- Colombia: BanRep Survey: Inflation expectations moderated again in June

Closed US Treasury markets (for Juneteenth) and limited data and events overnight—outside US-China rapprochement developments—has markets trading quietly with a bit of a risk-off feel ahead of a busy ex-US week; shrugging of US-China diplomatic rapprochement.

US equity futures are little changed while European markets gapped a touch lower on the cautious risk tone and a weak end to Friday’s US session. European rates markets are on the backfoot (especially in the UK) and Treasury futures are near Friday’s low. Crude oil prices are a touch lower, copper is down 0.5%, and iron ore is up 0.5%. The USD is up against all major currencies with a loose underperformance of commodity/Asia EM FX; the MXN and CAD, are practically flat. US and Colombian markets are closed today.

Today’s highlight, amid tertiary data, is the BCCh’s decision at 18ET. Bar one submission that sees a 25bps cut, all economists surveyed by Bloomberg (including us) expect a rate hold from Chile’s central bank. This may very well be the bank’s last decision before the rate cutting cycle begins.

We project a 50bps cut in July, which you can read about in our latest Latam Weekly. In a nutshell “the BCCh will go into its rate decision on Monday with well-anchored inflation expectations among economists and traders (surveyed by the bank), and breakeven markets. The bank is not expected to make a rate adjustment, but guidance will likely have clear changes and new projections out on Tuesday that show a lower inflation forecast should reflect a rate path that anticipates over 100bps in cuts in Q3.”

On the topic of rate cuts, Colombia’s FinMin and BanRep board member Bonilla added a bit more colour to his view on rates late on Friday, saying that rate cuts will not come as fast as rate increases. He also said that rate cuts may be considered two or three months after the June meeting. We’ll get some more clues this week as to when BanRep could begin its easing cycle, with economic activity data and imports data out tomorrow and on Wednesday, respectively. The latest BanRep economists’ survey also showed another moderation in inflation expectations (see below). Today, however, Colombian markets are closed (again? yes, with envy).

We have a busy week ahead, on top of the BCCh’s decision, there’s rate decisions from Banxico and the BCB (hawkish and dovish holds, respectively), and Mexican mid-month CPI and retail sales. Chilean markets are closed on Wednesday.

Political developments, as always, are important to watch. Colombia’s regular legislative session is scheduled to end tomorrow (note that lawmakers have called a plenary for today), but the period will likely be extended and will see debate on the government’s social reforms continue. Chilean and Peruvian governments are also struggling with public disapproval amid health outbreaks (respiratory virus in Chile and dengue in Peru). In Mexico, a poll carried out for El Economista showed that (now) former head of Mexico City’s government, Claudia Sheinbaum, leads opinion polls for Morena presidential candidates with 33% against what is thought to be her main opponent, Marcelo Ebrard (former foreign affairs minister), at 21.4%.

