- Chile: Labour market narrows employment gap vs. pre-pandemic

- Colombia: Employment shows strongest monthly rebound since September 2020; closing gaps vs. pre-pandemic

- Mexico: Quarterly Inflation Report highlights stronger growth; fiscal accounts show improvement over 2021

- Peru: Government unveils a “steady as she goes” budget

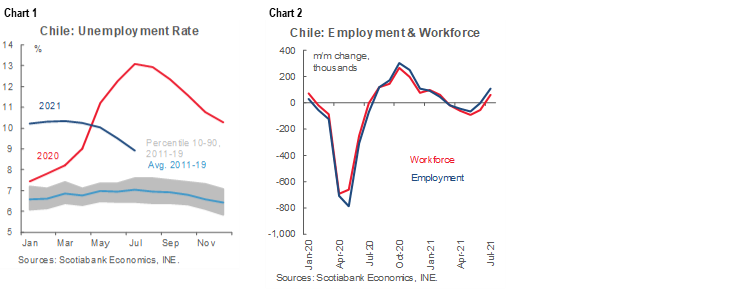

CHILE: LABOUR MARKET CREATED 108 THOUSAND JOBS IN JULY, NARROWING THE EMPLOYMENT GAP COMPARED TO PRE-PANDEMIC

On Tuesday, August 31st, Chile’s statistical agency, INE, released the country’s updated unemployment rate, showing a drop to 8.9% in the quarter ended in July (Bloomberg: 9.2%), as workers returned energetically to the labor market, especially informal workers (chart 1). The drop compared to the previous month reflects a higher growth in employment (1.3%) in relation to that observed in the workforce (0.7%). Employment grew again (+108 thousand), after four consecutive months of falls or null variations. However, the figures show that most of the new jobs are informal (104 thousand) while only four thousand of them correspond to formal jobs. Nonetheless, the increase in employment was the largest since December 2020 (chart 2). It should be remembered that, with the extension of the Universal Emergency Family Income (IFE) until the end of the year, the Government proposed the creation of 500,000 new formal jobs during the remainder of the year.

July’s figures narrow the employment gap against pre-pandemic levels, as these dropped to 914 thousand jobs, of which 476 thousand are formal jobs (52% of the total) and 439 thousand are informal. We believe that a part of the remaining gap will begin to recover (mainly in informal ones), given the fewer restrictions imposed by authorities in recent weeks, due to the drop in COVID-19 cases.

On the other hand, fiscal spending had a new record expansion last month, anticipating strong economic growth for July. According to figures from the Budget Office, total spending expanded 59.7% y/y in real terms in July, its highest increase so far this year, highlighting the growth of current spending (+65.7% y/y) which was partly explained by the implementation of the IFE Universal. All in all, we expect July’s economic activity index (Imacec) to grow 17% y/y (+1.0% m/m).

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

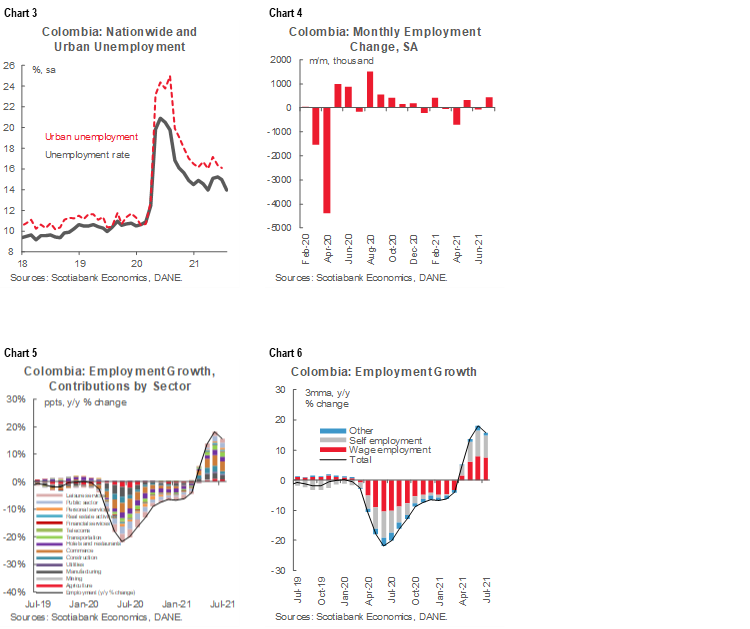

COLOMBIA: EMPLOYMENT SHOWS STRONGEST MONTHLY REBOUND SINCE SEPTEMBER 2020; CLOSING GAPS VS. PRE-PANDEMIC

As Colombia advanced with vaccination rollout, major cities allowed more activities to operate, which was reflected in a monthly creation of 434 thousand jobs, constituting the best rebound since September 2020. That said, up to July total active jobs are down by 1.23 million (-5.5%) relative to July 2019, which pointed to a significant improvement from June´s data, when the lag was 1.9 million people (~8% below pre-pandemic levels). On the other side, the inactive labor force fell by 227 thousand (the best reduction since august 2020) and now is just 8.7% above from pre-pandemic levels. The main contributions came from job creation in main cities, which also contributes to close somewhat gender gaps and improve formality metrics.

