- Colombia: Unemployment rate surprisingly declined in June, reaching single digits

- Mexico: Q2 GDP beats thanks to still-strong services

- Peru: July inflation could be the last close to 6%; President Boluarte’s Independence Day address stressed business as usual

European hours traded with a risk averse, sell everything feel. Crude oil is chopping around to lose about 0.5% on the day, and iron ore and copper are off ~1.5% and 0.8%, weighed by a weak Chinese Caixin manufacturing PMI (first sub-50 since April). SPX futures have erased the US Monday late-session gains, tracking a 0.3% loss. Rates curves are steepening for the most part, with modest conviction.

The USD is posting widespread gains versus the majors, where the AUD takes a 1.2% hit from the RBA’s dovish rate hold overnight and the MXN sits in the middle of the pack, down 0.3% and building a small buffer away from its best levels around 16.63 last week. Gloam markets are looking ahead to the release of US JOLTS job openings and ISM manufacturing data.

Another busy day awaits in Latam today, with Chilean June economic activity, Peruvian inflation, Banxico’s economists survey, and Brazilian industrial production data all on tap. Today’s releases come just after BanRep’s rate decision yesterday (see here) and Friday’s BCCh decision (see here), as well as a stronger-than-expected Q2 GDP and unemployment data yesterday in Mexico and Colombia, respectively (see below), and weak Chilean retail sales (-13%v vs –9.9% y/y median) that contrasted with a better than expected but still contracting industrial production reading (-2.7% vs -4.0% y/y median).

Below, our Peru team outlines their projection of a 6.3% y/y inflation print for Lima, 0.5ppts above the Bloomberg median forecast of 5.8%, owing to a rebound in poultry and fresh food prices. As for Chilean economic activity, the 1.4% y/y contraction seen by the median economist (Scotiabank at –1% y//y) would be the ninth drop in ten months, a result that is clearly supportive of the BCCh’s 100bps rate cut on Friday. Chilean markets will also follow Boric’s announcement of details of his government's fiscal pact this afternoon.

In the June edition of Banxico’s survey, end-2023 and end-2024 Banxico rate projections averaged 10.91% and 8.43%, respectively (Scotiabank Economics at 11% and 8.25%, in that order), while year-end inflation was seen at 4.7% and 4.0% (Scotiabank at 4.7% and 4.1%). We likely won’t see significant changes based on the latest Citibanamex survey, and data since the June poll have not materially impacted expectations for inflation or Banxico policy—while yesterday’s GDP data will not be reflected in today’s survey results.

—Juan Manuel Herrera

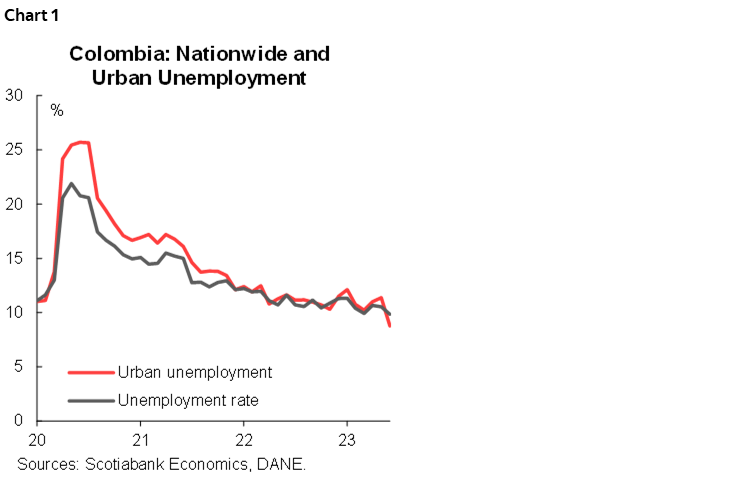

COLOMBIA: UNEMPLOYMENT RATE SURPRISINGLY DECLINED IN JUNE, REACHING SINGLE DIGITS

On July 31st, the National Administrative Department of Statistics (DANE) published labour market figures for the month of June. The national unemployment rate decreased to 9.3%, while the urban unemployment rate stood at 8.8%. These single-digit results had not been seen since November 2022 and represent the lowest rates recorded since November 2018 for the national total and since November 2015 for urban areas. Additionally, the employment rate for June 2023 was 58.3%, indicating a 1.8 ppts increase compared to the same month in 2022 (56.5%).

Seasonally adjusted monthly figures also recorded a decrease as the national unemployment rate reached 9.8%, the lowest since August 2018, while the urban unemployment rate was recorded at 8.8%, marking the lowest rate ever recorded (chart 1).

