- Colombia: Moderation in Colombian economic activity: manufacturing and retail sales remained in negative territory, miss analyst estimates

- Peru: Fiscal balance is favourable, but the devil is in the details

Range-bound Asia markets that made little of PBoC rate cuts were followed by a more risk averse feel to European hours with no clear explanation that has US equity futures about 0.3/4% weaker, global rates curves losing ground, and a mixed USD where high-beta FX are underperforming with muted 0.2% drops. Commodity prices are mixed as iron ore catches a small bid in contrast to a 1.2% drop in copper and a slight decline in crude oil. Global markets await the release of US retail sales and Canadian CPI data at 8.30ET, after UK wages data beat expectations earlier today.

Peruvian and Colombian GDP data out at 11ET and 12ET, respectively, are the day ahead highlights in Latam, accompanied by Peruvian jobless rate figures and BanRep’s economists survey and trade balance and imports data in Colombia. Uruguay’s central bank is also expected to announce a 50bps reduction to its policy rate to 10.25%, and we’ll continue to monitor developments in Argentina for spillovers to the rest of the region’s markets.

We’ve got mixed guidance from Peruvian authorities on the country’s economic performance in June. First, Fin Min Contreras had guided a decline of about 1% y/y, but changed his tune last week to project nil growth for the month. On Friday, however, the BCRP teed up a 0.5-0.7% y/y contraction that is closely aligned with the 0.7% drop forecast by the median economist polled by Bloomberg.

In any case, the first half of 2023 was a poor showing for Peru’s economy, and were it not for strong gains in copper output from the recently-opened Quellaveco mine the first half of the year would have shown an even larger contraction amid muted growth in services. We think a weak print today will add to expectation that the BCRP will begin lowering the reference rate at the September meeting, with a 25bps cut. July unemployment data out at 11ET will also be watched for weakness spreading to labour markets (median 6.4%, Scotiabank: 6.6%, same as June).

As for Colombia, yesterday’s weaker than expected retail sales and industrial sector data for June (see below) added to downside risks for today’s Q2 GDP release. Our team projects a 0.4% y/y gain, alike the Bloomberg median, that would mark a strong deceleration from the Q1 pace of 3% y/y. On a quarter-over-quarter basis, economists are also penciling in the first decline in GDP since 2021. It is a weak result, but improvements are expected in the second half of the year while persistently strong core inflation keeps BanRep cuts at bay—at least until the fourth quarter. On that note, the results to the bank’s survey of economists will shed some light on how many analysts side with Fin Min Bonilla’s view that cuts could start in September.

—Juan Manuel Herrera

COLOMBIA: MODERATION IN COLOMBIAN ECONOMIC ACTIVITY: MANUFACTURING AND RETAIL SALES REMAINED IN NEGATIVE TERRITORY, MISS ANALYST ESTIMATES