From a sectoral perspective, services-related sectors were the best performers amid the almost complete normalization that is taking place, around 52% of yearly employment gains came from commerce (+644 thousand y/y), hotels and restaurants (+447 thousand), and leisure (+426 thousand), those sectors have relevant participation of women labor force, which contributes to close some gender gaps. It is worth noting that employment losses as of July 2021 versus pre-pandemic levels remained concentrated in four sectors: Manufacturing (-281 thousand), especially in the clothing sector; leisure (-264 thousand), and commerce (-205 thousand). We think those gaps will continue closing as regional leaders allow yet more activities such as massive events. Additionally, people returning to the office and schools would lead to better demand dynamics.

Earlier negative trends are now improving:

1. Female Participation: the wider gap between the female unemployment rate (18.6%) and male rate (10.9%) is narrowing, as the rebound in services sectors and children going back in school are allowing women to participate more in the labor force.

2. Formality: formality is improving, evidenced by the 57% of employment attributable to formal jobs in July, while self-employment contributed with 38%. Informality is also moderating, for urban areas (13 major cities) informality is around 46.3%, while for a wider sample (23 cities) it is 47.5%.

Summing up, July showed an overall recovery in the labor market, showing that now services sectors are leading the gains and are contributing to close somewhat the gender gap and to improve formal jobs. We expect the labor market to continue gradually improving, as major cities are now broadly operating normally. In addition, the vaccine roll-out is now available for children above 12 years which would lead to a better dynamic in the education sector in terms of job creation but also allowing women to return to the labor market.

—Sergio Olarte & Jackeline Piraján

MEXICO: PUBLIC FINANCES SHOWED A LOWER THAN PROGRAMMED DEFICIT IN JANUARY–JULY AS REVENUES SURGE HIGHER THAN EXPENDITURES YTD IN REAL TERMS

I. Public finances improve as revenues surge

According to data published by the Ministry of Finance and Public Credit (SHCP), in the months from January to July 2021, the public sector balance reported a deficit of MXN -242.67 billion pesos (USD -12.1 million). This deficit was MXN 205.2 billion lower than expected and lower than the MXN -414.64 billion deficit in the same period a year ago as a result of higher revenues but also lower expenditures than programmed. The primary balance recorded a surplus of MXN 132.92 billion (USD 6.6 million), above the deficit of MXN -15.19 billion programmed for this period.

Looking at the details:

- Public revenues totaled MXN 3.409 trillion (USD 170 billion). This figure is 3.5% higher than programmed, and represents an increase of 8.2% YTD in real terms. Oil revenues, about 15% of total revenues, rose 59.8% YTD in real terms owing to the strong recovery of oil prices y/y. Non-oil revenues surged 2.4% YTD, as tax revenues rose 2.3% thanks to 12.6% in VAT despite the drops of -0.7% and -8.3% in income taxes and production, respectively. Non-tax revenues soared 18.5% owing to the use of financial assets.

- Total expenditures amounted to MXN 3.689 trillion (USD 183.9 billion), marginally below the programmed amount for the period, yet 2.1% YTD above a year earlier. In particular, programmable expenditures counted for 73.9% of the total and rose 4.6% YTD in real terms. Non-programmable expenditures dropped -4.3% YTD in real terms.

- Finally, the Public Sector Borrowing Requirements registered a deficit of MXN 434.3 billion (USD 21.6 million). Thus, the broader measure of public debt, Historical Balance of Public Sector Borrowing Requirements (SHRFSP) totaled MXN 12.498 trillion (USD 623.03 billion), equivalent to 50.8% of GDP.

In recent days, the president and the finance ministry indicated their intention to use the SDRs that the IMF provided to Mexico’s Central Bank (USD 112.117 billion) in order to pay public debt with high rates and reduce the amount of debt outflows. However, according to the Central Bank Constitutional Law, SDRs are considered part of the international reserves, meaning that in order to make use of them the federal government would have to buy them from Banxico at market prices. More information regarding FinMin and Banxico’s negotiations on this issue will be announced in the coming days, along with the fiscal budget, to be released on September 8th.

