Colombia: BanRep held its benchmark monetary-policy rate at 1.75% in a unanimous vote with a hawkish tone

Mexico: Large trade surpluses returned in February

Peru: New poll favours Lescano in a very close race

COLOMBIA: BANREP HELD ITS BENCHMARK MONETARY-POLICY RATE AT 1.75% IN A UNANIMOUS VOTE WITH A HAWKISH TONE

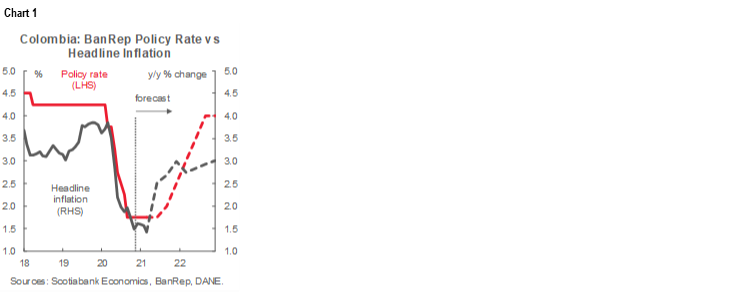

On Friday, March 26, the BanRep’s Board left its benchmark monetary-policy rate at 1.75%, as expected by both ourselves and market consensus—in a unanimous vote amidst better growth forecasts, anchored inflation expectations, and still favourable, but tightened, international financial conditions. Governor, Leonardo Villar underscored in the press conference following the meeting that the Bank's monetary policy stance remains very expansionary and continues to support the economic recovery. Also, Gov. Villar highlighted that BanRep’s current countercyclical monetary policy would depend on the approval of a fiscal-reform package, which is essential to guarantee the medium-term sustainability of public finances.

Some key features of the decision included:

- From the communiqué, we noted that the BanRep staff revised its 2021 real economic growth forecast upward from their previous 4.5% y/y to a preliminary projection of a 5.2% y/y expansion. Governor Villar emphasized that the impact of January’s lockdowns had been less significant than expected by the staff and that data for Q4-2020 showed better-than-projected dynamics. Therefore, the central bank staff’s improved view of economic growth and its upward revision on inflation (n.b., they didn’t provide the specific numbers in the press conference) point to changes in the staff’s anticipated interest-rate path in the forthcoming quarterly Monetary Policy Report (expected to be released after April’s meeting);

- The communiqué underscored a vigilant stance from the Board with respect to international market developments since increasing international rates can affect Colombia’s financial conditions. In the press conference, Villar highlighted that the Biden Administration’s fiscal package constitutes a risk for sooner-than-expected rate hikes from the Federal Reserve; the pricing of this possibility has led to higher rates in markets that could imply some challenges for Colombia’s future efforts to finance itself;

- Fiscal reform is in the BanRep’s spotlight. In the communiqué and the press conference, Villar emphasised that fiscal reform is key for the sustainability of public finances and warned that monetary policy couldn’t continue providing counter-cyclical support to the Colombian economy if a fiscal-reform package isn’t approved; and

- International reserves and a response to the IMF’s suggestion that they be increased by USD 3 bn. Governor Villar said that IMF efforts to revise its scheme of Special Drawing Rights (SDRs) could see countries such as Colombia increase its reserves automatically without going to the market.

To sum up, BanRep’s decision to hold was in line with market projections, but it was tilted to the hawkish side, as better economic growth forecasts, higher inflation projections, and changing international financial conditions provided arguments for considering the possibility of increased monetary-policy rates in the future. The minutes of the meeting, due to be published today, March 29, will be key to understanding how the Board’s members skew on these issues. Similarly, the April Monetary Policy Report will be eagerly awaited for its updated staff macroeconomic forecasts and rate scenario.

We maintain our call that the BanRep will remain on hold over the coming months with the possibility of a first rate hike by Q3-2021 (chart 1). The lift-off in policy rates we anticipate later in 2021 would be predicated on further consolidation of the economic recovery, with inflation rising closer to the BanRep’s 3% y/y inflation target.

—Sergio Olarte & Jackeline Piraján

MEXICO: LARGE TRADE SURPLUSES RETURNED IN FEBRUARY

INEGI’s trade data for February, released on Friday, March 26, showed that Mexico returned to a large monthly trade surplus, with the print coming in at USD 2.681 bn, up from a deficit of USD -1.236 bn in January (chart 2). For reference, this year’s February surplus was modestly smaller than the USD 2.868 bn surplus we saw in the same month of last year, and so far puts the 2021 trade balance YTD at USD 1.445 bn. Although not to the same degree as we saw in the second half of 2020, net exports remain a strong positive driver of Mexican growth. Trade at the start of the year has been somewhat disrupted by semi-conductor shortages in the auto industry and the return of pandemic-induced shocks, but we expect the US stimulus package to support the Mexican economy through both the trade and remittances channels.

We look at the data in further detail.

- Monthly declines from January. February’s trade numbers reported a monthly decrease in total merchandise exports of -3.65% m/m sa which was the result of reductions of -3.67% m/m sa in non-oil exports and -3.28% m/m sa in oil exports; meanwhile total imports reported a monthly fall of -2.34% m/m sa, which originated from decreases of -2.53% m/m sa in non-oil imports and -0.22% m/m sa in oil imports.

- Exports still off a year-ago’s levels. In its annual comparison, Mexico exported USD 36.19 bn worth of goods, down -1.1% y/y compared with February 2020 (chart 2 again), which was the net result of a -1.7% y/y decrease in non-oil exports and a 10.7% y/y increase in oil exports. Within non-oil exports, manufacturing exports were down -2.7% y/y, dented mainly by the auto sector which posted a -10.0% y/y drop. Exports to the US were off -2.9% y/y in the second month of 2021: we believe that the February data were affected by the harsh winter that our main trading partner experienced.

- Imports closing gap versus 2020. The value of imports was down -0.6% y/y, better than the previous reading of -5.90% y/y, at USD 33.51 bn. This figure was the net result of a -9.9% y/y decrease in oil imports and a 0.3% y/y increase in non-oil imports. When considering imports by type of good, there was an annual reduction of -10.8% y/y in imports of consumer goods, while there were gains of 0.5% y/y in imports of intermediate goods and 4.8% y/y in imports of capital goods. Given the persistent weakness of private domestic consumption, we expect the recovery in non-oil imports to be gradual in 2021.

—Paulina Villanueva

PERU: NEW POLL FAVOURS LESCANO IN A VERY CLOSE RACE

Results of a new poll by a well-known local pollster, IEP (Instituto de Estudios Peruanos), were released to the news media on Sunday, March 28. The poll showed that Yonhy Lescano (Acción Popular) continues to lead with 11.4% of voting intentions, although this was down 2.5 percentage points from numbers published two weeks ago by the same pollster. Tied in second place were Rafael López Aliaga (9.7%) and Verónika Mendoza (9.6%), with Hernando de Soto (8.5%) and George Forsyth (8.2%) narrowly behind. Given the 2.8 ppts margin of error of the poll, Keiko Fujimori (7.9%) should probably also be included in the group of close contenders. Note that while most polls coincide with IEP’s in having Lescano leading, the order of the candidates that follow differs across them.

With two weeks to go before the elections, Yonhy Lescano has been leading in the polls more or less consistently, albeit with too small a margin to be assured that he will make it into the second round. Note that 27% of voters (voting is mandatory in Peru) are not satisfied with any of the candidates. A portion of these will deliver a blank vote, but most will likely move in the end toward some candidate or another. In view of the 3.5 point difference between the leader Lescano, and sixth place Fujimori, the race is still very much open.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.