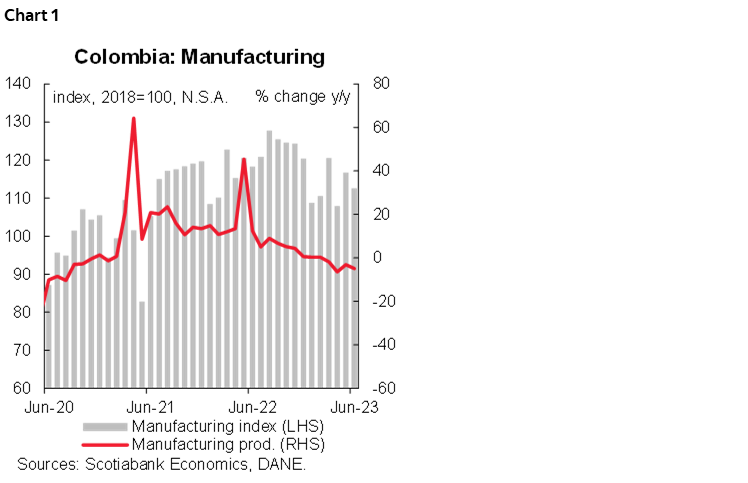

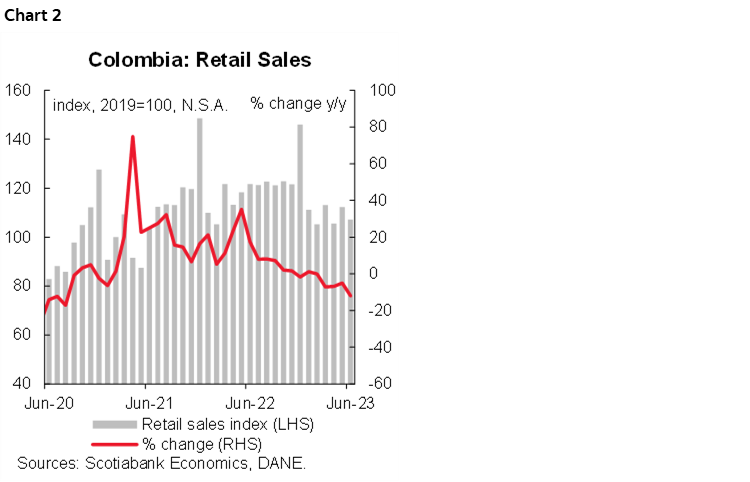

On Monday, August 14th, The National Administrative Department of Statistics (DANE) published information on manufacturing and retail sales for June 2023. The real production of the manufacturing industry again fell on a y/y basis, it came in at -4.8% YoY in June 2023. Meanwhile, real retail sales decreased by 11.9% YoY in June and became the lowest annual variation since August 2020. Thus, June became the fourth consecutive month in which the manufacturing industry along with retail sales came in negative territory. In addition, these results surprised market expectations, including our projections, by a wide margin.

In the year to date until June 2023, the real production of the manufacturing industry showed a variation of -2.6%, compared to the same period of the year 2022, while during the first half of 2023, compared to the period Jan–Jun 2022, retail sales decreased by 5.2%.

These results confirmed the gradual adjustment of economic activity. Having said that, we think that economic activity touched the bottom in June 2023 and will start a gradual and slow-motion recovery. This moderate slowdown has been reflected in reductions in investment in machinery and equipment, and lower demand for durable and semi-durable goods by household consumption.

Manufacturing production

Manufacturing production contracted by 4.8% YoY in June 2023 (chart 1), being the fourth consecutive month. In seasonally adjusted terms, manufacturing contracted by 1.1% monthly, after the slight improvement recorded from the previous month.

In annual terms, the sectors that showed better performance were sugar and panela processing (+47.2% YoY), coking, oil refining and fuel blending (+8.5% YoY), soap, detergent, and perfume manufacturing (+7.0% Yoy), and beverage processing (+5.4% YoY). On the other hand, the sectors that registered the largest contractions were precious metal industries (-34.1% YoY), manufacturing of other types of transport equipment (-32.1% YoY), manufacturing of motor vehicles (-31.3% YoY), wood processing (-28.8% YoY) and manufacturing of basic chemical substances (-25.6% YoY).

In turn, other important industries experienced annual contractions, particularly those associated with durable and semi-durable goods, such as rubber product manufacturing (-19.9% YoY), garment making (-18.6% YoY), spinning of textile products (-18.5% YoY), and vehicle body manufacturing (-13.0% YoY).

Retail sales

Retail sales contracted by 11.9% YoY in June 2023 (chart 2), the lowest record since mid 2020 and the same as the manufacturing industry, recording the fourth consecutive month of decline. This result came below the -7.0% YoY expected by Bloomberg analysts. In seasonally adjusted terms, retail trade without fuels or vehicles showed slight growth of 0.2% MoM, compared to the previous month. These results show a slight recovery in household consumption this year, after four consecutive months of declines.

In annual terms, the behaviour of retail sales in June 2023 were influenced by the fall in sales of durable goods such as televisions (-47.1% YoY), household appliances and furniture (-37.8% YoY), computer and telecommunications equipment (-37.8% YoY), vehicle and motorcycle sales, which decreased by 16.6% YoY in June, along with the component of other vehicles and motorcycles (-36.6% YoY), hardware, glass, and paint (-20.1% YoY).

Non-alcoholic beverages (+24.4% YoY), alcoholic beverages and cigarettes (12.0% YoY), and personal hygiene and perfumery products (+6.2% YoY) were the categories that showed the highest annual growth during June 2023.

It should be noted that other goods such as clothing, food, pharmaceuticals, footwear, and household cleaning products continued to experience contractions, reflecting the correction in household consumption patterns in a scenario of high-interest rates, added to the statistical base effect due to the VAT-free day a year ago and lower demand for pandemic-related products such as masks among other health-related items.

Concluding remarks

Today’s data were weaker than expected, although we must wait to see the performance of sectors related to services such as hospitality and transportation (with the release of activity data tomorrow, Tuesday, August 15th). At Scotiabank Colpatria, we estimate a GDP growth of 0.4% YoY in Q2, the weakest expansion since Q1-2021. In any case, the market forecast ranges between 0% and 1% expansion (BanRep +0.7% YoY). Having a result within this range, in our opinion, will probably not significantly impact market expectations regarding monetary policy.

