Chile: S&P downgraded Chile’s sovereign ratings to “A” and revised its outlook to “stable”

Mexico: Banxico delivered unanimous hold at 4.00%; recovery pace remains gradual

Peru: Moody’s upgrades the outlook for Peruvian banks from “negative” to “stable”

CHILE: S&P DOWNGRADED CHILE’S SOVEREIGN RATINGS TO “A” AND REVISED ITS OUTLOOK TO “STABLE”

On Wednesday March 24, S&P Global Ratings lowered its long-term foreign-currency sovereign credit rating on Chile to “A” from “A+” and its long-term local currency rating to “A+” from “AA-”. S&P’s outlook on the long-term ratings changed to “stable” after having been “negative” since April 2020. S&P’s announcement comes the same day that Fitch affirmed Chile's long-term foreign-currency issuer default rating (IDR) at “A-” with a “stable” outlook. S&P also re-affirmed their short-term foreign currency sovereign credit rating at “A-1” and lowered their short-term local currency rating to “A-1” from “A-1+”. Finally, they also revised down their transfer and convertibility (T&C) assessment to “AA-” from “AA”.

The downgrade was based on the marked erosion of Chile’s public finances over the last 10 years, which are likely to stabilize at a weakened level once the pandemic recedes and the economy recovers to its trend pace of GDP growth. While the economic recovery should help to reduce recent, high fiscal deficits, persistent political pressure to boost social spending is likely to weigh on Chile’s public finances over the next two to three years.

As a result, S&P expects net general government debt to hover around 30% of GDP by 2024, just below its current level (chart 1). Interest costs are likely to average 4.3% of general government revenues during 2021–24, thereby capturing favourable financing conditions in the international and domestic markets, but reflecting a structurally higher debt level.

On the bright side, S&P’s ratings on Chile are based on its policy nimbleness and prosperous economy, as well as its favourable assessment of Chile’s institutional effectiveness and governance. A transparent, rules-based fiscal policy and still low debt levels, along with an autonomous central bank with a credible track record of targeting inflation, support the rating.

The sovereign’s institutional strength has contributed over the years to stable economic policies along with smooth changes in government, consistent economic growth, a weaker but still healthy fiscal situation, and low inflation. Governance indicators are strong, perceived corruption is low, and human development readings are better than most regional peers. The strength of public institutions helped to ensure relatively good management of the COVID-19 pandemic and a less severe economic contraction than in many regional neighbours, which minimized its social costs.

Chile will shortly elect delegates to write a new constitution. The move follows a recent referendum that rejected the current constitution, which had been written by a military government in 1980 and amended many times by subsequent civilian governments. The new constitution is likely to feature commitments to stronger social benefits, which may translate gradually into the provision of more public services by the government in the next five to 10 years.

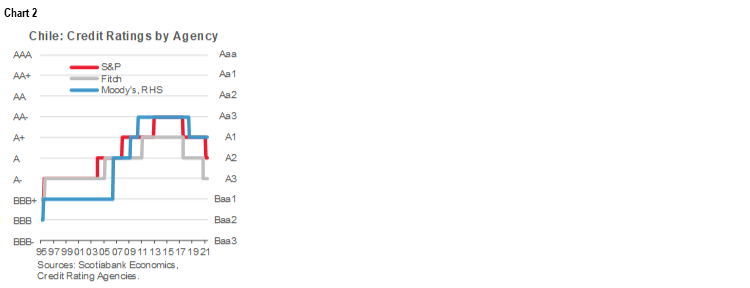

All in all, Fitch continues to have the lowest credit rating for Chile, with an “A-” (chart 2). Now, Fitch is located 1 notch below S&P and two notches below Moody’s. Given that the Moody’s assessment of the Chilean economy was done after Fitch’s downgrade in March 2020, we don’t anticipate any more changes in credit agencies’ ratings.

—Carlos Muñoz

MEXICO: BANXICO DELIVERED UNANIMOUS HOLD AT 4.00%; RECOVERY PACE REMAINS GRADUAL

I. Banxico delivered unanimous hold at 4.00%

As most analysts expected, and was priced in, Banxico’s Board delivered a unanimous hold of its overnight target rate at 4.00% at its Thursday, March 25, meeting. The MXN outperformed other emerging-markets’ currencies on Thursday, both in anticipation of a more cautious signal from the central bank and following its actual delivery: the Mexican peso gained about 1% on the day while other Latam currencies were in the red.

The Board’s statement noted domestic and international factors that underpinned the decision to hold the benchmark policy rate unchanged. The Board highlighted the spike in core inflation we saw in early-March to 4.09% y/y, above the top of the 2–4% y/y headline inflation target range, as well as risks from depreciations in the MXN. The Board pointed to the need to ensure an orderly adjustment in markets: with recent increases in US and other emerging-market rates, cutting at this stage to support the domestic economy could have heightened risks to financial stability.

Looking forward, the Board maintained relatively neutral, data-dependent guidance. It explained that its next moves would “depend on the evolution of the factors that have an impact on inflation, on inflation’s projected trajectories within the forecast horizon, and on inflation expectations”.

