- Colombia: Headline inflation was in line with expectations, while core inflation reflects a divergent dynamic between goods and services prices

It was a mostly uneventful start to the week in Asia and Europe, and the day ahead is equally quiet ahead of a busy schedule of central bank decisions and key data releases. An early-Europe Bloomberg report on BoJ insiders saying officials aren’t pressed to end negative rates on the 19th woke up trading but had limited after-effects. Over the weekend, Chinese inflation was a solid miss, reflecting steep declines in pork prices but also muted services inflation reflecting weak domestic demand.

In the G10, we’ll only have the NY Fed’s survey of consumers on tap in terms of data, while the UST auctions of 3s and 10s at 11.30ET and 13ET are the main on-calendar risk for markets. The US also sells 30s on Tuesday, which may mean that supply disproportionately weighs on the long-end in the first half of the week while the remainder of the week could be a drag on the front-end as central bankers attempt to stop rate cut bets in their tracks. The US publishes CPI data tomorrow and the Fed announces policy on Wednesday.

USTs are slightly bear steepening, in contrast to bull flattening German rates and bull steepening gilts. WTI and Brent are down 0.3/4%, sliding off their best levels about two hours ago, while iron ore tracks a 0.5% decline and copper drops 0.9% with both possibly impacted by disappointing Chinese data. US equity futures are little changed as is ESX cash while FTSE trades 0.3% lower. The BoJ news triggered a move higher in the USDJPY of about 100 pips, to shed 0.8/9% as the worst major today. Most other majors are also trading weaker against the USD although the EUR and GBP are little changed, while the MXN sits in the middle of the pack, down 0.2%.

The Latam day ahead doesn’t have much to get local markets going, although Brazil’s, Colombia’s, Chile’s, and Peru’s reopen after Friday’s holidays. Moves in Colombia will likely be outliers as traders will also react to the post-trading release of November CPI last Thursday (see below). Today, there’s only the weekly BCB survey results to watch and central bankers will be quiet ahead of their respective decisions.

This week (see Latam Weekly), we’ll get policy updates from the BCB, Banxico, and the BCRP but there may be little room for surprise. The BCB is very clearly on track for 50bps cuts this week and at their February meeting. In Peru, downside surprises in inflation and a weak economy could motivate a 50bps cut according to some, but caution will likely overpower dovish inclinations, resulting in the 25bps that we project. Banxico already surprised us at their previous meeting by opting for less hawkish guidance, so markets may already be going into the decision thinking that the bank could somewhat tee up a February start to cuts.

—Juan Manuel Herrera

COLOMBIA: HEADLINE INFLATION WAS IN LINE WITH EXPECTATIONS, WHILE CORE INFLATION REFLECTS A DIVERGENT DYNAMIC BETWEEN GOODS AND SERVICES PRICES

Monthly CPI inflation in Colombia stood at 0.47% m/m in November, according to DANE data released on Thursday, December 7th. The result was broadly in line with the economist’s expectations of 0.46% m/m, according to BanRep’s survey, while it was above Scotiabank Colpatria’s expectation of 0.41 % m/m.

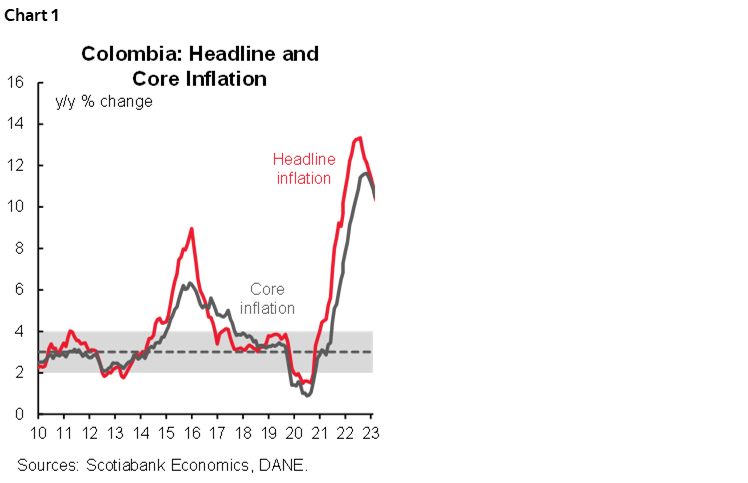

Annual headline inflation declined for the seventh month, from 10.48% in October to 10.15% in November (chart 1), the lowest since June 2022 (9.67% y/y). Core inflation delivered an unexpected spike, interrupting four consecutive months of reduction; non-food inflation is now at 10.61% y/y, 0.10 percentage points higher versus the previous month’ figure; however, inflation ex-food and regulated fell significantly from 9.20%y/y in October to 8.86% y/y in November. That said, the upside surprise in ex-food inflation came from electricity prices, which increased by 5.89% m/m. On the other side, inflation ex-food and regulated price reduction was explained again by lower tradable goods inflation (especially vehicles). In contrast, core services inflation remains sticky at 9.03%, resulting from indexation effects, especially in rent fees.