At Scotiabank Economics Colombia, we see a low probability that BanRep will cut rates in September, instead, we continue to lean towards thinking that the first-rate cut could be in the last quarter of 2023 or later, waiting for new signs of inflation convergence to the target.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

PERU: FISCAL BALANCE IS FAVOURABLE, BUT THE DEVIL IS IN THE DETAILS

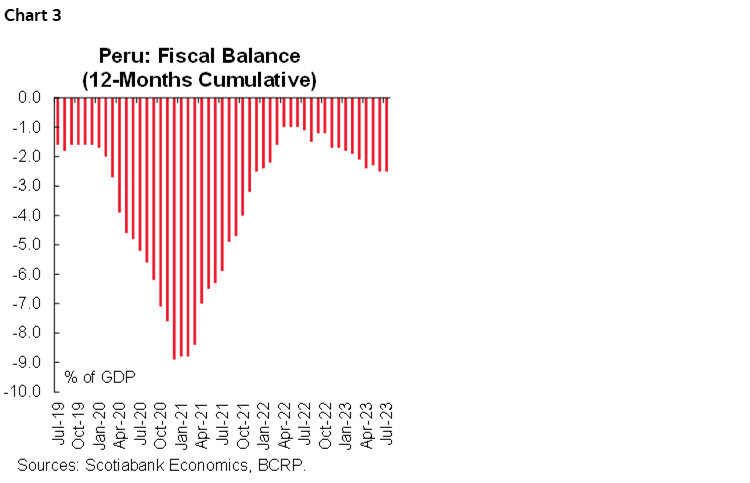

The BCRP reported a fiscal deficit of 2.5% in GDP for July. This was largely expected. Additionally, although the figure was, perhaps, a tad high, it was broadly within the realm of a full-year 2.4% GDP fiscal deficit, which is the ceiling for Peru’s fiscal rule (chart 3). The bottom line is that Peru’s fiscal situation remains quite manageable.

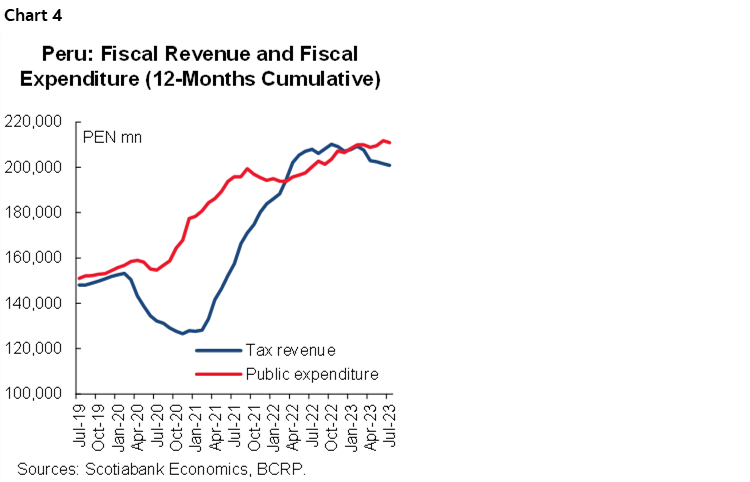

And yet, fiscal accounts are not without some concern. At least not when you take a deeper look. Government revenue was down 5.3% y/y in July, and this was not an outlier, as revenue declined 5.1% y/y in the year-to-July. Income tax, down 6.1% in July and -12.1% YTD, was the main culprit. And, within income tax, mining made up the bulk of the decline. This was expected, because mining taxes were exceptionally high in 2022. Even so, the magnitude was surprising. Mining revenue was down 32% YTD (-45% y/y in July) in terms of monthly payments. Furthermore, mining also makes up the bulk of the yearly balance adjustment which takes place mainly in April–May, and which declined 36% this year.

The only other consistently declining component of tax revenue was sales tax on imports, down 11.4% YTD (-15% y/y in July), which reflects plunging imports value.

Outside of mining, tax revenue fared moderately well. Note that, as if to underscore the base comparison aspect of the decline, the BCRP also published tax growth figures for 2023 over 2021. In these terms, overall government income was up 17.7% YTD for 2023 versus 2021, much better than the 5.1% decline YTD for 2023 over 2022.

Domestic sales tax, which is an indicator of the strength of domestic demand, held up better, up 2.8% YTD, and 5.8% y/y in July. Hopefully, the figure for July portends the beginning of a bit of a rebound starting July.

A look at the expenditure side of fiscal accounts is not entirely comforting. Fiscal spending was up 4.1% YTD, but down 4.4% y/y in July (chart 4). This is quite modest growth, which one might feel grateful for considering how low revenue growth is. And yet, with private investment so low, one might wish to see public spending, and public investment (+4-9% YTD; -7.9% y/y in July) in particular, making up for the slack. On the other hand, if heavier spending with revenue so weak could imperil reaching a full-year deficit of 2.4% of GDP, which is the ceiling established by the fiscal rule.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.