—Juan Manuel Herrera

COLOMBIA: BANREP SURVEY: INFLATION EXPECTATIONS MODERATED AGAIN IN JUNE

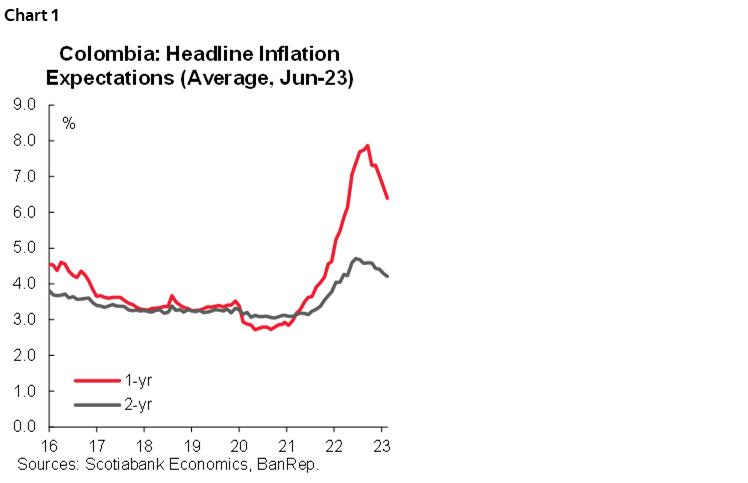

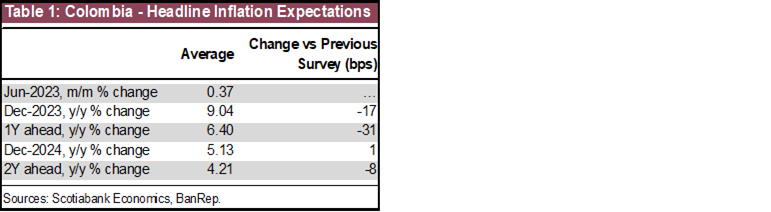

Last Thursday, the Central Bank (BanRep) released its monthly survey of economic expectations. Inflation Expectations (IE) for the end of 2023 decreased once again, registering a decline of 0.17 percentage points compared to the previous survey. This decrease can be attributed to the downward trend in headline inflation observed in May, despite the announcements of upcoming gasoline price increases in the coming months. Currently, the expectations for December 2023 stand at 9.04% year-on-year. Meanwhile, one- and two-year inflation expectations continue to decline (chart 1). By the end of 2024, inflation is projected to reach 5.13% y/y, still above the central bank’s target.

Inflation for June is expected to be 0.37% m/m, leading to a continued gradual deceleration of headline inflation to 12.22% in June. At Scotiabank Colpatria Economics, we anticipate a slightly higher figure of 0.51% m/m (12.37% y/y), which is slightly above consensus. For the end of the year, our projection stands at 8.88%, followed by 4.38% by the end of 2024, slightly below the previous forecast.

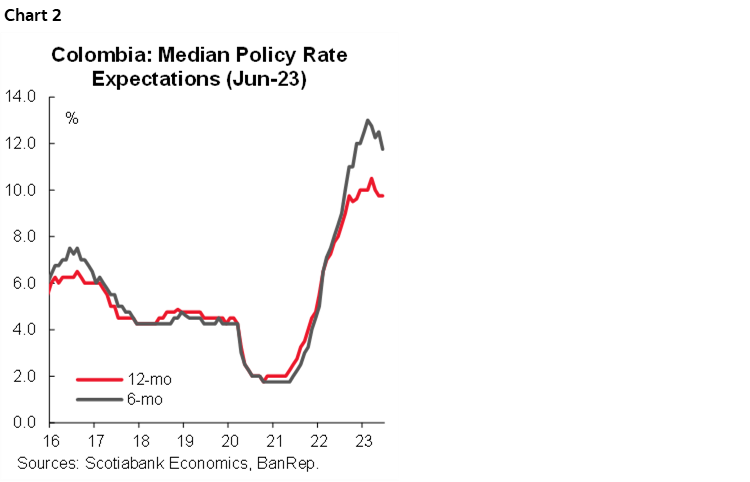

In line with inflation expectations, the market consensus anticipates stability in the monetary policy rate at 13.25% at the June decision, which aligns with Scotiabank Colpatria Economics’ expectations. By the end of the year, the market consensus places the policy rate at 11.75% (50 basis points lower than our projection of 12.25%).

- Short-term inflation expectations. For June, the consensus is 0.37% m/m, which implies an inflation rate of 12.22% y/y (down from 12.36% in May). The survey responses exhibit a wider dispersion this time, with the lowest projection at -0.10% m/m and the highest at 0.59% m/m. Scotiabank Colpatria Economics expects a monthly inflation rate for May of +0.51% m/m and 12.37% y/y.

- Medium-term inflation expectations continued to improve. Inflation expectations for December 2023 decreased to 9.04% y/y, a decline of 0.17 percentage points compared to the previous month’s survey (table 1). This decline occurred despite new information regarding higher gasoline price increases for the rest of the year and an increased probability of the El Niño phenomenon. The inflation expectations for the one-year horizon are at 6.4% y/y, a decrease of 0.31 percentage points compared to the previous survey, while the two-year outlook decreased by 8 basis points to 4.21% y/y. Inflation expectations have declined for five consecutive months, which is a crucial factor supporting the call for rate stability by the central bank.

- Policy rate. The median expectation (chart 2) indicates a stable policy rate until the October meeting, where the first 75 basis points cut is expected. By the end of 2023, the policy rate is projected to reach 11.75%. Scotiabank Colpatria Economics also expects rate stability until October 2023, with the first 50 basis points cut anticipated, resulting in a year-end rate of 12.25%.

- FX. The projections for the USDCOP exchange rate for the end of 2023 averaged 4,250 pesos (350 pesos lower compared to the previous survey). For December 2024, the respondents, on average, expect the peso to settle at USDCOP 4,169 pesos. The USDCOP rate for the end of June is expected to be around 4,195 pesos.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.