- Colombia: Monetary Policy Preview, is BanRep ready for a pause?

- Peru: Inflation to decline significantly in June, but so will early GDP indicators for May

Asia trading calm with Singapore closed for business was disrupted by on balance stronger than expected inflation data in Spain and at the state-level in Germany (ahead of the national print at 8ET). The figures weighed on rates markets that are weakening in flattening fashion across the majors and helped dent the USD’s rally on Wednesday—though most FX are in +/-0.1/2% ranges vs the dollar. SPX futures are a touch stronger, as is oil in contrast to 0.5% and 1.2% declines in iron ore and copper, respectively. Global markets have US jobless claims and a third release of US Q1 GDP to look forward to at 8.30ET.

In Latam, the focus will be on central bank events and Chile’s unemployment rate data at 9ET. On Chile’s print, from our latest Latam Weekly: “ We project an increase in this indicator with respect to the last moving quarter—to 9.1% from 8.7%—due to an increase in the labour force versus our employment gains expectation. In this sense, we see that both public and private salaried employment will continue to show less dynamism than in previous quarters, mainly the private sector which is losing employment due to the deterioration of labour-intensive economic sectors. “

Colombia’s FinMin and BanRep board member Bonilla speaks at a couple of events (9ET and 13.15ET), where may again express his view that rate cuts may begin in September. BanRep holds a policy meeting tomorrow, so he may choose to abstain from mon-pol comments, however. A rate hold is universally expected (see below). At 11ET Mexican Fin Min Ramirez de la O speaks on the government’s Q3 auctions schedule.

From Chile’s BCCh, Garcia and Cespedes speak at 9.45ET and 11ET, respectively, with the former at a Chile Day event in Toronto where Fin Min Marcel will also talk pension reform and mining sector. Cespedes will present the BCCh’s June MPR (see here). We heard from BCCh dove Griffith-Jones yesterday, who said that the bank should cut rates by at least 50bps in July given a path to 8% by year-end (325bps in total). Recall that she dissented at the most recent decision in favour of easing instead of the hold that the majority approved.

At 7ET, the BCB releases its quarterly inflation report that includes new projections and at 10ET the bank's president Campos Neto will give his take on it. Also today, the country’s National Monetary Council (Campos Neto, Min Fin Haddad, and Planning and Budget Min Tebet) meets to reaffirm the 3% inflation targets for 2024 and 2025 as well as unveil what will likely be an unchanged target for 2026. We maintain that the BCB will begin its cutting cycle in August with a 25 or 50bps reduction.

—Juan Manuel Herrera

COLOMBIA: MONETARY POLICY PREVIEW, IS BANREP READY FOR A PAUSE?

BanRep will hold its regular policy meeting this Friday, June 30th. After 1150bps in hikes since September 2021, we expect BanRep to end its hiking cycle and leave the policy rate at 13.25%, an expectation in line with analysts’ consensus and market expectations. On top of the decision, we think this time is more important the message that communiqué and post-meeting press conference will send. Specifically, the distribution of the votes and the importance that Minister Bonilla and Governor Villar will assign to recent activity deceleration and downward surprise in headline inflation.

Since the last decision-making meeting (April 28, 2023), headline inflation has shown stronger-than-expected deceleration dropping 98bps to 12.36% y/y, on the back of a faster-than-expected normalization path of food prices, while core inflation continues to stay above 10% y/y. Having said that, the COP has appreciated almost 9% since April, which will help core inflation start to ease soon. In fact, inflation expectations point to a one-digit headline inflation (~9% y//y in December 2023), which although is still 3x the BanRep’s target, points to a positive and restrictive policy rate at a current level.

Additionally, economic activity is showing stronger-than-expected deceleration. April’s economic activity fell on a y/y basis, while consumer credit is falling in real terms by more than 4pp in May, and the health of this type of credit is deteriorating faster. NPLs for consumer credit went to 6.7% in March 2023 from 4.4% last March. We foresee those durable goods, which are the more sensitive consumption to interest rates, are the type of goods that most have decelerated this year due to higher inflation but also higher credit interest rates.