These labour market results for June interrupted the stagnation observed in job creation during the previous months, probably reflecting that economic activity is decelerating but at a moderate pace. This will be an additional element to consider by BanRep when determining if interest rates should remain stable in coming months.

Highlights:

- In June, the female unemployment rate was 11.6%, while the male unemployment rate stood at 7.7%, resulting in a continuous narrowing of the gender gap, reaching 3.9 p.p.—the lowest level since 2017.

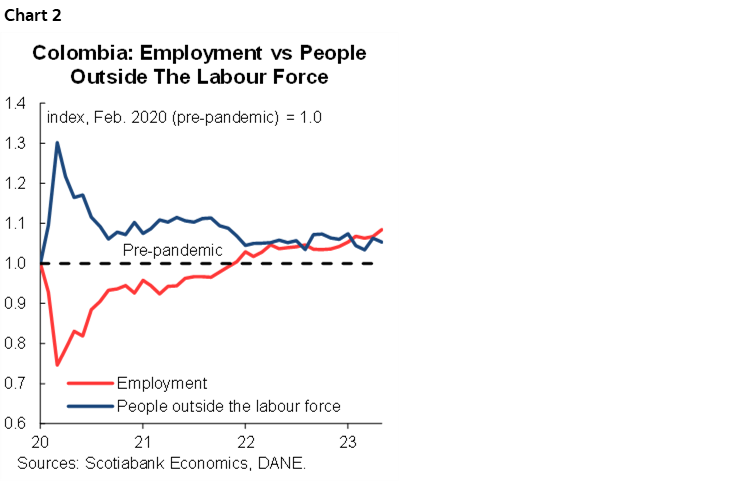

- During June 2023, total employment stood at 23.1 million people, an increase of +1 million y/y (chart 2). Employment increase was primarily driven by the female population, which posted an increment of +591 thousand jobs compared to June 2022. The female population in urban areas accounted for 52.9% of the total employment growth (+350 thousand). On the other hand, the male population accounted for an increase of +439,000 employed individuals in June 2023 compared to the same month the previous year, mainly coming from urban areas, which contributed to 44.0% of the new employment (+326,000).

- The sectors that contributed most positively to the variation in the employed population in June 2023 were public administration and defense, education, and health services (+269,000); followed by professional, scientific, technical, and administrative services (+266,000) and transportation and storage (+146,000). Similarly, the sectors of artistic, entertainment, recreation, and other service activities, accommodation and food services, along with trade and vehicle repair, showed positive contributions of +105,000, +92,000, and +88,000, respectively. Conversely, the sectors that registered negative contributions were agriculture (-8,000) and information and communications (-108,000).

- Regarding occupational positions, the categories of worker, particular (formal) employee, and family worker without remuneration were the occupational positions that contributed most positively to the variation in the national total with +944,000 and +95,000, respectively.

- Regarding the quality of employment, most of the job creation was concentrated in the formal sector in June (+1,013,000 compared to June 2022), leading to an improvement in the informality index from 58.3% in June 2022 to 55.7% in June 2023, with urban areas showing the most significant progress, decreasing from 44.3% to 41.4% in June 2023.

In summary, the labour market displays a trend opposite to the most recent economic activity results, revealing that employment growth is concentrated in the services and commerce sectors, offsetting the weakening of other sectors such as agriculture. This indicates that the economy is undergoing a gradual and moderate deceleration process.

From a sectoral perspective, while there is an improvement in employment indicators, some sectors continue to face challenges. However, the overall quality of the workforce shows a positive trend in terms of formality and new job creation. With these results, the bank will enter a scenario of careful assessment.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

