- Chile: GDP fell 2% y/y and 0.5% m/m in May

- Mexico: Banxico survey shows better expectations for 2023; remittances rose in May

- Peru: Inflation plunged in June

Closed UST markets with the US on holiday for Independence Day and a quiet overnight session where the RBA’s rate hold was the highlight leave little in terms of broad market moves. The day ahead is quiet in the DM and Latam space, where data releases are limited to Canadian manufacturing PMI and Brazilian industrial production. Canadian and Colombian markets reopen after the long weekend.

The mood is mixed and overnight markets mostly traded in narrow ranges, where the standouts are solid gains in crude oil and iron ore of 1% and 0.4% respectively, against copper losing 0.2%. The USD is mixed to weaker against the key majors, with the MXN marking a new best level in the current cycle this morning at 17.02; a 0.5% appreciation in the CNY/H seems to be weighing on the dollar. US equity futures are little changed, while Treasury futures drift lower alike weakening moves in longer-term European debt.

Brazil’s senate will hold a confirmation hearing for Lula’s candidates to the BCB board starting at 9ET. Yesterday’s results to the BCB’s economists survey showed a lower end-2023 interest rate forecast, at 12% from 12.25% last week, accompanied by a 4.98% year-end inflation projection, from 5.06% previously. Inflation expectations trending in the right direction will add to bets that the BCB will begin its cycle of rates reductions in August as markets head towards pricing in a larger 50bps hike (currently 41bps priced in).

—Juan Manuel Herrera

CHILE: GDP FELL 2% Y/Y AND 0.5% M/M IN MAY

- We estimate a contraction of 0.7% q/q in Q2-23. Technical recession in Q3-23 in the absence of economic acceleration

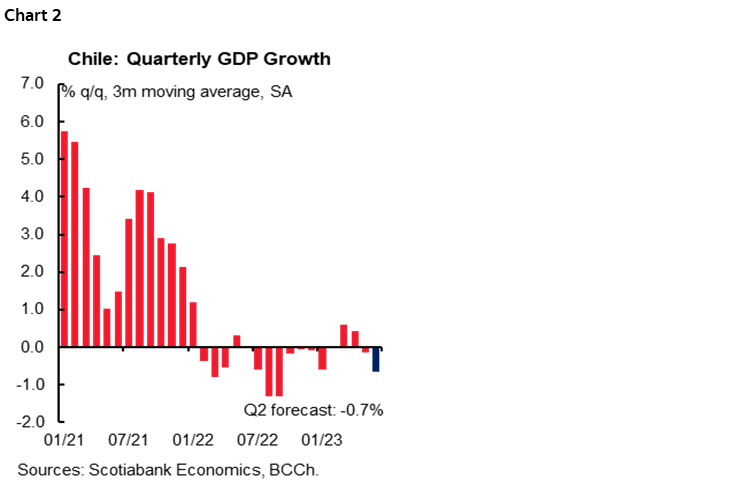

On Monday, July 3rd, the Central Bank (BCCh) released GDP growth (Imacec) for May, which fell 2% y/y, in line with our expectations (Scotia: -2.0%) and below both consensus (-1.7%) and surveys (Economist Survey: -1.1%). Furthermore, this record is a real negative surprise for the BCCh’s baseline scenario in terms of expected GDP contraction in 2023.

The carry-over makes a moderate GDP contraction as expected by the consensus difficult. Avoiding a technical recession in Q3-23 requires an acceleration in June and/or in one of the months of the third quarter. Indeed, if the economy experiences 0% m/m seasonally adjusted growth for the rest of the year, the GDP contraction in 2023 would be above 1%. Moreover, to achieve a contraction of only 0.2% of GDP as in the BCCh’s baseline scenario, the economy needs to recover seasonally adjusted growth in the remainder of the year, a difficult task given the high level of the monetary policy rate, sluggish execution of public and private investment, and negative business and consumer confidence indicators. For now, we project a q/q contraction of 0.7% for the Q2-23 (chart 1). In this context, we anticipate a further downward revision in GDP growth forecast in surveys, currently at -0.5% for 2023.