Therefore, we think new data point that the current level of the monetary policy rate is enough to help to consolidate headline inflation deceleration and to anchor inflation expectations in the medium term, while the policy rate is every day becoming more and more restrictive which contributes to the economic activity deceleration.

All of the above let us anticipate that BanRep will keep the policy rate at 13.25% this Friday, while will send in a non-necessarily unanimous decision that is not ready to start an easing cycle and will wait for the consolidation of the inflation deceleration, which in our opinion is going to be in October’s meeting. Having said that, we think the possible surprise is that the board sends a more dovish message with a unanimous decision and explicitly saying that is the end of the hiking cycle.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

PERU: INFLATION TO DECLINE SIGNIFICANTLY IN JUNE, BUT SO WILL EARLY GDP INDICATORS FOR MAY

June inflation figures will be released on Saturday, July 1st. The key prices that we follow suggest that monthly inflation for June is tracking at about 0.1%. If this plays out as we expect (more or less), then yearly inflation in June should plunge to 6.8% from 7.9% in May. Government officials are expecting something similar, with authorities mentioning yearly inflation figures of 6.7% and “below 7.0%”.

An exceptionally high base in June 2022 is a leading factor in the improving inflation picture. We do not, however, see the BCRP reducing its reference rate based on the drop in inflation in June, nor on a similar decline that we expect to take place in July. The BCRP cannot implement policy reversals on the basis of convenient base comparison effects alone. We continue to expect the BCRP to maintain the policy rate at 7.75% throughout Q2 and Q3, and not begin lowering its rate until Q4, when we expect a 50bps decline.

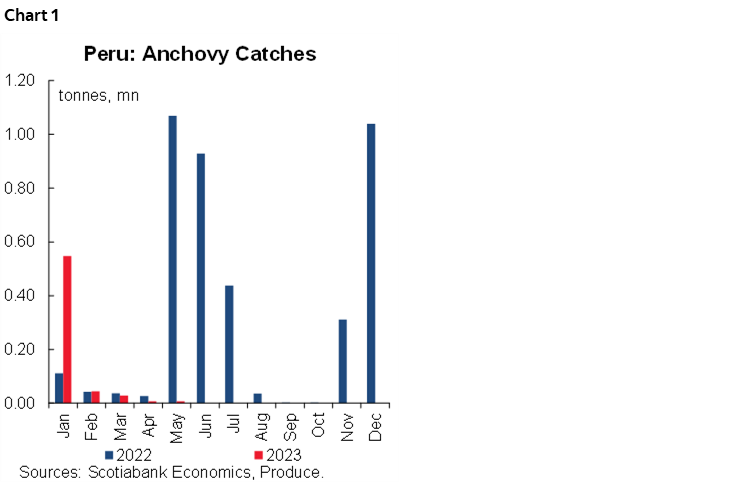

Also on Saturday, May mining and fishing GDP figures are to be released. Fishing will be interesting, as the largest component of fishing, the heavily regulated anchovy fishing for fishmeal, has been highly affected by El Niño. The fishmeal season typically runs from May to July. This year the start of the season has been delayed, and may be suspended altogether. In May 2023 in particular, no anchovy fishing was permitted. This contrasts with 2022, which should hugely affect the y/y fishing GDP growth figure to be released on Saturday (anchovy fishing for fishmeal makes up over 40% of total fishing GDP in a typical year). The difference with May 2022 is huge (see chart 1, the bar for May 2023 is barely perceptible). We do not have the figure for catches over the full spectrum of species, but if the remainder of fishing (non-anchovy fishing) in May is similar to May 2022, then the low anchovy catch alone would spell a 70% y/y decline in fishing GDP. Even considering that fishing has a low (2%) weight on GDP, such a large decline has the potential to be a strongly negative factor for May GDP growth.

