- Chile: Lower House rejects pension funds withdrawal bill. Congress must wait a year before presenting a similar initiative

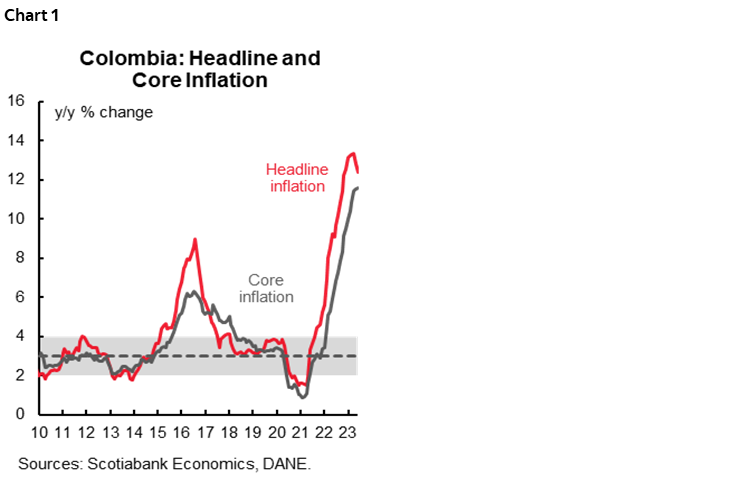

- Colombia: Headline inflation affirms downtrend, and core inflation showed stabilization signals

- Peru: BCRP to pause for the fifth straight month, awaiting more convincing signals; Lower tax revenue reflects a slow economy; Mining investment plummets in April, but not more than expected; San Gabriel and Yumpag (Buenaventura)

It’s a busy one today in Latam, but not so much elsewhere in the Americas. Before a preview of the Latam day ahead, here is a recap of the scant developments in overseas markets. Yesterday’s trends continued overnight as Asia hours provided little additional information—or at least not of enough importance to shift market-think—before European trading warmed up a bit to rates markets.

US equity futures are unchanged. The USD is overall weaker, with some commodity-sensitive currencies among the best performers (NOK, NZD, AUD up 0.5/6%) thanks to a ~2.5% strengthening of Jul iron ore futures (on China developments) that are 20% off their lows in late-May. Iron ore has gained on Chinese state-owned banks lowering deposit rates following calls from officials a few days ago. On the flip side, copper and crude oil are 0.3% and 0.5% weaker, respectively. The US and Canada day ahead have the release of weekly US jobless claims to prompt some moves in markets amid an otherwise mostly uneventful calendar until the BoC’s Dep Gov Beaudry speaks after yesterday’s surprising 25bps hike (though not for us, see here).

So, what awaits in Latam? Chilean and Mexican CPI at 8ET, and the BCRP’s rate decision at 19ET. First, another (related) intermission. On the inflation front, we got data from Brazil and Colombia yesterday.

Brazilian inflation declined to sub 4% levels in May, at 3.94%, coming in below the median projection that saw a 4.04% increase, with a 0.23% m/m increase against a consensus call of 0.33%. Gasoline and diesel price cuts and a smaller than expected increase in food prices were to blame for the ‘miss’ against relatively steady m/m gains in core prices. The still high core reading is likely enough to keep the BCB from lowering its Selic rate this month, and markets feel the same way with little in terms of cuts priced in for the June decision, but the first full 25bps cut now expected in August versus September previously. On the basis of the latest inflation print, the real policy rate is only a couple of decimal points shy of sitting in double digits—an unsustainable level of restrictiveness that may make even the hawks at the BCB uncomfortable.

In the case of Colombia, our economists provide below a full rundown of the miss in headline inflation, thanks to an important decline in food prices, which was nevertheless accompanied by a slight acceleration in core inflation. In their words “Wednesday’s results are very positive and affirm our expectation for a pause in BanRep’s hiking cycle in June, at a 13.25% level, lasting until October, when economic conditions could motivate a discussion of rate cuts.” Already, recently-appointed Fin Min Bonilla said yesterday that they “will be looking at the trend of the next two months to see if rates begin to drop”. Encouraging inflation signals as well as a stalling of President Petro’s reforms will likely remain tailwinds for Colombian assets, with the COP yesterday trading briefly below the 4,200 pesos level for the first time since last August, thanks to a ~250 pesos rally from May’s close.

Turning finally to the day’s events, the teams in Mexico City and Santiago (see more in Latam Weekly) anticipate slowdowns to 6.0% from 6.25% and 8.8% from 9.9%, respectively. Banxico seems firm in its stance of a long hold and the H1-May core reading of 7.45% (falling from 7.75%) supports this position. The bank’s meeting minutes and quarterly inflation report also add to a sense that the conversation is not about whether to hike again, but when the first rate cut could come (though the minutes were more hawkish than expected).