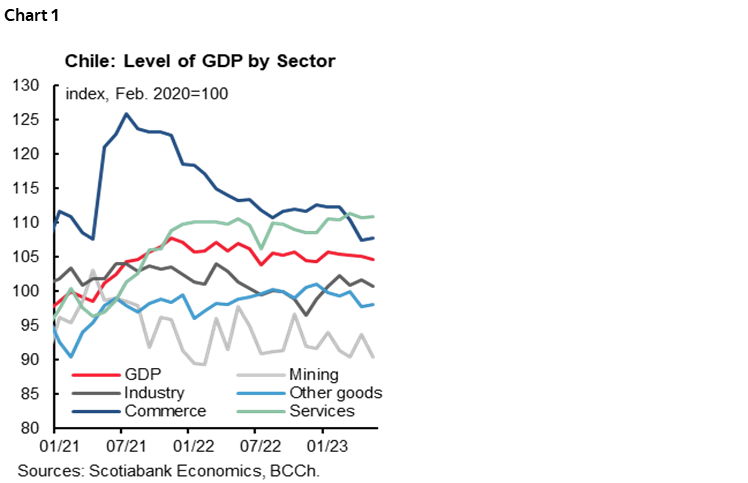

The non-mining Imacec remained stable with respect to the previous month (0% m/m), mainly thanks to the commerce and services sectors, whose economic activity did not show large increases with respect to the previous month, although it was enough to offset the drop in industry and mining GDP (chart 2). This month, commerce would have been positively influenced by the advance of the automotive and retail sectors, which may not be repeated in June based on indicators of high frequency of card purchases. Similarly, personal services continued to show weakness in June due to the negative effects of the rains at the end of the month on educational services, which were partially offset by the increase in health services. In short, both sectors reportedly maintained low levels of activity in June, showing no signs of recovery.

All in all, we reiterate our forecast of a GDP decline of around 0.8% in 2023, worse than the consensus and the baseline scenario of the BCCh.

—Aníbal Alarcón

MEXICO: BANXICO SURVEY SHOWS BETTER EXPECTATIONS FOR 2023

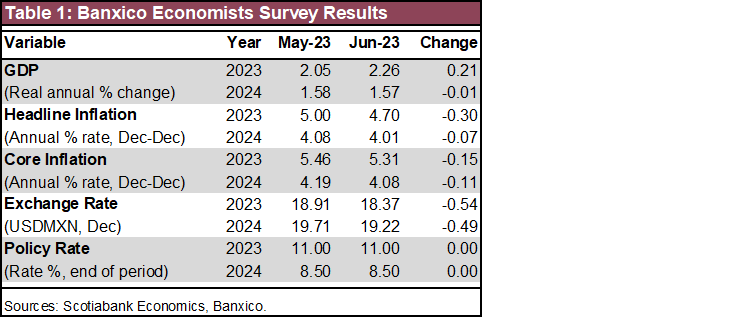

Analysts foresee better economic conditions in the June Banxico Survey. The most noticeable change was in the end of period inflation forecast for 2023, where they expect for a 4.70%, down from the previous 5.00%. However, they still expect challenges in the medium, since average forecast only slightly changed from 4.08% to 4.01% for the 2024, above the 3.0% +/-1% target from Banxico. The core inflation expectation also moved down, albeit at a lower pace, from 4.36% to 5.31% for 2023, and from 4.19% to 4.08% for 2024, suggesting a stickier downward trend in the forecasts horizon.

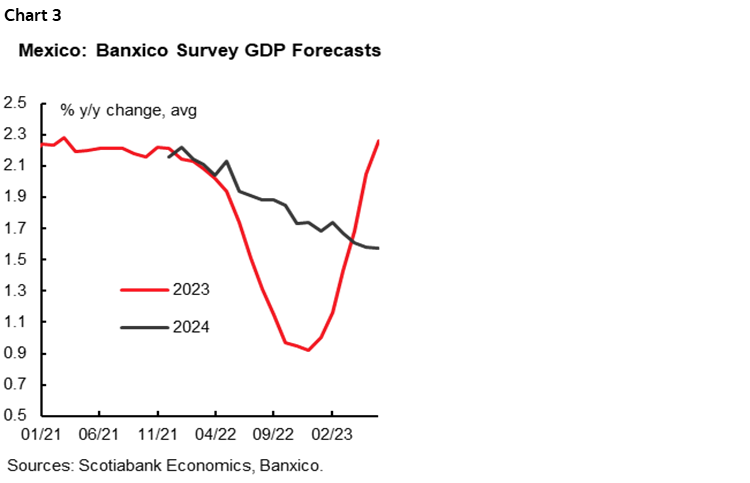

Another patent change was the GDP forecast for the current year, where analysts expect now 2.26% advance, up from the 2.05% previous, whereas the consensus for 2024 stood almost unchanged at 1.57%. This higher consensus goes in line with the above consensus prints for economic activity since late 2022, specially owing to a stronger-than-expected private consumption, although fixed investment has also recently gone up, accompanied by the positive narrative of stronger dynamism by the nearshoring phenomenon.

Regarding the exchange rate forecasts, consensus went down, to 18.37 USDMXN, from 18.91 previously for 2023, and from 19.22 to 19.71 for year-end 2024. In recent weeks, The USDMXN has fluctuated above 17.0, above what we consider might be a psychological threshold (17.00). Forecast suggest that analysts are seeing the current exchange rate somewhat overpriced, with potential harms for the exporting sector.

For our part, we consider the rate spread is the main factor for the recent peso appreciation, but other factors include the dynamism in remittances, and stronger than expected economic activity. Upside risks for the USDMXN include a higher uncertainty for both the Mexican and the US elections in 2024, a negative impact of the consultation process under the USMCA, a economic slowdown in both countries, and higher public debt in Mexico in the short term.

Lastly, the median responses for the Banxico rate remain unchanged, at 11.00% for 2023, and 8.50% for 2024, yet we highlight a still uncertain outlook for both inflation and target rate.