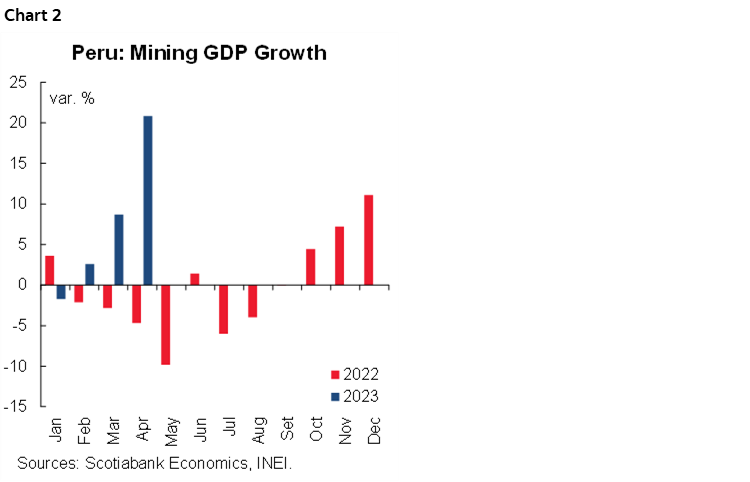

Thankfully, we also have mining. Mining GDP growth was 7.4% y/y, in the year to April, and 21% y/y in April alone. In May growth should be similarly high, or even higher, as production in May 2022 was particularly affected by social protests (chart 2), providing a particularly low base to rebound off of.

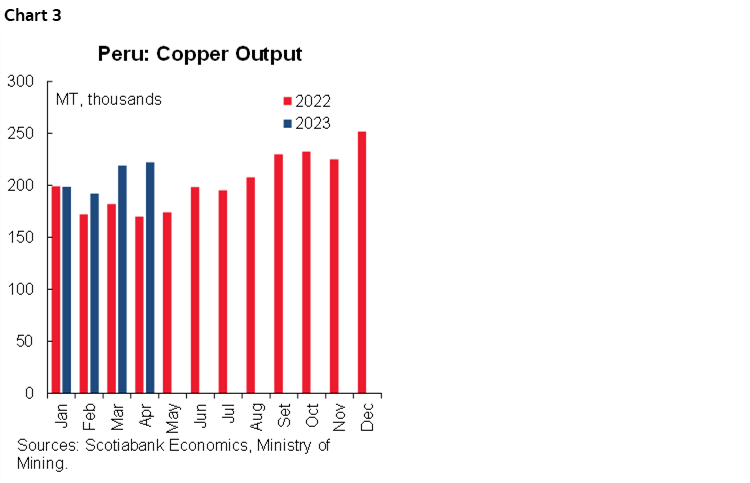

The increase in copper output is leading the way in mining. Copper output was up 15.7% y/y in the year to April and 31% y/y in April alone (chart 3). There are two factors driving copper production growth. One is the Quellaveco copper mine, which represents 10% of Peru’s current total copper output, which came on stream in September 2022. The second is the impact that protests had on mining operations in April–May 2022, and which have not recurred in April–May 2022. In 2022, large operations including Las Bambas (MMG) and Cuajone (Southern Peru) were partially disrupted due to protests.

Both effects existed in April, and should persist in May, supporting the notion that copper output may well rise around 30% y/y again, boosting mining GDP.

What will be of even greater interest to see, and is much more difficult to anticipate, is how key domestic demand sectors performed, in particular Manufacturing. Sectors linked to domestic demand have been particularly weak in the year-to-date. There is no real reason to believe that May will be notoriously better. The risk, rather, is that the economy will again underperform. All in all, May does not seem to be the month which will show the economy turning around.

The drop in fishing GDP in May is likely to be too severe to be offset by mining. Thus, we expect May to be another month with weak GDP growth. The figure for aggregate May GDP growth will be released on July 15. Hopefully, GDP growth in June will be more normal, although we feel like we’ve been repeating that prayer month after month for some time now.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.