In Chile, stubbornly-high inflation is keeping Q2 rate cut bets at bay (by traders and economists), but the team believes that the BCCh will be ready to discuss at its June meeting the possibility of easing policy in July. Note also the slight deceleration in nominal wages growth data for April published yesterday, to a still very high 10.8% from 11.2% y/y.

For the BCRP, it’s another rate hold. Not too many fireworks are expected here, and you can read more about the factors driving the decision below, but our Lima economists believe that clearer signs of decelerating inflation in June and July CPI data will be welcome news to the BCRP that would be able to consider cuts in the fourth quarter.

—Juan Manuel Herrera

CHILE: LOWER HOUSE REJECTS PENSION FUNDS WITHDRAWAL BILL; CONGRESS MUST WAIT A YEAR BEFORE PRESENTING A SIMILAR INITIATIVE

On Wednesday, the Lower House rejected the bill that proposed the permission of a new withdrawal of pension funds, an initiative that was rejected by the House Constitution Committee last Tuesday and generated great opposition from the Central Bank and the Government. With 48 votes in favor (of the 89 required), 63 against and 3 abstentions, the plenary rejected the idea of continuing to discuss a proposal that was put forward as a way to help households to face the economic slowdown. The bill of the sixth withdrawal of pension funds will be shelved and, in addition, a decree will be put in place to prohibit the legislation of a bill of the same characteristics for one year.

—Anibal Alarcón

COLOMBIA: HEADLINE INFLATION AFFIRMS DOWNTREND, AND CORE INFLATION SHOWED STABILIZATION SIGNALS

Colombia's pace of monthly CPI inflation was 0.43% m/m in May, according to DANE data released on Wednesday, June 7. The result was again below expectations of the BanRep survey (0.61% m/m) and also below Scotiabank Economics' projection of 0.65% m/m. Food inflation was negative by 0.85% m/m, the most significant contraction since 2016 (excluding the atypical effects observed post-nationwide strikes in mid 2021). The previous dynamic is encouraging since it points out that food inflation is starting to behave more closely to the historical average, and previous shocks associated with the impact of fertilizer prices appear to vanish. It is relevant to note that although the correction on inflation comes from a volatile item (food), it also contributes to reducing the headline inflation by the end of the year, reducing the indexation effects ahead of 2024.

Year-on-year headline inflation confirmed its downward trend, from 12.84 % in April to 12.36% in May (chart 1), the lowest since October 2022. Additionally, May's data showed a new positive, and encouraging signal from core inflation metrics: ex-food inflation stood at 11.59% y/y, vs. 11.51% in the previous month, which is a more moderate increase compared with the observed in previous months, while ex-food and regulated inflation stood at 10.47%, falling from the last month's figure of 10.48% y/y. On that front, we observed that tradable goods, such as vehicles, contribute to this dynamic.

Wednesday’s results are very positive and affirm our expectation for a pause in BanRep’s hiking cycle in June, at a 13.25% level, lasting until October, when economic conditions could motivate a discussion of rate cuts. From May’s CPI result, we highlight that many ex-food items that previously showed a strong upward trend are now reaching a plateau; in fact, tradable goods ex-food are showing more moderate inflation. An offsetting effect comes from the increase in gasoline prices. However, this move is necessary to affirm the commitment to fiscal sustainability.