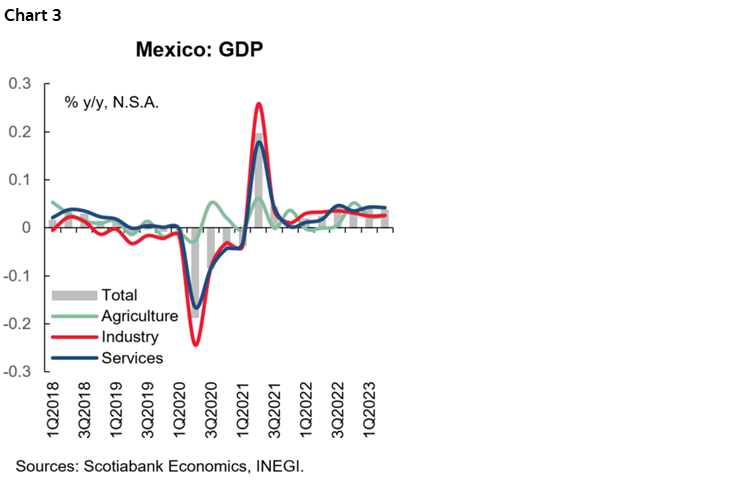

MEXICO: Q2 GDP BEATS THANKS TO STILL-STRONG SERVICES

The flash estimate for Mexican GDP for Q2 showed a repeat of Q1’s 3.7% y/y nsa expansion, above the 3.2% economist median (chart 3). By sector, services slightly moderated to 4.2% y/y (from 4.3% in Q1), but is still driving economic strength, industry picked up to 2.6% y/y (2.5% in Q1), and primary activities 2.5% (2.3% in Q1). Year to date, real GDP accumulates a 4.2% y/y increase. On quarter-on-quarter basis, economic activity rose 0.9%, also led by services, which rose 1.0%, followed by industry and agriculture, both up 0.8%. From the demand side, economic activity has shown a still-dynamic pace of private consumption, supported by a solid labour market, whereas investment remains somewhat stagnant, albeit some months showing advances and some medium-term positive nearshoring expectations. Analysts have positively revised 2023 growth expectations on the back of better-than-expected economic data, now anticipating an annual growth of 2.5%, implying the possibility of a slowdown in economic activity during the second half of the year.

PERU: JULY INFLATION COULD BE THE LAST CLOSE TO 6%

We expect July inflation to come close to 0.7% m/m, higher than that of June (-0.15% m/m), but lower than that of July 2022 (0.94% m/m) and with that being the case, the y/y rate would decline from 6.5% to 6.3%. Our forecast is above the official figure (5.9% of MoF) and the market consensus (5.8%), although overall we believe that inflation is likely to be close to 6%. Official data will be released on Tuesday, August 1st.

According to our monitoring of key prices, we see a recovery in poultry prices after a sharp decline in prices in June and increases in the prices of perishable foods and fruits, which would offset the decline in fuel and fish prices. Core inflation would be around 0.6% m/m, driven by seasonal factors, going from 4.3% to 4.2%.

Starting in August, the base effects for comparison will already be marginal, so we anticipate that the annual rate of inflation will stabilize around 6%. It is likely that the prices of perishable foods will remain under upward pressure and will continue to reflect the effects of the El Niño phenomenon and that the prices of fuels will also climb, because of the increase in oil prices of recent weeks. The BCRP remains cautious, in monetary pause mode during the last six months, and we expect it to continue in that stance until inflation does not fall with greater conviction.

—Mario Guerrero

PRESIDENT BOLUARTE’S INDEPENDENCE DAY ADDRESS STRESSED BUSINESS AS USUAL

Every July 28th (Independence Day) Peru’s current President gives their annual address to the nation. In the past this has sometimes included dramatic announcements of reforms and/or cabinet shakeups.

This year there was little drama. If anything, President Dina Boluarte’s very long (over three hours) speech gave the impression that the status quo is to be maintained. This is not a minor issue, however, given the recent political turbulence. What this means is that early elections are not on the agenda and, in fact, are not even considered an issue. Secondly, she noted that relations with congress will be as amiable as possible. Third, social conflict and social issues are taking a back seat to day-to-day public management as the focal point of government time and activities. Furthermore, no cabinet member was removed. None of this is very exciting stuff, but it is comforting in that it does favour an increasing sense of stability.

The government’s priorities have not changed much. Perhaps the main stress of Boluarte’s address was security. She announced that the government will be seeking special powers from congress to legislate on this front.

President Boluarte also reiterated the concern the government has regarding the likely El Niño weather event that we are all expecting for 2024, and repeated that emergency measures will be put in place to lessen its impact.

Economic priorities have also not changed, with emphasis on growth stimulus through spending programs (Con Punche Peru programs), in addition to various formulations to promote investment in infrastructure. The first is short-term and ongoing, the second is longer-term and rather incipient. None of this is new, however, except for augmented figures and details given here and there. One would have liked to have heard more on plans to stimulate private investment, which continues in the doldrums. Alas, this was lacking.

Bottom line, little has changed, and the country is likely to continue with a semblance of relative stability and very low growth.

Another issue of note: protests had been called for multiple occasions in July (July 14th regional strikes; July 22nd concentration in Lima; July 27th to July 29th, attempt to disrupt Independence Day celebrations). However, only very minor protests occurred. It is difficult envisioning a significant resurgence of protests, despite the low popularity of the Boluarte regime, for the following reasons. The leadership of the protests have lost legitimacy due to the violence of past protests, and to the radical demands that they continue to include in their platforms. The second reason is the workings of democracy itself. Elections will be held in 2026, after which the current government will be no more. For many people, it’s simply a question of being patient, rather than taking to the streets. Furthermore, one does not need to like the government to prefer a spell of stability versus the eternal fear that strikes Peruvians to the core every time there is a change in government, namely, what could follow?

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.