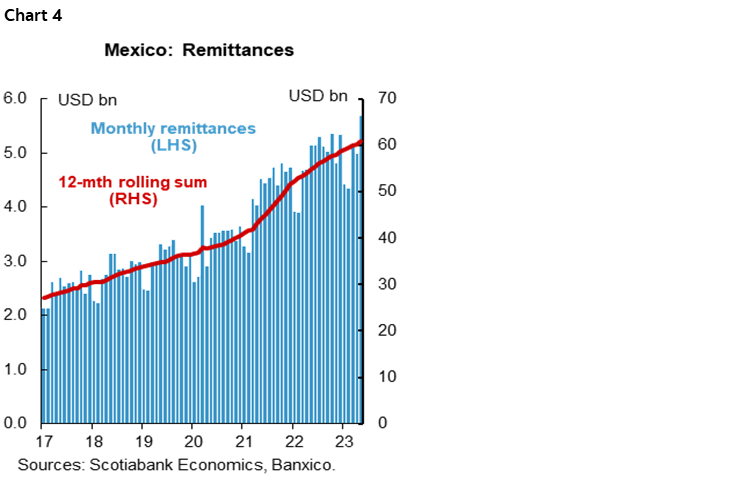

Remittances rose in May, with still strong signs

Remittances in May accelerated to 10.7% y/y from the 6.3% previous, to 5.69 billion USD. This is typically a month where flows outperform, owing to the “Mother’s Day” celebration in Mexico, yet annual increase suggest a still strong dynamism. From January to May, remittances remain almost with the same pace (10.3% vs. 10.1%. YTD previously).

In the 12 months sum, remittances accounted for 60.8 bn USD, equivalent to a 11.0% increase, slightly below the 11.3% previously, but less than half the 24.4% from the same month a year ago, showing clear signs of deceleration, yet still in strong numbers. The tightness in the US labour market has boosted remittances in Mexico since the pandemic, for most of the newly created jobs have come from the services sector, where latinos occupy a big share of services vacancies. In the short term, we expect flow to remain positive, although moderating, contributing to support private consumption, along with an also tight Mexican labour market.

—Miguel Saldaña

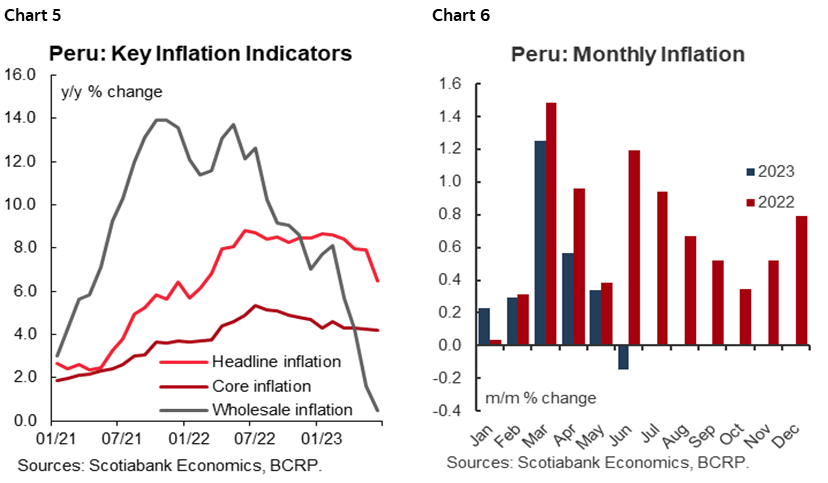

PERU: INFLATION PLUNGED IN JUNE

Yes, we were expecting a low monthly print for June, and also a sheer drop in the yearly rate. But the actual figures surprised even our expectations. Monthly inflation was down 0.15%. Yes, negative inflation. This was possible, but uncertain. Yearly inflation declined to 6.5%, from 7.9% in April, and a tad below our expectations of 6.7%–6.8%.

This raises expectations that the BCRP may move forward its decision to begin lowering the reference rate. We continue to expect the BCRP to maintain the current rate of 7.75% during the July 13th meeting. We are not changing our opinion that the BCRP will not begin lowering the reference rate until November, but are intrigued at the possibility of an earlier decision, which will likely hinge on another sharp downturn in inflation in July. What gives greater credence to the expectation that inflation will continue declining notably in coming months is the trend in the wholesale price index. Wholesale inflation, which was 8.1% only four months ago, in February, shot straight through the BCRP target range (from 1% to 3%), and has come out at the other side, with yearly wholesale inflation registering only 0.5% in June.

Other information that has been released were in line with our expectations (see Latam Daily). Mining GDP for May was up 21% y/y, on two counts, the full impact of the new Quellaveco copper mine and a low base in 2022 due to roadblocks. The was offset by a 71% decline in Fishing GDP, as the initiation of one of the two large yearly fishing seasons, which typically begins in May, was postponed due in part to the impact of severe El Niño related countercurrents. The balance means low, or no, growth in May aggregate GDP.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.