- Chile: New fiscal package of 4% of GDP to be financed mainly with more debt issuance abroad

- Mexico: Banxico minutes a touch more dovish than expected; both unemployment rate and jobs rose in April

- Peru: Government announced new stimulus measures; Castillo renewed vow to dissolve private pension fund system

CHILE: NEW FISCAL PACKAGE OF 4% OF GDP TO BE FINANCED MAINLY WITH MORE DEBT ISSUANCE ABROAD

On Wednesday, May 26, the government announced a new fiscal package worth 4% of GDP (equivalent to approximately USD 11 bn). The initiative contemplates emergency transfers for three months (Jun.–Aug.) to lower-income families, a USD 2 bn support fund for SMEs with sales below USD 1 mn, and other minor measures. The political opposition still considers this new fiscal package insufficient for Chile’s needs, so we expect to see negotiations over the coming days that could result in some increase in the scale of the proposed measures, especially the support for SMEs. Regarding the three months of direct transfers to families, these would be renewable if public-health or economic conditions warrant it. The financing of this new fiscal package has not been disclosed by the government, but our estimates imply that it would require new sovereign debt issuance abroad and moves to tap the sovereign wealth fund. The resources of the sovereign wealth funds are, however, already committed to financing the government’s earlier fiscal packages, so we believe that any engagement of the funds would involve debt placements.

—Jorge Selaive

MEXICO: BANXICO MINUTES A TOUCH MORE DOVISH THAN EXPECTED; BOTH UNEMPLOYMENT RATE AND JOBS ROSE IN APRIL

I. Banxico minutes a touch more dovish than expected; short-end TIIE maintains downward bias

Banxico published on Thursday, May 27, the minutes of its May 12 monetary policy meeting where the Board of Governors unanimously maintained the benchmark interest rate at 4.00%. We noticed a more dovish bias in the minutes than we or consensus had expected; this strengthened our view that Banxico’s benchmark policy rate shall be held unchanged through the end of the year. We continue to forecast a first rate hike in Q1-2022. TIIE pricing concurred, with 1-year rates maintaining their declining bias.

The minutes noted that the unanimity of the decision does not mean that all members anticipated a tighter stance in the near future. Although, the majority of Board members believed that a “prudent” approach to monetary policy should be maintained to ensure the convergence of inflation toward Banxico’s 3% y/y inflation target, members didn’t seem to see the current inflation spike as a risk to getting inflation back within the target over their forecast horizon—even though risks to growth are now more balanced and inflation risks have titled up. Two of the five Board members noted that inflation risks are principally transitory. The text noted that one Board member still saw room for a more accommodative monetary stance owing to a decline in the neutral rate, but even this member saw a pause in rate changes as justified.

Regarding the discussion on external developments, the Board mentioned the heterogeneity of the pace of recovery worldwide, which continues to depend across countries on the availability of vaccines and fiscal stimulus. This uneven recovery could cause ongoing disruptions in supply chains, posing an upside risk to the prices of some products. However, we have previously heard a member of the Board indicate that monetary policy is not a particularly effective mechanism to combat supply-side price pressures. In terms of the speed of global recovery, emerging economies are expected to return to pre-pandemic levels of economic activity by 2023, while the United States could reach its 2019 production levels by end-2021; a weaker recovery for economies in Europe and Japan is anticipated.

With respect to international monetary policy, Board members made some comments which suggested that, despite recent increases in inflation, they did not expect the US Fed’s FOMC to raise interest rates until 2023 nor undertake tapering in the Fed’s asset purchase programs this year, although a shift toward a more restrictive stance is a latent risk. Regarding emerging economies, Board members mentioned that some central banks have begun to pare their monetary stimulus and adopt tighter policies owing to exchange rate and/or inflationary pressures—particularly monetary authorities that may have been too aggressive in loosening during the pandemic’s peak. One of the members noted, however, that this was not the case in Mexico, because stakeholders have acted relatively cautiously and prudently. Capital flows were also discussed, although most members stated that financial markets were now exhibiting more orderly behaviour and that the enthusiasm for higher yielding US securities has stabilized. Another member noted that amongst emerging markets, fixed-income inflows continue to improve, while China remains the main destination for allocations into equity assets.

On the domestic economy, the Board highlighted that the recovery has been differentiated across sectors and regions; members also made reference to the moderation in the recovery observed in the first two months of the year, which they described as a temporary phenomenon driven mainly by the new round of restrictions related to the most recent wave of COVID-19. Still, Board members underscored that the main driver of the economic recovery continues to be the external sector, while consumption has slowly reactivated, supported by record inbound remittances. In contrast, investment continues to be soft and growth expectations are low due the prevailing sense of uncertainty in the business sector. On the labour market, the Board noted that it has been recovering, although it still remains below pre-pandemic levels. Overall, most Board members perceived the risks to growth as more balanced. Among the upside risks, they mentioned an increase in external demand, while on the downside, they highlighted uncertainties associated with the pandemic and possible delays in the vaccination process.