—Miguel Saldaña

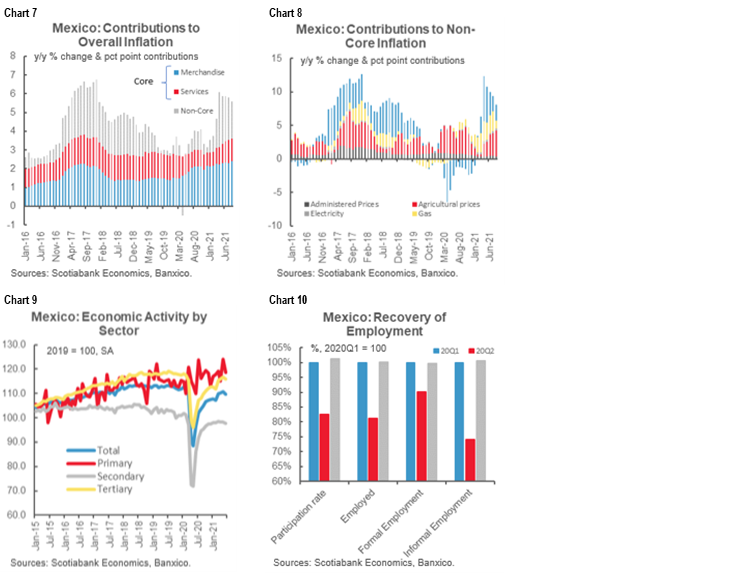

II. Banxico’s Quarterly Inflation Report inflation unchanged, faster growth

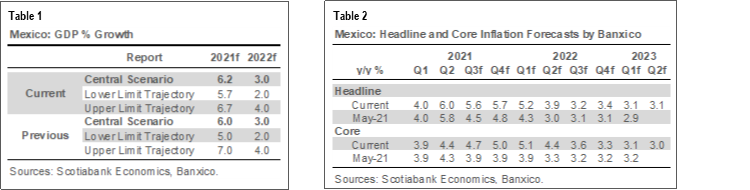

Banxico’s latest Quarterly Inflation Report (QIR) released August 31st offers little in terms of new forecasts but does add more clarity into the central bank’s current priorities. Given that Banxico had already made two upward revisions to its inflation forecasts from the May 2021 QIR, and the latest relatively benign print, which saw inflation drop about 20 bps, there were no changes in August. Notably, growth forecasts to 2021 were revised up based on the strong Q2 data. Banxico’s new central scenario envisions 6.2% growth for the year (we expect our own revised forecasts will land quite close to that), while Banxico anticipates 2022 growth at 3.0%.

Banxico’s current inflation forecasts see CPI converging to 20 bps above the midpoint of its 3% +/- 1 pp target by 2022 H2, within the central bank’s policy horizon. Because Banxico also estimates the output gap will be largely closed by the second half of 2022, we are calling for policy settings to move to neutral by the end of next year, at which point Banxico’s own forecasts suggest inflation will be close to target.

The latest estimate of the neutral policy rate we have from Banxico was published a couple of years ago. In it, the central bank suggests neutral policy settings would be consistent with real rates of 1.8-3.4 percent. We can either take the consensus long-run inflation or Banxico’s inflation target to proxy where neutral settings would end up as the economy moves closer to potential, which would mean a neutral nominal rate in the 5.85% to 6.1% range, depending on whether we take long run inflation estimates or Banxico’s inflation target. Our current forecast has Banxico rapidly moving its policy rate to 5.25% (which is still accommodative), followed by gradual tightening throughout 2022, leaving policy settings at neutral by the end of next year, which are consistent with the output gap being close to shut by the end of 2022.

We remain comfortable with our forecast, but acknowledge that communication from Banxico’s board members, alongside the arrival of former FinMin Herrera as Governor (his comments on monetary policy so far suggest he will lean dovish) point towards a skewing of risks towards a slower unwinding of stimulus than we currently expect. However, if tightening falls behind inflation, resulting in lower real policy rates, there is a risk that inflation could become self-sustaining, which suggests a more gradual rate hike path might risk a higher terminal rate.

In terms of the Report’s focus, there is a fair amount of work dedicated to evaluating the impact of the pandemic’s supply chain disruptions on overall economic activity levels as well as prices. Key highlights include:

- Non-core inflation was contained by price caps on residential gas, although these caps are described as temporary. Non-core inflation’s contribution to headline has been steadily declining since their peak at the end of Q2.

- Core inflation dynamics have been the main drivers of upward price momentum. Even though a large part of price spikes is driven by supply chain disruption, the broad-based rise warrants caution given it is running at twice the target level. In addition, Banxico also focused on the longer than anticipated deviation of inflation from its target.

