- Chile: The BCCh cut the benchmark rate by 100 bps (to 10.25%). We continue to see it at or below 7.5% by December 2023; No job creation in June, while unemployment rate remained at 8.5%

CHILE: THE BCCH CUT THE BENCHMARK RATE BY 100 BPS (TO 10.25%). WE CONTINUE TO SEE IT AT OR BELOW 7.5% BY DECEMBER 2023

- The process of cuts begins aggressively, owing to downside surprises to core inflation.

On Friday, July 28th, the Central Bank (BCCh) held its monetary policy meeting, initiating the process of cuts in the reference rate somewhat more aggressively than expected by consensus, indicating that in the short term it will continue with reductions higher than those of the base scenario and more in line with the lower part of the rate corridor. This confirms our view that we have been indicating since the beginning of this year. For the September meeting it seems clear that the BCCh will further cut by 100 bps and would only reduce the pace of cuts in the last meeting of the year conditional on no further falls in activity and inflation.

At Scotiabank Economics, we see economic activity more likely to surprise negatively relative to BCCh expectations (at -0.2% for 2023), while we project inflation to largely match their expectations (3.7% by December 2023), with risks somewhat tilted to the downside. In that context, we see the benchmark rate no higher than 7.5% by December 2023, which is consistent with two additional 100 bps cuts, and a likely reduction in the pace of cuts only at the December meeting.

What surprises us positively is the achievement of unanimity for this aggressive cut given the absence of unanimity at the last meeting. This would confirm that there is a consensus diagnosis that the pace of cuts needs to accelerate as inflation (and at Scotiabank we also consider economic activity) is slowing more rapidly. In effect, unanimity is returning to the Board’s decisions, with greater conviction about the weakness of the economy, so it is necessary to make up for lost time.

While headline inflation was known to have surprised to the downside in recent months, mainly in June, the Board reports a surprise in core CPI with respect to the most recent IPoM. As long as expected, annual goods inflation has fallen rapidly thanks to the stability of the real exchange rate, contrary to the depreciation expected by the BCCh in the last IPoM. This element largely explains the difference with respect to the baseline scenario, according to the statement. At Scotiabank, we continue to project a faster inflation convergence, which would be around the 3% target as early as Q1-24.

We reaffirm our view that the benchmark rate will end the year in the 6.5–7.5% range, returning to neutral by mid-2024 at the latest. We reiterate that the nominal neutral rate will be revised upwards in the September IPoM, increasing it by 25–50 bps to 4.0–4.25%. The above will also determine the pace of cuts required to reach the new level of the neutral rate by mid-2024, and after total inflation is at or below 3% in the middle of the first half of the year.

NO JOB CREATION IN JUNE, WHILE UNEMPLOYMENT RATE REMAINED AT 8.5%

- Stabilization of the labour market with public services demanding private employment. Construction deepens deterioration.