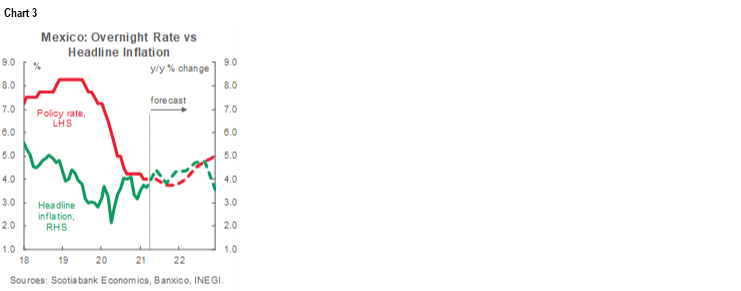

We maintain our view that recent data augurs for additional caution from the Board and that the space for further easing is very narrow. We anticipate only one more cut, likely in Q3-2021 (chart 3), but this call remains contingent on Mexican prices exhibiting greater stability in the coming months and US rates finding a ceiling soon.

—Eduardo Suárez

II. Recovery in economic activity remained gradual in January

January IGAE real GDP proxy data, released by INEGI on Thursday, March 25, showed that growth in economic activity picked up from -0.01%% m/m sa in December to 0.1% m/m sa, slightly above the Bloomberg consensus of 0.0% m/m sa. The rebound was driven by stronger growth in industry (up from 0.1% m/m in December to 0.2% m/m) and a solid rebound in agriculture (up from -4.3% m/m in December to 1.8% m/m). These moves were only partially offset by a downturn in services growth that cooled from 0.3% m/m in December to -0.1% m/m.

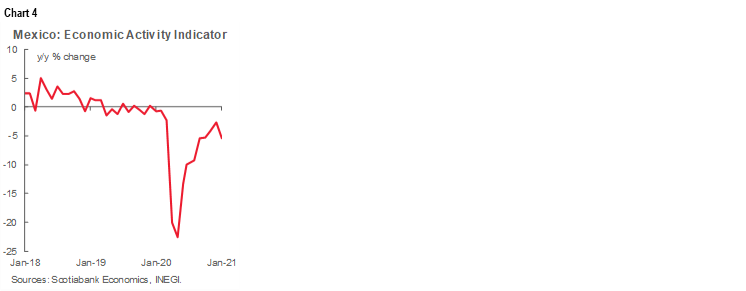

In annual terms, the comparison with a year ago worsened, a reflection of some of the headwinds at the beginning of the year from the resurgence of the pandemic. Annual growth went from -2.7% y/y in December to -5.4% y/y (chart 4), below consensus expectations of -5.25% y/y. By components, industry and services deepened their annual contractions from December’s -2.1% y/y to -4.9% y/y and from end-2021’s -3.1% y/y to -6.1% y/y, respectively. In contrast, agriculture saw growth accelerate from 0.9% y/y in December to 2.3% y/y.

We expect real GDP growth to strengthen significantly in the second half of the year. The further recovery should be driven mainly by the services sector as public-health measures are relaxed.

III. Weak start to commercial activity in 2021

Domestic demand indicators continue to point to a slow rebound, with INEGI’s Thursday, March 25, release showing retail sales growth recovered somewhat, from -2.7% m/m in December to 0.1% m/m in January, while wholesale growth edged up from 0.8% m/m in December to 0.9% m/m. Consumer spending at the beginning of 2021 reflected the negative impact of the new restrictions to mobility and lockdowns that resulted from a second wave of COVID-19 cases in Mexico City and other important regions of the country.

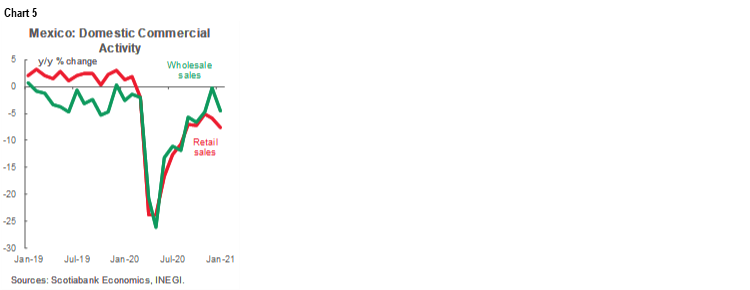

On an annual basis, retail sales were down for an 11th consecutive month in January, going from -5.9% y/y in December to -7.6% y/y. Similarly, annual wholesale sales growth came down from -0.3% y/y in December to -4.5% y/y, for a total of 24 months in the last 26 where total wholesale sales have been below their year-ago levels (chart 5).

We expect cautious consumer behaviour to continue into February in the face of ongoing pandemic-related restrictions.

—Paulina Villanueva

PERU: MOODY’S UPGRADES THE OUTLOOK FOR PERUVIAN BANKS FROM “NEGATIVE” TO “STABLE”

Moody’s upgraded its outlook for Peruvian banks from “negative” to “stable” on Wednesday, March 24. Moody’s sees a better environment for Peruvian banks over the next year and a half, and specifically highlighted the BCRP’s liquidity injections and the government’s loan guarantees as key instruments that are supporting local banks’ financial profiles in 2021. In general, banks are coming out of the worst of the COVID-19 pandemic and related lockdowns much better-off than many may have expected given the magnitude of the past year’s disruptions. And, yet, it is a bit surprising that Moody’s changed its outlook ahead of the April 11 elections given uncertainties around possible regime change and consequent implications for the banking system.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.