- Colombia: Annual inflation again neared 2% y/y in April as major prices continued to normalize

COLOMBIA: ANNUAL INFLATION AGAIN NEARED 2% Y/Y IN APRIL AS MAJOR PRICES CONTINUED TO NORMALIZE

April price data, published late on Monday, May 5, by DANE, put sequential inflation at 0.59% m/m sa, once again well above both market consensus (BanRep and Bloomberg surveys: 0.32% m/m) and Scotiabank Economics’ own projection (0.29% m/m). Foodstuff inflation, along with the lodging and utility groups, contributed the most to the positive surprise, which took monthly inflation up from 0.59% m/m in March. This moved annual headline inflation up from 1.51% y/y in March to 1.95% y/y in April (chart 1), just below the 2–4% y/y target range—which puts in sight our 3.1% y/y forecast for end-2021.

Core inflation stood at 0.30% m/m sa, also above the BanRep market survey consensus of 0.22% m/m and up from 0.39% m/m in March. This reflected further upward price pressures amongst key components of Colombia’s consumer basket—a signal of the strengthening economic environment and further normalization of prices. April’s month-on-month inflation rate was the highest for any April in the last five years and 17 bps above the mean of the previous five years. Annual core inflation increased from 1.06% y/y in March to 1.56% y/y in April (chart 1, again).

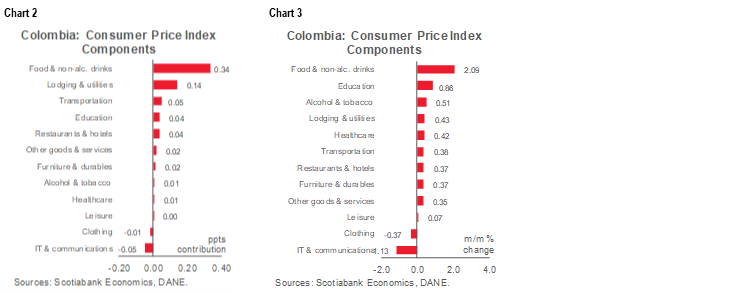

Looking at the April numbers in detail, 10 out 12 sectors contributed positively to the monthly inflation print (charts 2 and 3). Some prices strengthened upward trends observed in previous months, pointing to a consistent re-setting of markets affected by the pandemic.

- Food and non-alcoholic beverage prices made the strongest contribution to month-on-month inflation with 34 bps on a sectoral price gain of 2.09% m/m: meat (11 bps and 5.3% m/m); potatoes (6 bps and 18.8% m/m); and fruits (3 bps and 3.14% m/m) were the main contributors of the group. Export dynamics in the meat sector were the main driver of its upward price pressures. Nationwide strikes in recent days are likely to lead to significant increases in some prices in May owing to blockages in key national roads.

- The lodging and utilities group was the second-largest sectoral contributor to April’s inflation reading (14 bps on a 0.43 % m/m rise in prices).

- Utility charges made a 9 bps contribution to April’s month-on-month inflation owing mainly to adjustments in electricity fees. Rental fees added 5 bps, which is a major signal of some normalization in prices that have been heavily affected by the pandemic.

- Other sectors, such as transport (5 bps and 0.38% m/m), education (4 bps and 0.86% m/m), and restaurants and hotels (4 bps and 0.37% m/m), also added to April’s price gains. Education’s contribution represented a special case since, in a normal April, these prices would be unchanged; however, the sector is currently moving rates and fees back toward its pre-pandemic levels.

- On the negative side, prices for IT and communications fell (-5 bps and -1.13% m/m) owing to better fees on mobile plans. A new player in the sector has launched its service at lower prices and incumbent companies have responded by lowering their tariffs as well. In the same vein, clothing group prices also softened (-1 bps and -0.37% m/m) amid weaker demand due to the lockdowns during weekends in Colombia’s main cities.

Looking at annual inflation across major categories, price gains accelerated across the board. Goods inflation increased to 1.21% y/y (versus 1.05% y/y in March), services inflation also rose by 36 bps from 0.89% y/y to 1.25% y/y, and regulated-price inflation accelerated by 127 bps to 2.79% y/y, the highest print since April 2020. As previously noted, core inflation rebounded: ex-food inflation came in at 1.56% y/y (up about 50 bps from March), while inflation exclusive of food and regulated prices increased by 30 bps from March to 1.24% y/y in April. Low-income households continued to face greater annual inflation (2.28% y/y) than high-income households (1.45% y/y).

April’s inflation numbers provided clear signals that key prices are normalizing as both the headline and core measures accelerated. The April results increase the likelihood that annual headline inflation will move above BanRep’s 3% y/y target by the end of 2021. At present, the upper bound of the central’s bank forecast for year-end inflation is 3.5% y/y, which supports our expectation that the BanRep Board will initiate a hiking cycle later this year. We anticipate that policymakers will keep the benchmark rate on hold at 1.75% until at least September 2021, when we project a first hike to be implemented.

—Sergio Olarte & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.