 1.9%.

El Niño

Local authorities have warned that a weak El Niño is currently underway in 2023, and should last until July. This explains the heavy rains recently. At the same time, however, since we are now leaving the crucial summer months, the impact going forward this year should not be dire (except, perhaps, at a very regional level).

More importantly, the US National Oceanic and Atmospheric Administration, NOAA, gives a 60% likelihood that El Niño will take place starting in December 2023. Timing is important for Peru. An El Niño that takes place in the Southern Hemisphere winter months, as expected in 2023, does not cause the severe weather events that occur when El Niño appears in summer, which starts in December. El Niño was originally named as such because the phenomenon appeared in force around Christmas (El Niño = The Child).

In addition to the NOAA probability statistic, Peru’s offshore sea temperature patterns are tracking similar patterns in the past that were a prelude to moderate to intense El Niño years. As a result, the likelihood that El Niño will have a material impact on growth in 2024 is starting to look uncomfortably high. We are lowering our GDP growth forecast for 2024 from 2.4% to 2.2% in consideration of the likelihood of a moderate Niño. On the face of it, this might not seem like that large of a change. However, our lower forecast for 2023 produces a base effect that would normally lead us to raise our forecast for the following year. Our new forecast for 2024 carries the message that the impact of El Niño overcomes this base effect, and then some.

As a side note, in the Latam Weekly published on March 24 we had raised our inflation forecast for 2024 from 2.5% to 3.5%, on expectations of El Niño.

Our forecast of 2.2% growth for 2024 is moving a bit away from consensus, which is closer to 2.7%. As we move closer to 2024, and if the risk of El Niño persists, consensus is likely to begin to decline.

There is one final thing to consider, and that is that El Niño is, of course, a weather event. It is unpredictable in terms of intensity (or appearance at all), duration, and geographical incidence. No El Niño is like another. This means that uncertainty surrounding 2024 forecasts are high.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.