- The BoC raised its overnight rate by 25bps...

- ...as a minority including Scotia Economics expected

- The bias leaves the door open to doing more...

- ...and tentatively favours another 25bps in July

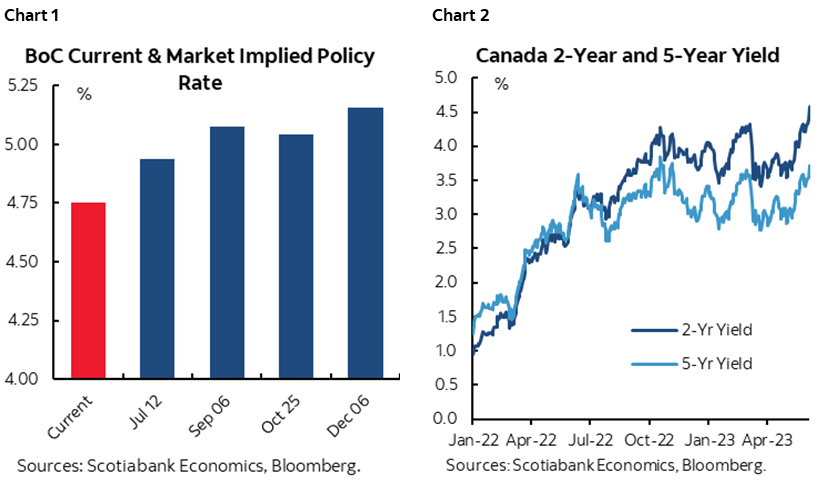

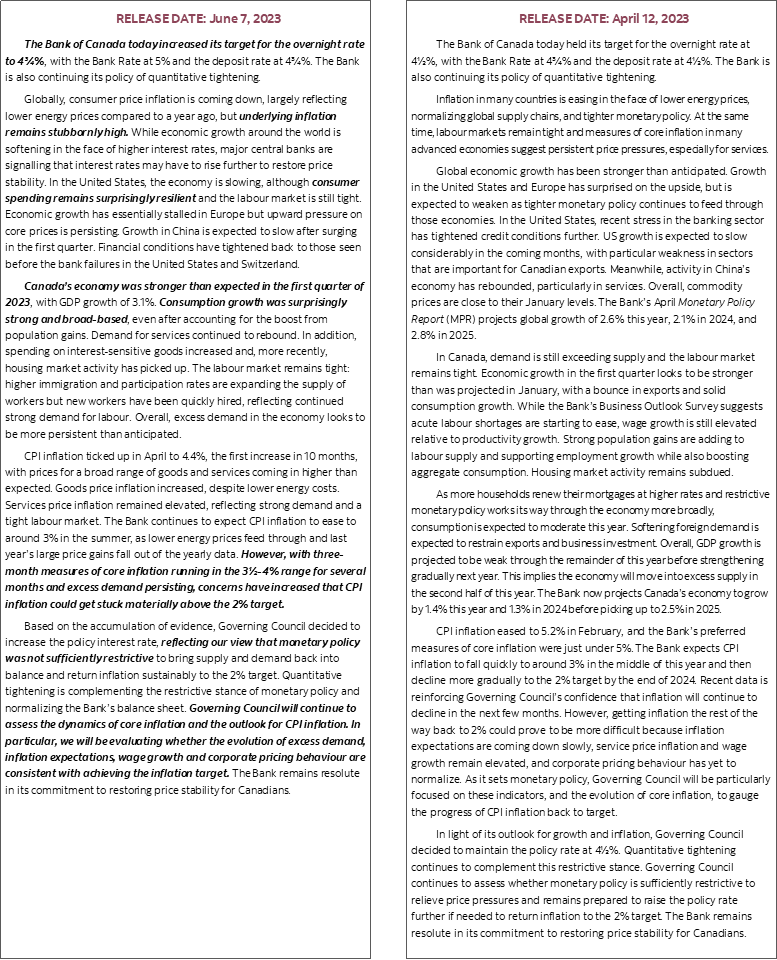

The Bank of Canada hiked its overnight rate by 25bps to 4.75% as forecast by Scotia Economics. This was a surprise to markets and so the Canada two-year yield jumped by 21bps post-statement while the C$ appreciated by half a penny at first before reining in some of that reaction because the BoC decision hit US short-term rates. The US two-year yield jumped by 7bps while raising the probability of another Fed hike on the logic that multiple central banks are not done yet. July is priced for another 25bps BoC hike.

Markets had gone up to the 10amET statement pricing less than 50% odds of a hike and only 8 out of the rather generously defined consensus pool of 37 forecasters anticipated the hike. Scotia Economics led all of this consensus with guidance that the front-end was overly dear back in March and April and for months has guided toward renewed hike risk into the summer months. Go Team Scotia, and kudos to the competition for strengthening the quality of the debate with views from all sides. I think the BoC did the right thing and hats off to the Governor and Governing Council for doing what’s necessary.

But where to from here? My reading of the statement leaves the door open to doing another 25bps in July, but it’s going to be a data dependent call. Today’s hike gives them more optionality to decide what to do before going on vacation in August. In coming to this view, the following remarks in the statement are worth emphasizing.

- “....monetary policy was not sufficiently restrictive...”

- “...underlying inflation remains stubbornly high.”

- “Overall, excess demand in the economy looks to be more persistent than anticipated.”

- “….prices for a broad range of goods and services coming in higher than expected.”

- “…with three-month measures of core inflation running in the 3 ½ – 4% range for several months and excess demand persisting, concerns have increased that CPI inflation could get stuck materially above the 2% target.”

- they used “surprisingly” to describe strength in US & Canadian consumer spending.

- “Governing Council will continue to assess the dynamics of core inflation and the outlook for CPI inflation. In particular, we will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behaviour are consistent with achieving the inflation target.”

“Stuck”? “Surprisingly”? These are frank words of admission that the BoC realizes it faces more upside risk to growth and inflation than previously judged. The final paragraph’s guidance certainly does not slam the door on further policy tightening. It keeps it wide open, depending upon the evolution of data and developments.

Please see the accompanying statement comparison. The next decision lands on July 12th with a full MPR and forecasts. Deputy Governor Beaudry will deliver tomorrow’s Economic Progress Report (3:10pmET) followed by a press conference (4:45pmET). The Summary of Deliberations will be published on June 21st. What the BoC also accomplished with a hike today is to disprove the flawed notion that only the Governor can deliver their decisions and that’s a very good thing for Governing Council’s credibility.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.