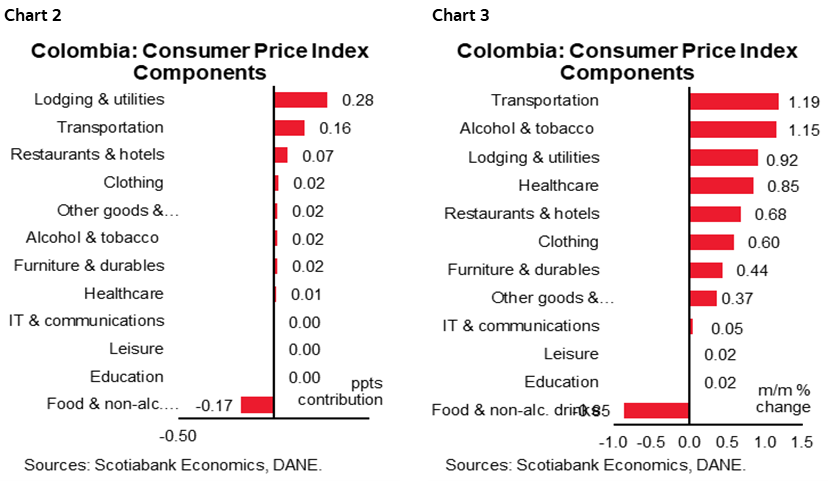

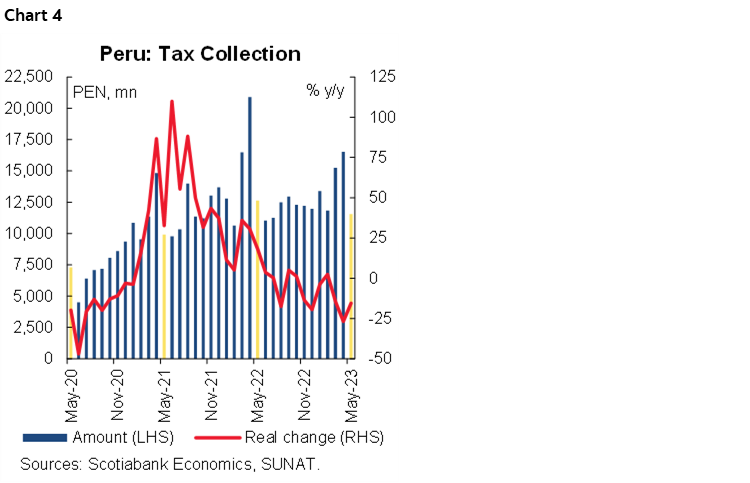

Looking at May’s numbers in detail, food inflation was the only group that showed monthly contractions (charts 2 and 3).

The highlights are:

- Foodstuff inflation posted a significant contraction (-0.85% m/m), the most substantial contraction since September 2016 (if we exclude the atypical episode after the nationwide strike in mid-2021). In May, the negative contributions came from fresh fruits (-5.80% m/m), onion (-18.07% m/m), potatoes (-8.12% m/m), and bananas (-6.10 % m/m). All show a favorable harvest cycle. However, it is worth noting that 21 food items out of the 59 references in the basket reported a m/m reduction, suggesting that atypical food inflation shocks due to external conditions, such as high input international prices, are vanishing.

- The lodging and utility group was the main contributor to the upside to monthly inflation (+0.92% m/m, and +28 bps of contribution). Rent fees continued increasing significantly (+0.92% m/m) due to indexation effects to December 2022 inflation, but probably also due to higher demand in the context of lower house sales. Utility fees increased again, however, at a more moderated pace (+0.92% m/m), with a significant contribution from water fees (+0.9% m/m) and electricity (+1.64% m/m).

- The second most significant contributor to headline inflation was the transportation group, showing a 1.19% m/m figure and a contribution of 0.16 ppts to overall inflation. Gasoline prices (+4.63% m/m), contributed 13 bps in the monthly inflation due to the 600 pesos increase; we expect this trend to continue as the government aims to reduce the potential deficit from the stabilization fund of gasoline prices, current gallon prices are at 12364 pesos and the “fair value” is estimated at around 16000 pesos. On the other side, prices of tradable items, such as vehicle prices, are decelerating. In fact, vehicle prices have shown the most modest inflation since June 2021, which partially reflects the FX appreciation effect and lower household demand.

In May, goods inflation decreased from 14.32% m/m to 14.05% m/m, signaling the moderation of food prices and some tradable items. In the case of services inflation, it increased from 8.98% y/y to 9.06% y/y, which is related to the indexation effects observed in some items that are labour intensive.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

PERU: BCRP TO PAUSE FOR THE FIFTH STRAIGHT MONTH, AWAITING MORE CONVINCING SIGNALS

We expect the BCRP’s board will leave its key rate unchanged at 7.75% at its meeting this Thursday, June 8, a move that is in line with the market consensus according to a Bloomberg survey. Year-on-year inflation fell slightly in May, in line with market expectations, while core inflation fell for the second consecutive month.

12-month inflation expectations fell from 4.25% to 4.21%, according to the latest BCRP survey, a decline still without conviction, still well above the target range (between 1% and 3%). The survey also showed that 24-month inflation expectations rose from 2.89% to 3.13%, reflecting that the consensus still sees inflation returning to the target range could take longer. This perception is in line with recent statements made by Velarde—BCRP’s governor—regarding the fact that inflation will reach the target later than expected because inflation has been slowly declining. This opens the possibility that the BCRP no longer expects inflation to return to the target range in 4Q-2023—as it has been maintaining up to now—but rather that it will do so in 2024. This would be a novelty if it is incorporated into tomorrow's statement.