November CPI gives arguments to both sides of BanRep’s board. On the dovish side, some members could see the headline inflation reduction as enough progress to start the easing cycle, as projections point that inflation could close at a single-digit levels in December. However, hawks will point to persistently sticky core inflation, which is an argument to wait a bit more before starting the easing cycle. In Scotiabank Colpatria economics, we continue to think that the recent economic activity deceleration plus the current account deficit coming in well below BanRep expectations are arguments to start a very gradual easing cycle and cut the benchmark rate by 25bps at the December 19th meeting. However, we know that it will be a close call.

A reason for the board to delay the rate cut is that inflation remains more than three times above BanRep’s target of 3%. There is a pending negotiation of the minimum salary, and other sources of upside risk on inflation could potentially materialize in forthcoming months. Before the December 19th meeting, BanRep will have, as a final input, the economic activity indicators for October and the Federal Reserve meeting; we think both are critical in defining this debate about the start of the easing cycle.

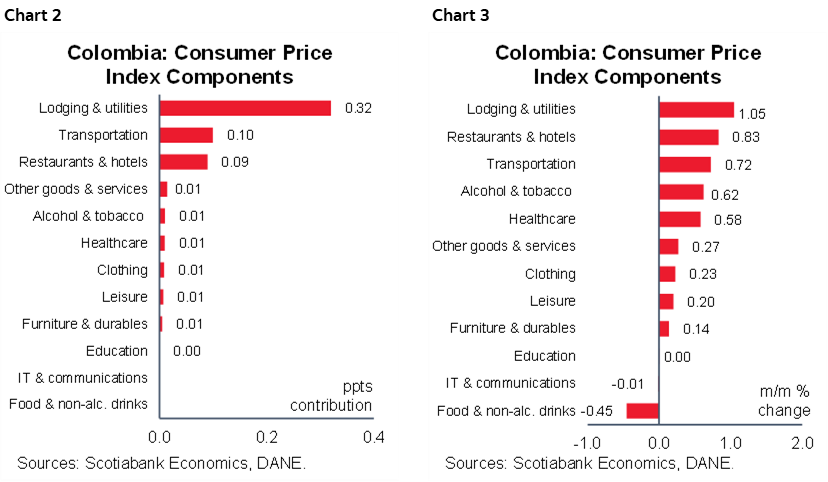

Looking at November’s figures in detail, food inflation is the group that generated the greatest upside pressure on inflation during the month (charts 2 and 3).

Complementary highlights:

- The lodging and utilities group was the main contributor to monthly inflation. The group recorded +1.05% m/m inflation and +32 bps contribution. Rent fees accelerated, posting a monthly figure of 0.47% m/m. However, it remains below the average 0.69% m/m inflation recorded in 2023. Either way, indexation effects remain a concern for 2024; in that regard, minimum wage negotiations will be critical for BanRep in assessing inflation risk. Utility fees increased by 2.85% m/m due to significant increases in electricity prices (+5.89% y/y) as a result of higher prices derived from speculation for the “El Niño” weather phenomenon in market electricity prices; we expect this effect to moderate as some of those upside pressures are vanishing.

- The transport group recorded a 0.72% monthly inflation, reflecting the increase in gasoline prices (+3.6% m/m), which offset the reduction in tradable items such as vehicles (-0.7% m/m) and airfare (-3.78 % m/m). In the medium term, a source of uncertainty came from the potential increase in diesel prices and toll fees. The government already said they will pursue increases in both in 2024, which could delay the inflation convergence towards the target of 3% even more.

- Food items inflation recorded a -0.45% m/m inflation and subtracted to the headline 9bps. In November, fresh fruits (-6.02% m/m), tomatoes (-18.52% m/m), and onion (-11.52% m/m) contributed to the lower inflation, while on the upside side, processes met prices increased by 7.26% m/m in anticipation of the holiday season by the end of the year. Either way, food inflation is normalizing, and despite the forthcoming months, we are vigilant of the effect of the “El Niño” weather phenomenon; we only expect a material impact on prices if this phenomenon lasts longer than current projections.

- Inflation by major groups: goods inflation decreased significantly, going down from 9.51% y/y to 8.45% y/y, while services prices decreased in a lower magnitude to 9.03% vs. the previous 9.07% y/y, and compared with the peak recorded in July, services inflation has gone down only by 16 bps.

—Sergio Olarte & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.