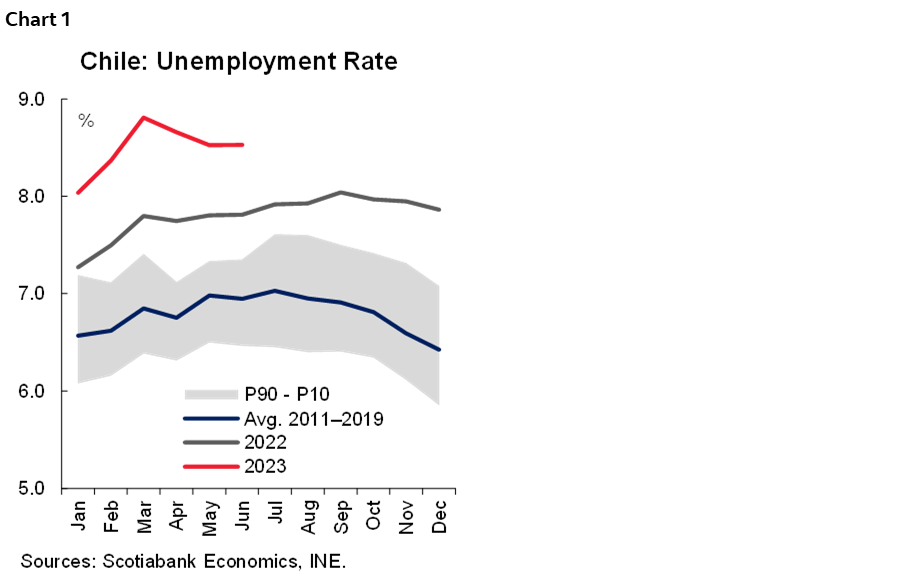

On Friday, July 28th, the statistical agency (INE) released the unemployment rate for the quarter ending in June, which remained at 8.5% (chart 1). This was explained by a stabilization in both the labour force and employment, both with marginal increases with respect to the previous quarter.

At the sectoral level, there is an increase in employment in the public service sectors compared to the previous quarter, such as public administration (+19k), education (+21k) and health (+9k), in persons reporting to be private salaried. These are probably private companies providing services to the state in the public administration sector and also an increase in employment in the education and private health sectors. This contrasts in part with what was observed at the beginning of the year, where job creation in these sectors was also significant, but in people who reported being public salaried.

On the other hand, the commerce sector reversed much of the job creation observed in May. As we anticipated, the unusual increase in employment in the commerce sector in May (+66k) was a transitory phenomenon, which did not correspond to the weak activity figures shown by the sector. Thus, 20k jobs were lost in June, most of them salaried, reversing part of what was created in May. The outlook for employment in this sector remains linked to the weak performance expected for economic activity in the coming months, mainly for consumption.

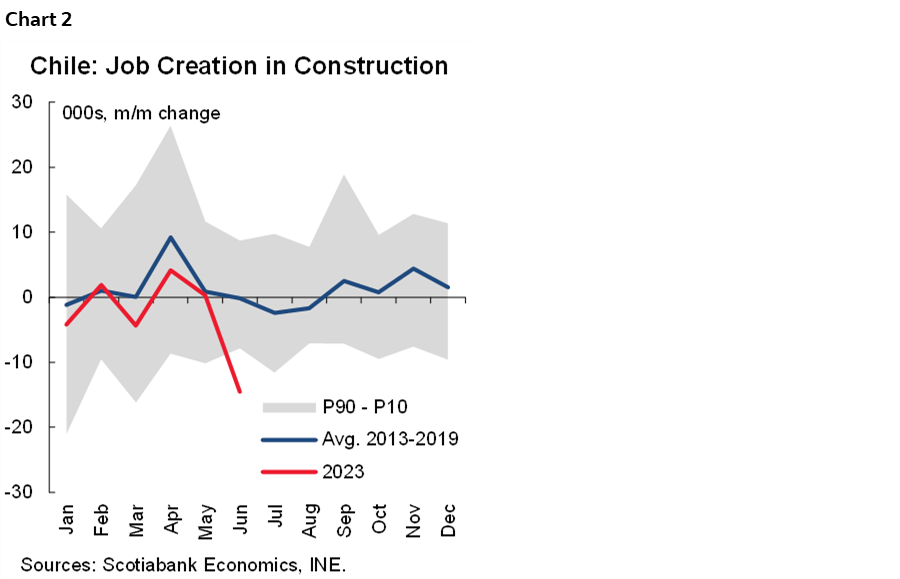

Construction destroyed 15k jobs, reflecting the slow progress of private and public investment (chart 2). The absence of new investment projects and the slow progress of existing projects is reportedly strongly affecting job creation in this sector. With figures as of May, the execution of public investment in health and public works shows relevant delays, while housing has advanced at a rate similar to the historical rate. Most of the jobs that were lost this month were salaried, showing a much greater deterioration than the seasonal trend.

—Aníbal Alarcón

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.