Business expectations improved in May in relation to April but remain in a pessimistic zone. The economic indicators have not been recovering as expected. For June, we expect a more visible decline in inflation, with the possibility that it may even be below the average of the last 20 years (0.17%), since we see a significant correction in poultry prices, which would be reflecting that the effects of bird flu are dissipating, to which would lower prices of local fuels. With this, we expect inflation to be close to or even below 7% in June. Our inflation forecast remains at 5.00% for 2023. The BCRP expects food prices to drop in the remainder of the year, which would help lower inflation. The BCRP president has also been wary of cutting interest rates too soon.

—Mario Guerrero

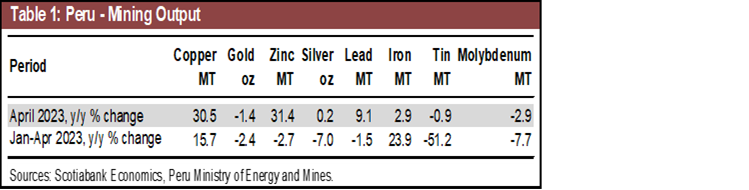

LOWER TAX REVENUE REFLECTS A SLOW ECONOMY

Tax revenue fell 15.4% y/y in May, completing three consecutive months of decline, according to figures from SUNAT. Although the magnitude of the decline was less than in April (see chart 4), the result was worse than we were expecting. This ratifies the fact that domestic demand is not picking up speed at the rate we were expecting, after suffering the ravages of social protests in the south and heavy rains in the north during 1Q23.

With May’s result, tax revenue accumulated a 13.7% decline during the first five months of 2023. In addition to low domestic demand, factors such as the lower coefficients used to determine the monthly payment of Income Tax, the temporary reduction of the general sales tax (IGV in Spanish) for small businesses in the hospitality and restaurant sectors, and the postponement of payments by companies located in areas declared in a state of emergency (due to social protests and heavy rains), contributed to poor revenue. We expect most of these factors to continue in the following months. This will affect our projections for the public sector, so our current projection of a fiscal deficit of 2.0% of GDP for 2023 has an upward (greater deficit) bias.

Of particular note in May was the 9.3% y/y decline in the General Sales Tax (IGV). May was the seventh consecutive month in which it declined. The tax for May is based on April sales and points to modest economic growth for the month. In fact, April's GDP would be below our initial growth estimate of 1.5% y/y, while domestic demand would not show a very different result to the -2.9% reported in March.

Meanwhile, Income Tax (-16.7%) was basically affected by lower payments on account of companies (-31.2%), especially in the mining sectors—affected by the drop in metal prices—trade and manufacturing. Finally, one of the few taxes that showed a positive result was the Selective Consumption Tax-ISC (+14.9%), benefiting from a base effect since between May and July 2022. Gasoline and diesel were temporarily excluded from the payment of this tax to fight rising inflation.

—Pablo Nano

MINING INVESTMENT PLUMMETS IN APRIL, BUT NOT MORE THAN EXPECTED

Local mining investment fell 19.0% y/y in April, according to data from the Ministry of Mining. Mining investment over January–April accumulated a 19.2% y/y, decline, in line with the -19.1% growth that we had in our forecasts. Lower investment continues to be linked to the completion of the construction of the Quellaveco mine (Anglo American) in 2022, which is being minimally offset by minor projects that were already under construction in previous years. To date in 2023, there has been no construction activity on any new mining projects placed on the 2023 pipeline.

The company that led in mining investment in April was Antamina. The company is still waiting for the approval of the Modification of the Modified Environmental Impact Study (MEIA-d), which it expects to obtain by mid 2023. This brownfield project is intended to give continuity to the operations of the Antamina mine and extend operations until the year 2036. The other three projects that have not started operations yet are Romina and Magistral (due to lack of EIA approval) and Corani (in limbo due to the social protests at the beginning of the year). Other companies that led in investment included Anglo American and Southern Peru.

SAN GABRIEL AND YUMPAG (BUENAVENTURA)

The San Gabriel project is currently under construction. According to Buenaventura, in May it reached total progress of 15% and currently, the mining company continues to search for financing. In addition, Buenaventura is also looking at different options to finance its small Yumpag project (US$81 million), which aims to extend the life of the Uchucchacua mine for another 15 years. Buenaventura plans to invest between US$350 and US$360 million this year, of which US$190 million will be for San Gabriel, and close to US$50 million for the development of the Yumpag project (Pasco).

On the other hand, a better performance was seen in the mining output. Output increases in most metals, except for gold, tin, and molybdenum (see table 1).

Copper output increased 31.5% in April, basically for two main reasons. The first was the start of operations of Quellaveco—in September 2022—and the second was the stoppage of operations for more than 50 days in Cuajone (Southern) and Las Bambas last year because of social protests. On the other hand, zinc output also stood out, which increased 31.4% in April, due to record increases in output by Antamina and Volcan due to higher ore grades.

—Katherine Salazar

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.