The Board noted that the balance of inflation risks are skewed to the upside. The Board considered that the near-term rise in inflation is transitory and driven primarily by base effects in energy prices—although core commodity price pressures are also present. Thus, members continued to see inflation converging towards the 3% y/y target by Q2-2022. Looking ahead, the priority would be to ensure that inflation expectations remain anchored and that headline and core inflation converge to the target within the time horizon in which monetary policy operates.

Risks to price stability include, on the upside, higher external inflation, as well as cost pressures from spending reallocations and possible episodes of exchange-rate depreciation. Additionally, most members highlighted risks posed by the drought on some food prices. In line with our forecasts, some Board members foresaw greater inflationary pressures in the services sector as public-health restrictions are lifted. Regarding downside risks, most mentioned the negative output gap: one of the members even highlighted the risk of further physical-distancing measures—which seems unlikely in our view—while another added that gasoline prices have stabilized so that going forward their contribution to inflation should be more limited.

—Paulina Villanueva

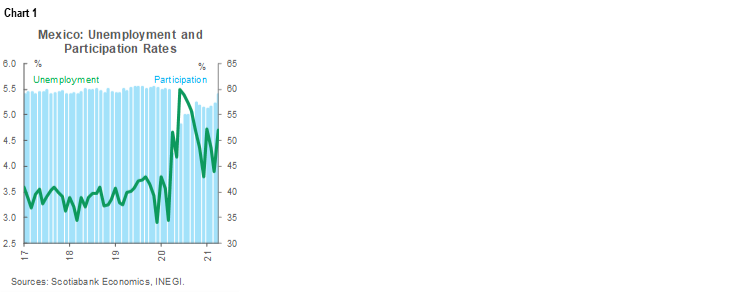

II. Unemployment rate went up in April, despite one million created and lower informality

According to the ENOE results released by INEGI on Thursday, May 27, the labour market in April remained strongly affected by the pandemic, but we got a positive sign from an increase in participation. In April, the Economically Active Population (PEA in Spanish) rose to 57.5 mn people or 59.05% of the total population (chart 1), up from 57.2% in March—and a big gain of 12.7 mn people and 11.6 percentage points from April 2020’s shutdown-affected levels. Still, April’s participation rate remained below the 60% recent peak observed in March of 2019. In the details, moving from March to April 2021, some 1.05 mn jobs were created, which lifted the employed population by 54.84 mn. However, the unemployment rate also went up, from 3.9% in March to 4.7%, roughly the same as in April 2020 (chart 1, again). Regarding the employed population, 13.7% was looking to work more hours (i.e., they are currently in part-time jobs), and the share of informal employment was 55.59%; these figures compare with April 2020’s 25.40% share in part-time jobs and 47.89% informally employed. Prior to the pandemic in March 2020, the share of people looking to work more hours and labouring in informal sector were 9.12% and 55.68%, respectively. The share of informal workers fell during the peak of the pandemic since layoffs and firings are easier in unregulated workplaces.

The April labour-market numbers remained consistent with a slow—but steady—pace of recovery. They were broadly in line with our forecast of a weak trend in private-consumption growth through the first half of 2021. Employment and consumer activity may both pick up as the vaccination process moves ahead in Mexico and fosters a broader reactivation of activities and job creation.

—Miguel Saldaña

PERU: GOVERNMENT ANNOUNCED NEW STIMULUS MEASURES; CASTILLO RENEWED VOW TO DISSOLVE PRIVATE PENSION FUND SYSTEM

I. Government announced new stimulus measures

The Minister of Finance, Waldo Mendoza, announced on Thursday, May 27, that the government was preparing stimulus and health measures to the tune of PEN 1.2 bn (USD 315 mn) that would be geared toward “vulnerable sectors”. The proposed breakdown would be as follows: PEN 388 mn in funds for COVID-19 health, vaccinations, and infrastructure; PEN 218 mn in household safety net programs; PEN 405 mn to stimulate greater economic growth; and PEN 220 mn to boost the Trabaja Perú temporary employment program. These resources should help counter, to at least some extent, the negative impact of political uncertainty on economic activity. Much of the effects of the proposed measures would be felt after the change in government in August.

II. Castillo renewed vow to dissolve private pension fund system

Presidential candidate Pedro Castillo reiterated on Thursday, May 27, his position that, if elected, his government would dissolve the private pension fund system. What was new, however, was the statement that a new workers’ bank would be created to take over pensions, although it was not clear how this would operate. The statement renewed speculation on just how a Castillo Government would go about eliminating the AFP system, whether this would be an orderly and legal process over time, or a more disorderly move that could affect property rights of fundholders and provoke legal challenges.

Meanwhile, this week, the process for the most recent round of pension withdrawals began. People with assets in the pension fund system may withdraw up to PEN 17,600 (USD 4,500). According to the banking superintendent, potentially as much as 23%, or PEN 38 bn (USD 10 bn), of a total of PEN 160 bn in assets could be withdrawn over the course of the next four months. In past rounds of withdrawals, part of the funds pulled out helped to uphold consumption, part was used to pay down household debt, and part augmented personal savings accounts. The risk now is that a much greater portion of withdrawn funds will seek safe havens given the current level of political uncertainty. This would include the purchase of USD, and, quite possibly, transfers abroad.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.