- The other driver of earlier than expected rate hikes was the deterioration in expectations, including Banxico’s own. After two upwards revisions to the central bank’s own forecasts since May, the latest QIR did not present any further deterioration in the central bank’s inflation forecasts. However, we did see a moderate upwards revision to GDP expectations for 2021, which implies an earlier closure of the output gap.

- Banxico estimates that the microchip scarcity shock to the auto industry reduced production by about 380k in the first half of the year and could reduce production by about 450k-650k in the second half. For GDP, the impact from the auto sector supply disruptions is estimated to be between 70 bps and 100 bps of growth in 2021.

- Most of the labor indicators tracked by Banxico show the labor market has recovered to levels seen before the onset of the pandemic. Consistent with this, Banxico’s estimate of the labor market “gap” shows virtually no slack is left in the labor market (0.5% slack vs a peak of 15.5% seen in the summer of 2020).

- The QIR spends some time discussing the anticipated trajectory of monetary stimulus unwinding in both the advanced and emerging world, consistent with its recurring references to “relative monetary conditions” in past monetary policy decision statements. This monitoring of other central bank actions could, on the margin, help explain the earlier tightening as “insurance” against any capital flow disruption from the Fed’s tapering (estimated around year-end). In this regard, Banxico’s pre-emptive rate hikes could help reduce financial volatility risks around year-end.

- In terms of the economy, Banxico sees a multi-speed recovery in output, with the output gap virtually closed by the end of next year.

—Eduardo Suárez, Miguel Saldaña & Paulina Villanueva

PERU: THE 2022 BUDGET—STEADY AS SHE GOES

The Ministry of Finance, MEF, released its 2022 fiscal budget plan, public debt program and its yearly multi-annual fiscal policy framework document, Marco Macroeconómico Multanual, MMM, over the last few days. The next step is for the budget to be discussed within the Congressional budget committee. Congress then has to approve the budget by December. If precedent holds, Congress will introduce modifications without materially affecting the basic guidelines of the budget.

The 2022 budget totals PEN/197 bn (approximately USD48 bn) and represents a moderate 7.6% increase over the initial 2021 budget. This will require a PEN/ 38 bn (USD9.5 bn) increase in debt, including PEN/ 30.6 bn (USD7.7 bn) in sovereign bonds issuance. This would be lower than the PEN/ 41.9 bn by which the debt increased in 2021. Frequently, the actual debt requirements surpass the initial budget allowance, although normally not by a huge amount.

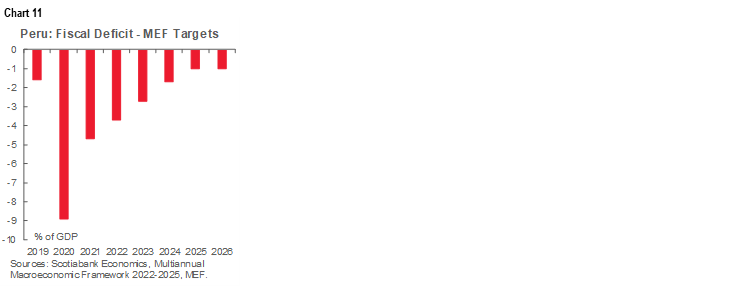

According to these documents, the MEF estimates that the 2022 Budget will allow for a decrease in the fiscal deficit from 4.7% of GDP 2021 to 3.7% in 2022. As a result, the public sector debt in 2022 will reach 36.6% of GDP. The MEF was keen on stressing in these documents the government’s intention to meet the fiscal rule long-run target of a 1.0% fiscal deficit by 2025.

The MEF is forecasting 4.8% GDP growth in 2022, which greatly surpasses our own forecast of 2.6%. The greatest difference is not discounting due to confidence issues resulting from policy and political uncertainty.

The two sectors which will see the greatest budget increase are education, 7.9% higher, and health, 5.8%. The Budget includes a 3.2% increase in government spending, in real terms. Public investment will rise 6.7%, in real terms.

What appears to be lacking from the new budget, interestingly enough, is any mention of an increase in taxes on mining, or other tax reform measures. However, this may simply reflect lack of time to structure a proposal for inclusion in this version of the budget. The overriding message is that this is a budget that is reasonable and more prudent than we might have expected. Following COVID-19 and Peru’s lockdown last year, any government would have needed to contend with a certain amount of fiscal deterioration. Outside of the normal concern one may have over this, there is otherwise nothing untoward or exceptional in the 2022 budget. The weight of the MEF as an institution appears clearly in the budget’s design. This is not a budget that is all that different from budgets in the past.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.